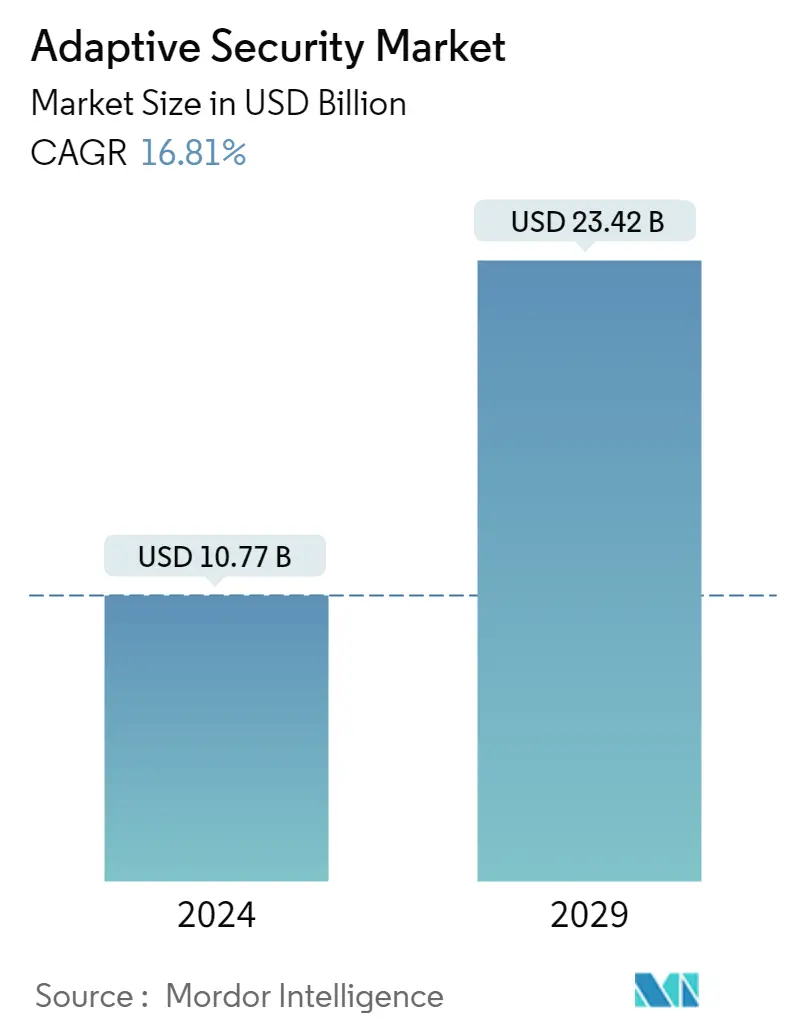

Adaptive Security Market Size

| Study Period | 2018 - 2028 |

| Market Size (2023) | USD 9.22 Billion |

| Market Size (2028) | USD 20.05 Billion |

| CAGR (2023 - 2028) | 16.81 % |

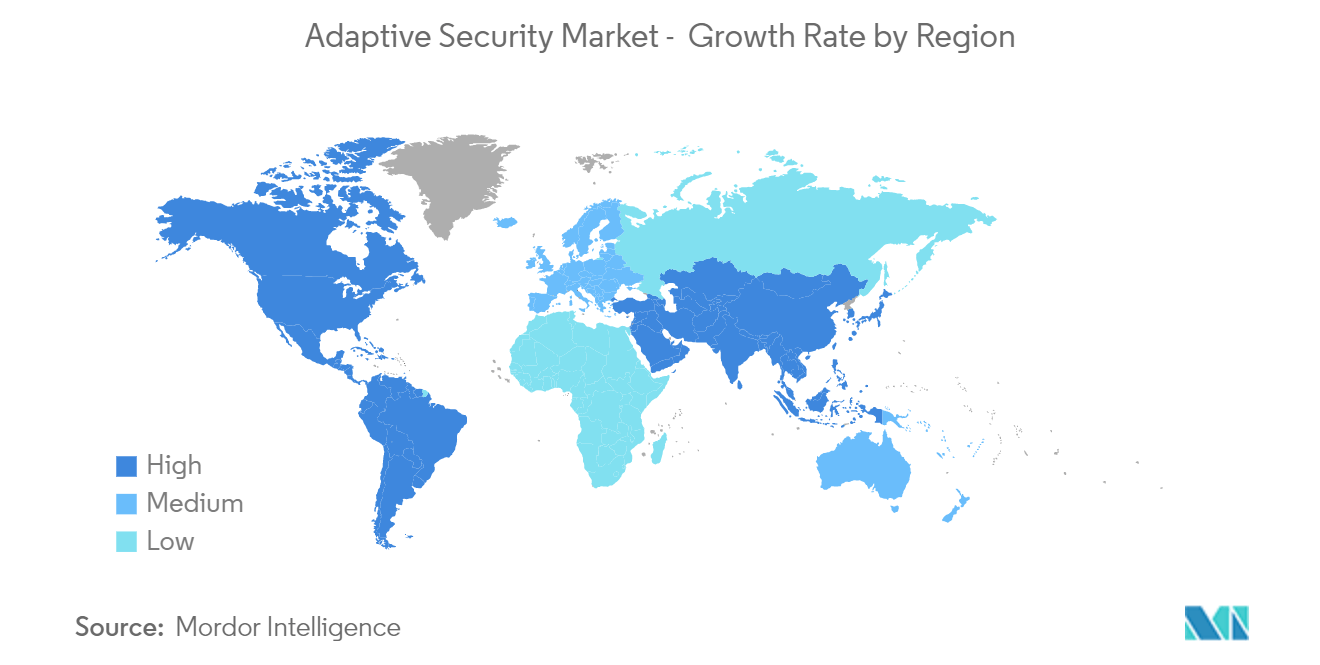

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Adaptive Security Market Analysis

The Adaptive Security Market size is expected to grow from USD 9.22 billion in 2023 to USD 20.05 billion by 2028, at a CAGR of 16.81% during the forecast period (2023-2028).

To secure businesses' data, networks, and applications, enterprises have increasingly used preventative measures to keep track of undetected risks.

- The primary factor driving adaptive security market expansion is that enterprises are continually being attacked by sophisticated threats such as advanced persistent threats (APTs), zero-day malware, and other targeted assaults. These current assaults are dynamic and coordinated, intending to exploit flaws in an organization's traditional defenses. Cybercriminals can breach a company's information technology (IT) infrastructure and access business-critical information to inflict harm and enormous financial and data loss. Protecting against increasingly sophisticated cyberattacks, then, necessitates preparation that goes beyond traditional defenses.

- Growing demand for multilayer security and smart solutions, as well as the urgent requirement for regulatory compliance, are some factors predicted to fuel market growth during the forecast period. The adaptive security market is driven by the growing usage of cloud-based security systems, particularly in organizations. However, factors such as a lack of technical skills and problems processing vast volumes of data limit the need for global adaptive security.

- Furthermore, the rising acceptance of cloud-based security solutions will likely generate attractive market development possibilities. Adaptive security strategies attempt to use an organization's present security infrastructure to develop a strong security posture. To safeguard their networks, endpoints, data, and users from malicious assaults, large and small companies (SMBs) try to deploy security solutions that can adapt to emerging threats. Businesses do not want to spend money on security services that are not necessary.

- Prioritizing the risks most important to their business can help them learn how to prevent such assaults in the future. The industry of adaptive security faces substantial obstacles from the expanding data and the demand for more qualified employees. These barriers make it difficult for enterprises to implement adaptive security solutions. During the forecast period, the need for more seasoned cybersecurity experts is anticipated to restrain the growth of the Adaptive Security Market.

- With the outbreak of COVID-19, almost the majority of the organization shifted to the work-from-home model due to the lockdown ad social distancing measures that created a significant demand for managing the application and monitoring the application aspect remotely. As a result of the rising demand from organizations for adaptive security for their application services needs, some companies providing adaptive application security services are making strategic inroads into delivering a package of services.

- For example, OpsRamp recently expanded its network, UC monitoring for the WFH world with new functionality in the OpsRamp platform that allows solution providers to help customers manage hybrid and multi-cloud IT environments and meet the needs of work-from-home employees as demand for cloud applications, unified communications (UC) and collaboration tools, video conferencing, and other IT resources increased significantly.

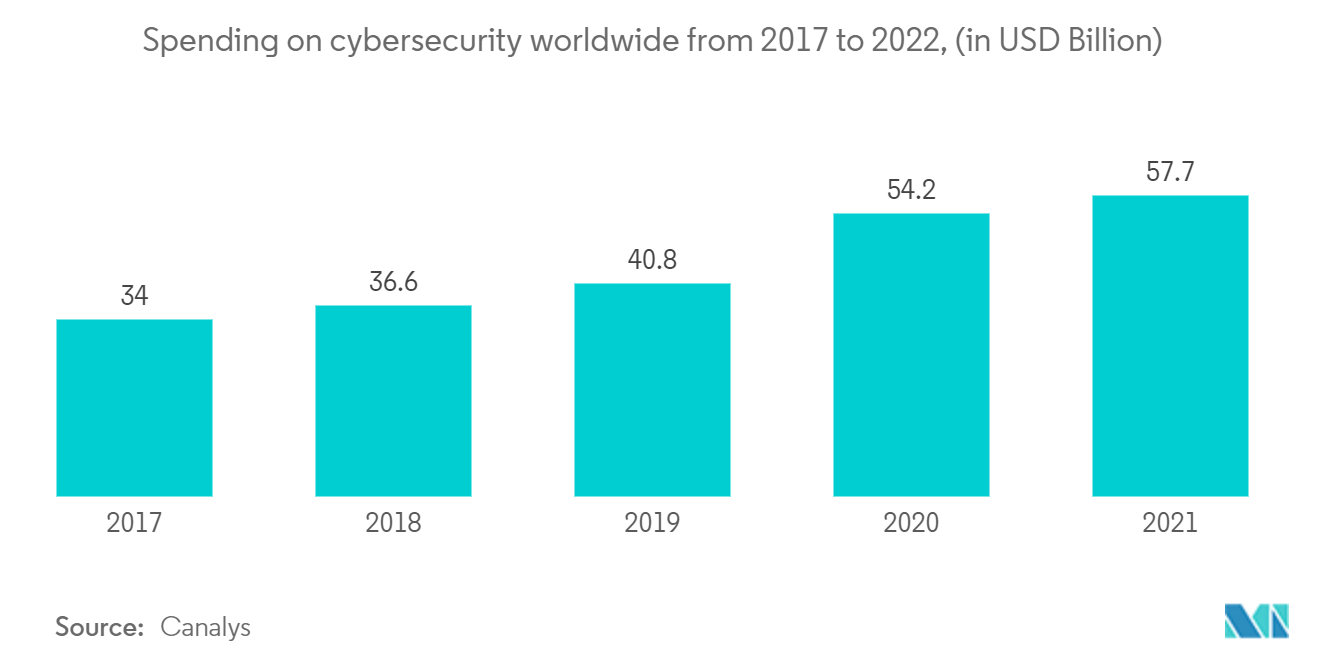

- Furthermore, there was an increase in cyber-attacks and data breaches throughout the epidemic. According to VMware's Cybersecurity Threat Survey Report, supplemented with a survey on the impact COVID-19 had on the attack landscape, 88% of US cybersecurity professionals stated that as more workers work from home, attack volumes rose. Moreover, 89% reported cyberattacks tied to COVID-19 malware in their companies. Approximately 89% reported being targeted by COVID-19-related malware.

Adaptive Security Market Trends

Cloud to Hold Significant Share

- Cloud security is less expensive to install than traditional premise-based systems, and firms may save money and staff. The provider also supplies the bandwidth, IT professionals, and infrastructure to safeguard the data.

- Due to enhanced agility, cheaper capital costs, and streamlined operation (from software to infrastructure-as-a-service), businesses' rapid adoption of cloud solutions and services by enterprises need equally dynamic cloud protection. This new environment necessitates cloud-based adaptive security.

- The latency, delays, and hazards of running confidential data from a cloud provider are at risk as cyber assaults get more complicated.

- As a result, enterprises are looking to install a hybrid solution in which on-premise solutions automatically update and secure network protection regularly and utilize the cloud to give a second layer of defense against various assaults.

North America to Hold Major Share

- North America is the most active and committed area regarding cybersecurity activities. The main nations' GCI (global cybersecurity index) scores (United States of America - 100 and Canada - 97.67) reaffirm their commitment to constructing a strong cybersecurity framework.

- However, due to the existence of vital corporations and data centers, North America is rated the most susceptible. The US Department of Homeland Security identified more than 60 organizations in critical infrastructure in the United States that were damaged by a single event that cost over USD 50 billion.

- The region's SMEs (about 97% of total firms) favor cloud deployment to reduce the total cost of ownership of security solutions. As a consequence, security solution providers have a chance to design solutions that meet customer needs. It is also predicted that most of these players would use technology and deploy effective end-point security measures to improve the client experience.

Adaptive Security Industry Overview

The adaptive security market is moderately competitive. The players in the market are innovating in providing strategic solutions to increase their market presence and customer base. This enables them to secure new contracts and tap new markets.

In March 2023, Rapid7, a cloud risk and threat detection company, announced the acquisition of Minerva Labs, Ltd., a provider of anti-evasion and ransomware protection technologies. Rapid7's Managed Detection and Response (MDR) services now give clients enhanced detection and response capabilities across cloud, on-premise, and extended attack surfaces. Rapid7's superior managed threat detection capabilities will be expanded with the ability to organize sophisticated ransomware protection due to this purchase. These new capabilities will allow companies to further consolidate their security expenditures by seamlessly extending MDR across cloud resources, legacy infrastructure, and current endpoint protection architecture.

In June 2022, Cisco, the business networking and security company, announced plans for a worldwide, cloud-delivered, integrated platform that secures and connects enterprises of any size and shape. With no public cloud lock-in, the Cisco Security Cloud was intended to be the most open platform in the market, preserving the integrity of the whole IT ecosystem.

The Security Cloud offers a unified experience for securely connecting people and devices to apps and data everywhere. The open platform delivers threat prevention, detection, response, and remediation capabilities at scale through a unified administration. Cisco has been on the path to the Security Cloud for some time and is now sharing further progress with new security advancements throughout its portfolio.

In July 2021, Rapid7, Inc., a provider of security analytics and automation, announced the release of InsightCloudSec, the fully integrated Cloud-Native Security Platform (CNSP). With continuous security and compliance for complex cloud environments, InsightCloudSec enabled organizations to improve their cloud security programs. InsightCloudSec, the newest component of Rapid7's Insight Platform, combined the cloud security posture management, infrastructure entitlements management, and infrastructure as code capabilities of DivvyCloud (acquired in May 2020), Kubernetes security provider Alcide (acquired in January 2021), and other cloud security providers into a single seamless cloud security solution.

Adaptive Security Market Leaders

Cisco Systems Inc.

Trend Micro Incorporated

Juniper Networks Inc.

Aruba Networks Inc.

Rapid7

*Disclaimer: Major Players sorted in no particular order

Adaptive Security Market News

- February 2022: Francois-Philippe Champagne, Minister of Innovation, the Canadian government, has announced that the National Cybersecurity Consortium (NCC) will receive up to USD 80 million to oversee the Cyber Security Innovation Network (CSIN). This money would contribute to developing a robust national cyber security ecosystem in Canada, positioning the country as a global leader in cyber security. Furthermore, Cyber Security Innovation Network (CSIN) will enhance research and development, increase commercialization, and develop skilled cyber security talent to expand Canada's national cyber security ecosystem and increase collaboration between academia, the private sector, non-profit sectors, and other levels of government from across Canada. The network will likely address the scarcity of cyber security personnel by increasing collaboration between academics and businesses. And by using Canada's highly trained workforce, world-class institutions, and rising cyber security business, CSIN will likely help Canada maintain its leadership in cyber security.

- May 2022: The National Cybersecurity Authority (NCA) launched the National Portal for Cyber Security Services (HASEEN) to create and administer cyber services, support communication mechanisms for national beneficiaries, and increase cybersecurity in the Kingdom. Furthermore, Eng. Majed bin Mohammed Al-Mazyed, Governor of The National Cybersecurity Authority (NCA), stated that cybersecurity had become critical in protecting the Kingdom's fundamental interests, assets, and infrastructure. The communications and information technology (ICT) industry was characterized by fast development in attack tactics and complexity, requiring governments to be always ready and flexible to neutralize any cyber danger. Moreover, he also stated that the HASEEN webpage is part of the Authority's efforts to improve national cybersecurity by managing national cybersecurity funds and developing local content in the ICT industry. As a result, NCA laws are consistent with best worldwide practices.

Adaptive Security Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Introduction to Market Drivers and Restraints

4.3 Market Drivers

4.3.1 Need to Secure IT Resources from Advanced Cyberattacks

4.3.2 Need for Security Compliances and Regulations

4.4 Market Restraints

4.4.1 Lack of Skilled Cyber Security Professionals

4.5 Industry Attractiveness - Porter's Five Forces Analysis

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Power of Buyers/Consumers

4.5.3 Threat of New Entrants

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Application

5.1.1 Application Security

5.1.2 Network Security

5.1.3 End Point Security

5.1.4 Cloud Security

5.2 Offering

5.2.1 Service

5.2.2 Solution

5.3 Deployment Model

5.3.1 On-premise

5.3.2 Cloud

5.4 End-User

5.4.1 BFSI

5.4.2 Government & Defense

5.4.3 Manufacturing

5.4.4 Healthcare

5.4.5 Energy & Utilities

5.4.6 IT & Telecom

5.4.7 Other End-Users

5.5 Geography

5.5.1 North America

5.5.2 Europe

5.5.3 Asia-Pacific

5.5.4 Latin America

5.5.5 Middle East & Africa

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Cisco Systems Inc.

6.1.2 Trend Micro Incorporated.

6.1.3 Rapid7

6.1.4 RSA Security LLC

6.1.5 Juniper Networks, Inc.

6.1.6 Fireeye Inc. (Trellix)

6.1.7 Panda Security Inc.

6.1.8 Illumio Inc.

6.1.9 Cloudwick

6.1.10 Aruba Networks Inc.(Hewlett Packard Enterprise Development LP)

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

Adaptive Security Industry Segmentation

Adaptive security is a method in which threats are constantly monitored and improved as cybersecurity dangers alter and adapt. Adaptive security software analyses behaviors and trends rather than only checking log files, monitoring checkpoints, and responding to warnings. It aims to create a feedback loop of threat detection, visibility, and protection that improves with time. Adaptive security is an intuitive intelligence strategy anticipated to detect cybercriminal practices and procedures, forestall an assault, and perhaps respond to a breach in milliseconds.

The Adaptive Security Market is segmented by Application (Application Security, Network Security, End-point Security, Cloud Security), Offering (Service, Solution), Deployment Model (On-premise, Cloud), End User (Global BFSI, Government & Defense, Manufacturing, Healthcare, Energy & Utilities, IT & Telecom, Other End Users), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Application | |

| Application Security | |

| Network Security | |

| End Point Security | |

| Cloud Security |

| Offering | |

| Service | |

| Solution |

| Deployment Model | |

| On-premise | |

| Cloud |

| End-User | |

| BFSI | |

| Government & Defense | |

| Manufacturing | |

| Healthcare | |

| Energy & Utilities | |

| IT & Telecom | |

| Other End-Users |

| Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East & Africa |

Adaptive Security Market Research FAQs

How big is the Adaptive Security Market?

The Adaptive Security Market size is expected to reach USD 9.22 billion in 2023 and grow at a CAGR of 16.81% to reach USD 20.05 billion by 2028.

What is the current Adaptive Security Market size?

In 2023, the Adaptive Security Market size is expected to reach USD 9.22 billion.

Who are the key players in Adaptive Security Market?

Cisco Systems Inc., Trend Micro Incorporated, Juniper Networks Inc., Aruba Networks Inc. and Rapid7 are the major companies operating in the Adaptive Security Market.

Which is the fastest growing region in Adaptive Security Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (20221-2028).

Which region has the biggest share in Adaptive Security Market?

In 20221, the North America accounts for the largest market share in Adaptive Security Market.

Adaptive Security Industry Report

Statistics for the 2023 Adaptive Security market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Adaptive Security analysis includes a market forecast outlook to for 2023 to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.