APAC Wind Turbine Rotor Blade Market Size

| Study Period | 2019 - 2028 |

| Base Year For Estimation | 2021 |

| Forecast Data Period | 2024 - 2028 |

| Historical Data Period | 2019 - 2020 |

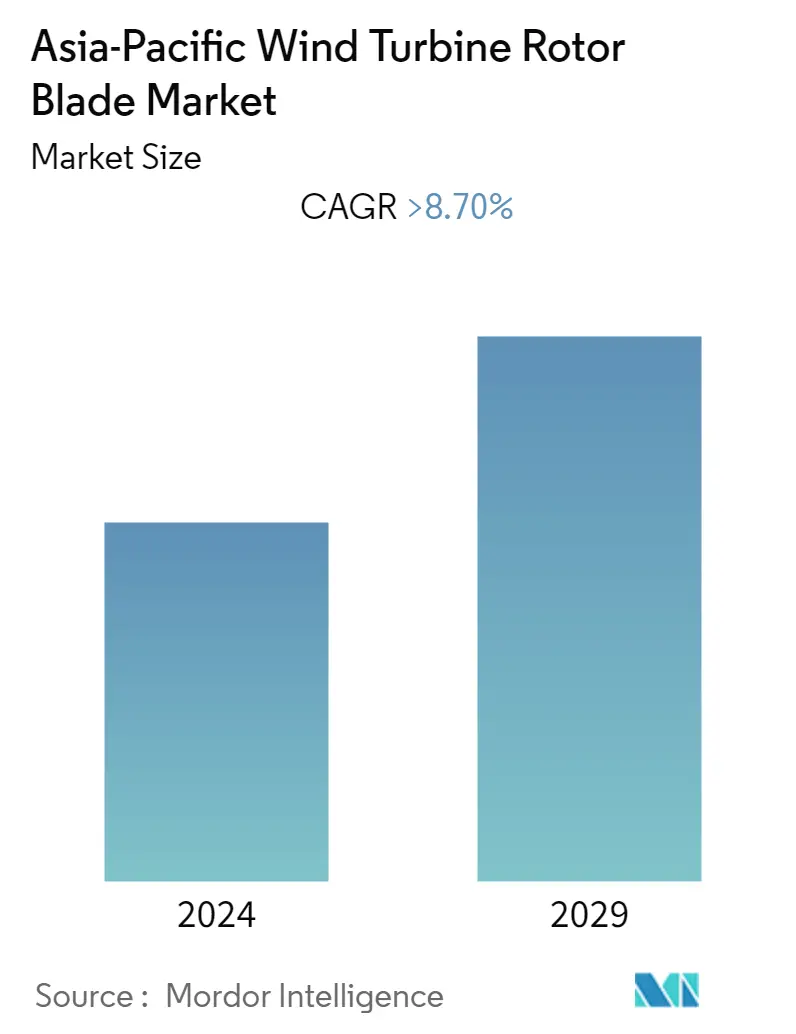

| CAGR | > 8.70 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

APAC Wind Turbine Rotor Blade Market Analysis

The Asia-Pacific wind turbine rotor blade market is expected to register a CAGR of more than 8.7% during the forecast period of 2022 - 2027. With the COVID-19 outbreak in Q1 of 2020, the growth of the wind turbine rotor blade market in the Asia-Pacific region was moderately impacted. Major countries such as China, India, etc. have faced disruptions in manufacturing and supplying of the rotor blades due to unexpected lockdowns. As a result, the commissioning of the wind projects was delayed. Factors such as the declining cost of wind energy and increasing investments in the wind power sector are expected to drive the wind turbine rotor blade market in the Asia-Pacific region during the forecast period. However, factors such as the associated high cost of transportation and cost competitiveness of alternate clean power sources like solar power, hydropower, etc., have the potential to hinder the market growth during the forecast period.

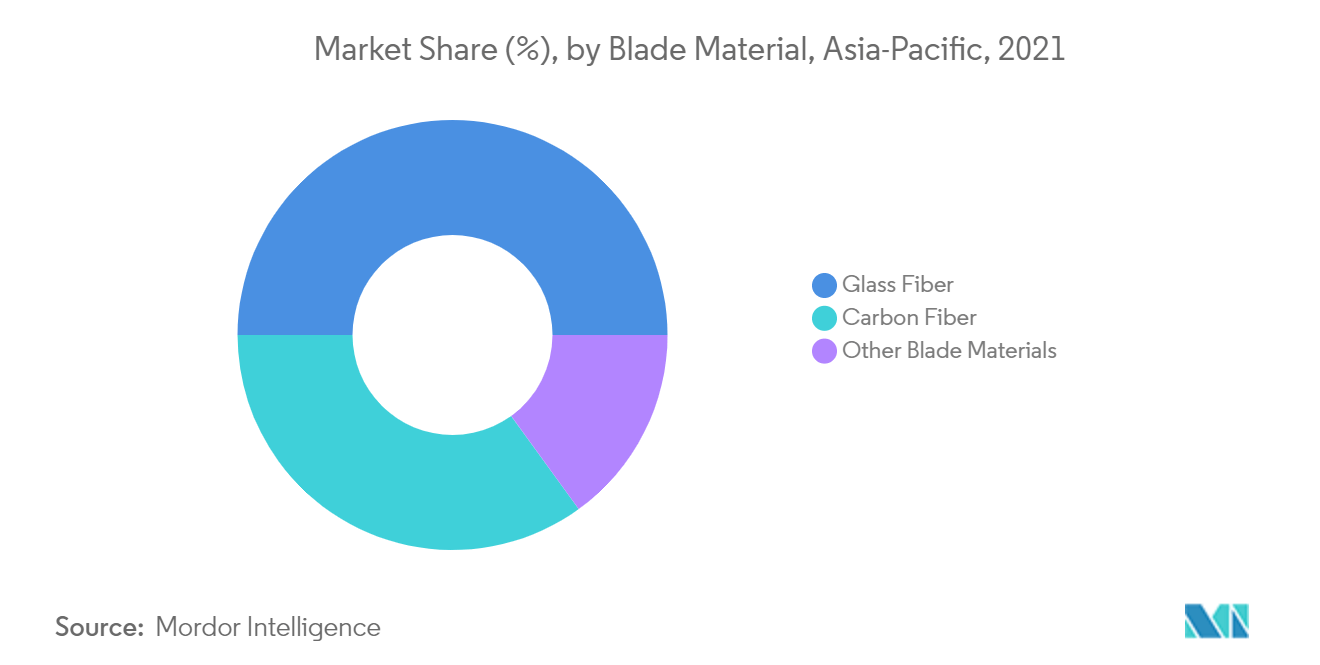

- As the majority of the modern rotor blades on large wind turbines are glass fibers, this segment is expected to witness significant demand for the wind turbine rotor blade market in the Asia-Pacific region during the forecast period.

- The wind power industry has been in demand for cost-effective solutions, and a highly efficient product has the potential to change the dynamics of the industry. There were instances where old turbines were replaced, not because of the damage but due to the availability of more efficient blades in the market. Hence, technological developments present themselves as a good opportunity for the wind turbine rotor blade market soon.

- China is expected to dominate the wind turbine rotor blade market in the Asia-Pacific region during the forecast period.

APAC Wind Turbine Rotor Blade Market Trends

This section covers the major market trends shaping the APAC Wind Turbine Rotor Blade Market according to our research experts:

Glass Fiber Blade Material to Witness Significant Growth

- The majority of the modern rotor blades on large wind turbines are made of glass fiber reinforced plastics (GRP), which is glass fiber reinforced polyester or epoxy. Glass fibers have higher density and are, therefore, heavier than carbon fibers.

- Apart from GRP, the wind turbine blades also contain sandwiched core materials, such as polyvinyl chloride foam, polyethylene terephthalate foam, or balsa wood, as well as bonded joints, coatings (polyurethane), and lightning conductors.

- As of 2020, the wind power industry was the largest market for glass fiber-reinforced composites. Glass is an inexpensive material to use, especially when compared to other popular-use composite materials, such as carbon or aramid fibers. Additionally, glass fiber does not corrode as metals do, therefore, it requires less maintenance and is an overall more cost-effective solution. These are the significant advantages for a wind turbine to have, since they are constantly exposed to the elements, both, on land and at sea.

- Typically, E-glass fibers (i.e., borosilicate glass) are used as the main reinforcements in the composites. S-glass and R-glass are the modified compositions of high-strength glass fibers. S-glass (high strength glass, S means “Strength”) exhibits 40% higher tensile and flexural strengths and 10–20% higher compressive strength and flexural modulus, compared to E-glass.

- Glass fiber represents the primary material in wind turbine blades. Some of the leading blade manufacturing companies, such as TPI Composites and LM Wind Power, rely on third parties for their raw materials. The glass fiber raw materials are mostly available in multiple geographic regions and reasonably proximity to the manufacturing facilities.

- Therefore, based on the above-mentioned factors, glass fiber blade material is expected to witness significant demand for the wind turbine rotor blade market in the Asia-Pacific region during the forecast period.

China to Dominate the Market

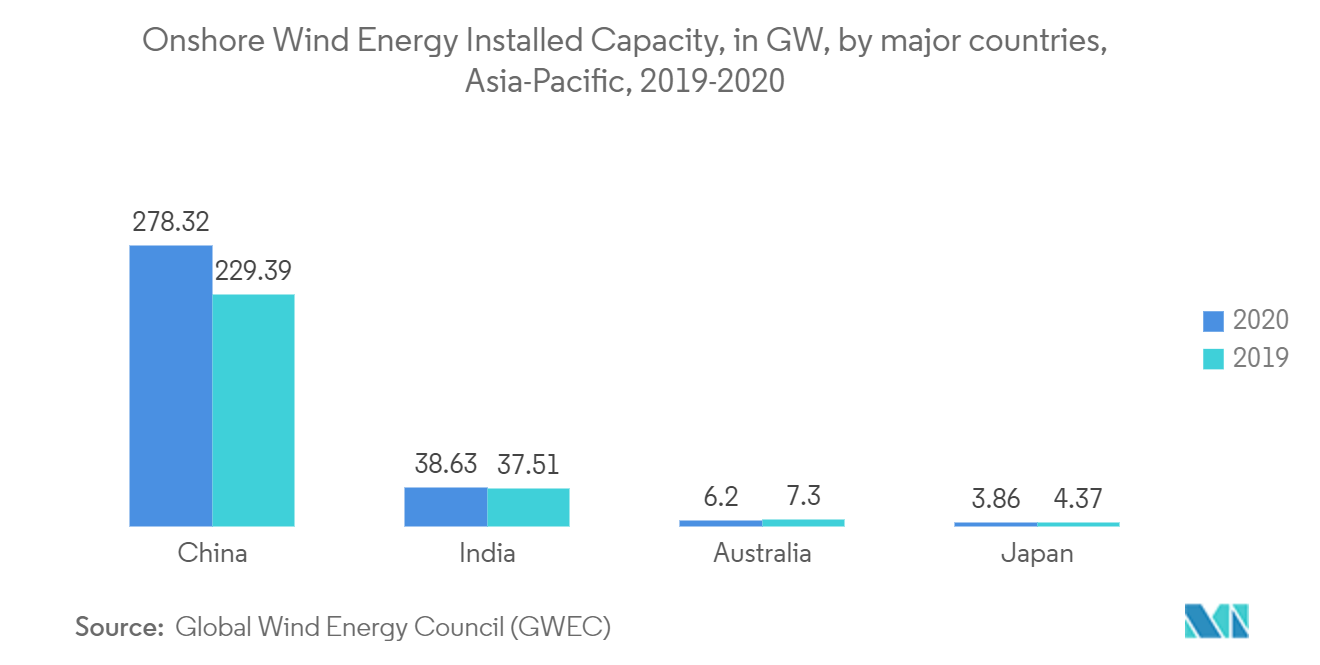

- The Asia-Pacific region is the regional hotspot for the wind turbine rotor blade market, owing to governmental support, numerous incentives, and national targets. As of 2020, the total installed wind power generation in the region reached 572.6 TWh, representing an increase of 12.41% over the previous year.

- Since the invention of the modern wind turbine generator (WTG) in 1891, China has recognized that wind energy technology offers an effective way to provide electricity to rural and isolated areas. China’s installed wind capacity has grown from a mere 4 MW in 1990 to 281.99 GW by the end of 2020 as a result of policy reforms, dedicated R&D initiatives, new financing mechanisms, and clear goals in the most recent Five-Year Plans.

- Both China's installed capacity and new capacity in 2020 are the largest in the world by a wide margin. According to IRENA, China is expected to continue to dominate the onshore wind power industry, with more than 50% of global installations by 2050. Also, due to the high population, high electricity demand in the country is expected to promote growth in wind energy. Many multinational corporations, including Chinese firms, are investing in this sector with the help of the federal and provincial governments across the country.

- The Chinese onshore wind market is expected to grow steadily in the coming years, with rising needs for key components and materials, not only for the national market but also for international exports. Besides, in China, nearly 70% of the electricity produced is from thermal sources of energy. Owing to the increasing pollution from thermal sources, the country has been making efforts to increase the share of cleaner and renewable sources in power generation. Furthermore, out of the total 6.1 GW installed offshore worldwide, 50% of the installations were from China in 2020 and the total offshore capacity of China stood at 9.884 GW.

- Therefore, all of this indicates that China is expected to be the largest market for wind turbine nacelle in the Asia-Pacific region.

APAC Wind Turbine Rotor Blade Industry Overview

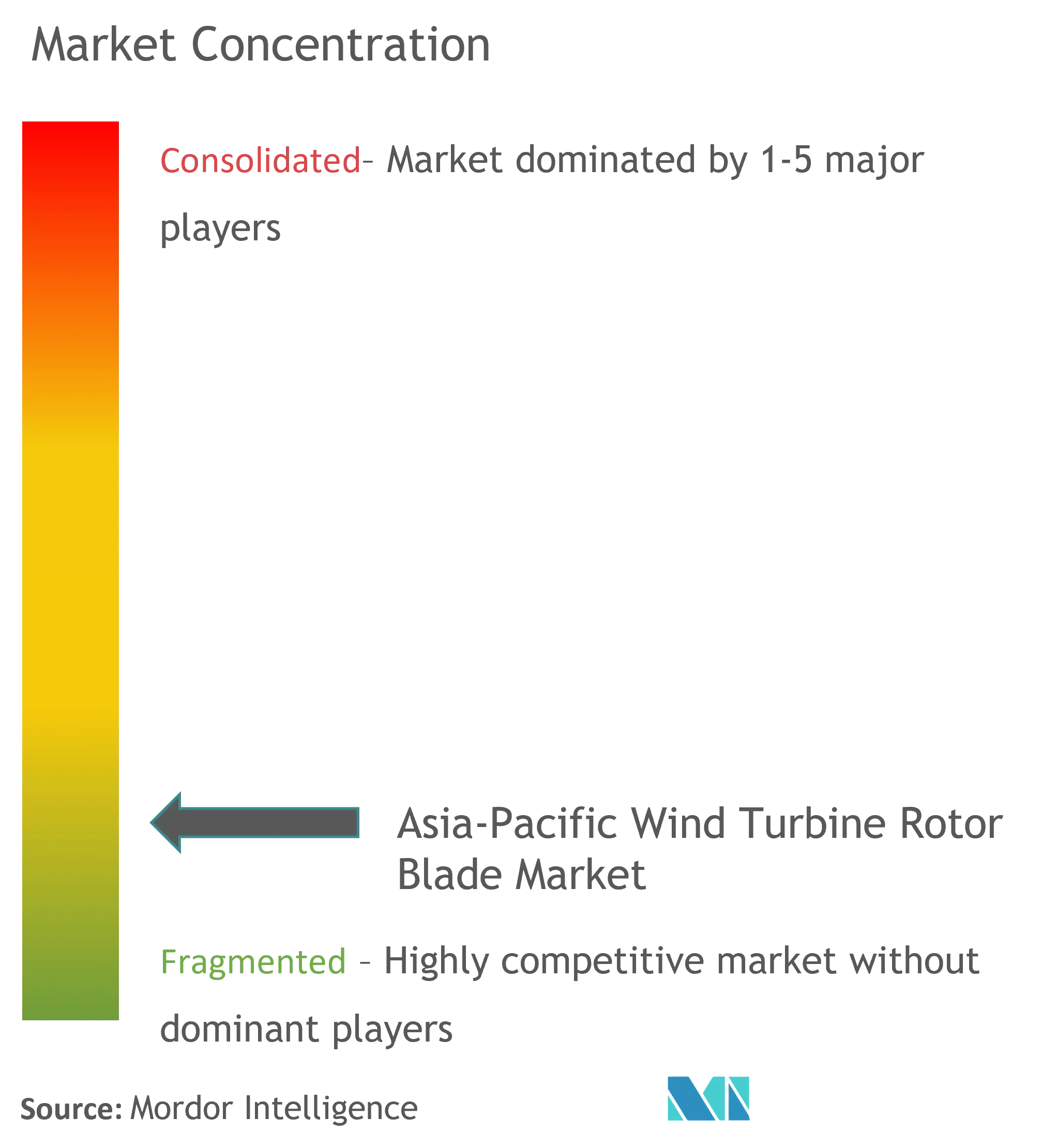

The Asia-Pacific wind turbine rotor blade market is moderately fragmented. Some of the major players in the market include Lianyungang Zhongfu Lianzhong Composites Group Co., Ltd., TPI Composites Inc., LM Wind Power (a GE Renewable Energy Business), Siemens Gamesa Renewable Energy S.A., and Vestas Wind Systems A/S.

APAC Wind Turbine Rotor Blade Market Leaders

TPI Composites Inc.

Lianyungang Zhongfu Lianzhong Composites Group Co., Ltd.

LM Wind Power (a GE Renewable Energy Business)

Siemens Gamesa Renewable Energy S.A.

Vestas Wind Systems A/S

*Disclaimer: Major Players sorted in no particular order

APAC Wind Turbine Rotor Blade Market News

- In October 2021, GE Renewable Energy received an order from JSW Energy to supply 810 MW of onshore wind turbines for upcoming wind farms in Tamil Nadu, India. LM Wind Power, a subsidiary company of GE, is likely to provide rotor blades for this project.

- In September 2021, Lianyunghas launched its first large-scale 100-meter offshore wind turbine blade of LZ Blades in Lianyungang blade production base. The blade is 102 meters long and adopts new interface fusion technologies such as carbon fiberspar cap, blade root prefabrication and trailing edge auxiliary beam prefabrication.

APAC Wind Turbine Rotor Blade Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2027

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.2 Restraints

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGEMENTATION

5.1 Location of Deployment

5.1.1 Onshore

5.1.2 Offshore

5.2 Blade Material

5.2.1 Carbon Fiber

5.2.2 Glass Fiber

5.2.3 Other Blade Materials

5.3 Geography

5.3.1 China

5.3.2 India

5.3.3 South Korea

5.3.4 Japan

5.3.5 Rest of Asia-Pacific

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Companies Profiles

6.3.1 TPI Composites Inc.

6.3.2 Lianyungang Zhongfu Lianzhong Composites Group Co., Ltd.

6.3.3 LM Wind Power (a GE Renewable Energy Business)

6.3.4 Siemens Gamesa Renewable Energy S.A.

6.3.5 Vestas Wind Systems A/S

6.3.6 Sinoma Technology Wind Power Blade Co., Ltd.

6.3.7 Suzlon Energy Limited

6.3.8 Nordex SE

6.3.9 Enercon GmbH

7. MARKET OPPORTUNITIES and FUTURE TRENDS

APAC Wind Turbine Rotor Blade Industry Segmentation

The Asia-Pacific wind turbine rotor blade market report includes:

APAC Wind Turbine Rotor Blade Market Research FAQs

What is the current Asia-Pacific Wind Turbine Rotor Blade Market size?

The Asia-Pacific Wind Turbine Rotor Blade Market is projected to register a CAGR of greater than 8.7% during the forecast period (2023-2028).

Who are the key players in Asia-Pacific Wind Turbine Rotor Blade Market?

TPI Composites Inc., Lianyungang Zhongfu Lianzhong Composites Group Co., Ltd., LM Wind Power (a GE Renewable Energy Business), Siemens Gamesa Renewable Energy S.A. and Vestas Wind Systems A/S are the major companies operating in the Asia-Pacific Wind Turbine Rotor Blade Market.

Asia-Pacific Wind Turbine Rotor Blade Industry Report

Statistics for the 2023 Asia-Pacific Wind Turbine Rotor Blade market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Asia-Pacific Wind Turbine Rotor Blade analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.