Encoder Market Size

| Study Period | 2017-2027 |

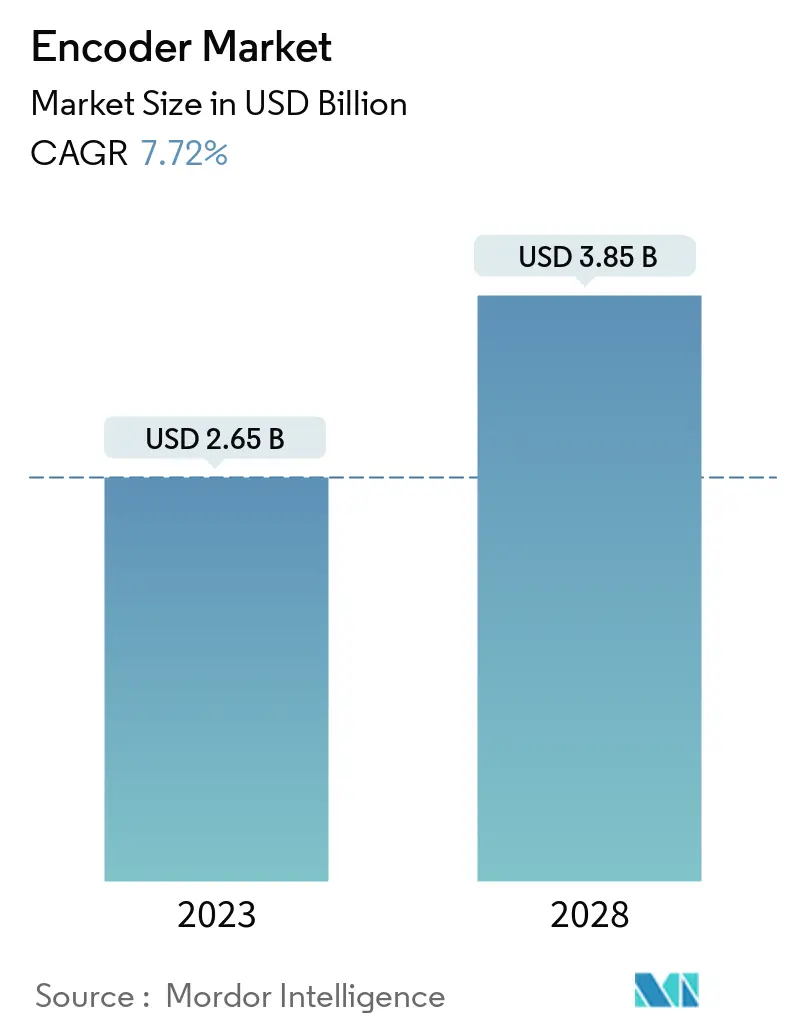

| Market Size (2023) | USD 2.65 Billion |

| Market Size (2028) | USD 3.85 Billion |

| CAGR (2023 - 2028) | 7.72 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Encoder Market Analysis

The Encoder Market size is expected to grow from USD 2.65 billion in 2023 to USD 3.85 billion by 2028, at a CAGR of 7.72% during the forecast period (2023-2028).

The market is witnessing rapid growth due to the increasing demand for encoders in multiple applications, from data centers to telecommunication.

The need for high-end automation and Industry 4.0 are the major factors driving the growth of the market. Industry 4.0 describes the fourth industrial revolution, a new world where factory automation moves beyond manufacturing plants controlled by conventional information technology systems to a cloud-based infrastructure that permits big data analytics and the virtualization of production processes.

Many countries worldwide have positively responded to Industry 4.0 by developing strategic initiatives to strengthen its implementation. For instance, SAMARTH Udyog Bharat 4.0 is an Industry 4.0 initiative of the Ministry of Heavy Industry & Public Enterprises, Government of India, under its scheme on Enhancement of Competitiveness in the Indian Capital Goods Sector. According to the UNCTAD, China and the United States are leaders in investment and capacity in Industry 4.0 technologies. They are home to the largest digital platforms, accounting for 90% of the market capitalization.

Furthermore, encoders are central to motion control applications. They can offer feedback on position, speed, and direction to a controller or drive to increase the accuracy and reliability of a drive system. As technology advances, so do encoders, incorporating the latest developments in communications and networking and offering engineers tools to solve challenges they face across a diverse array of motion control applications.

One of the most significant limitations of encoders is that they can be reasonably complex and comprise some delicate parts. This makes them less tolerant of mechanical abuse and restricts their allowable temperature. One would be hard-pressed to find an optical encoder that will survive beyond 120ºC. Such limitations pose a challenge to the market's growth.

Since the outbreak of COVID-19, industries have been looking for automation to reduce human interaction and enhance efficiency. For instance, leading retail and grocery outlets are exploring ways to ensure faster, automated self-checkouts that minimize human contact and keep shoppers and employees safe. Increased investment in automation and automated printing equipment has also been observed in the printing industry, which further has been instigated by the pandemic. For instance, in February 2021, Thieme announced that it had installed a new printing line at LUMON Oy in Kouvola, Finland, which allowed an automatic adaptation of different glass sizes to be printed without screen change or manual cleaning. These changes are expected to aid the growth of the market studied.

Encoder Market Trends

This section covers the major market trends shaping the Encoder Market according to our research experts:

Industrial Sector is Expected to Hold Major Market Share

Encoders are utilized in multiple industrial applications, such as linear measurement, registration mark timing, web tensioning, backstop gauging, conveying, filling, and more. The most standard application is providing feedback on the motion control of electric motors. In the industrial sector, a significant amount of electricity goes to electric power motors. Most of these motors have encoders incorporated into them.

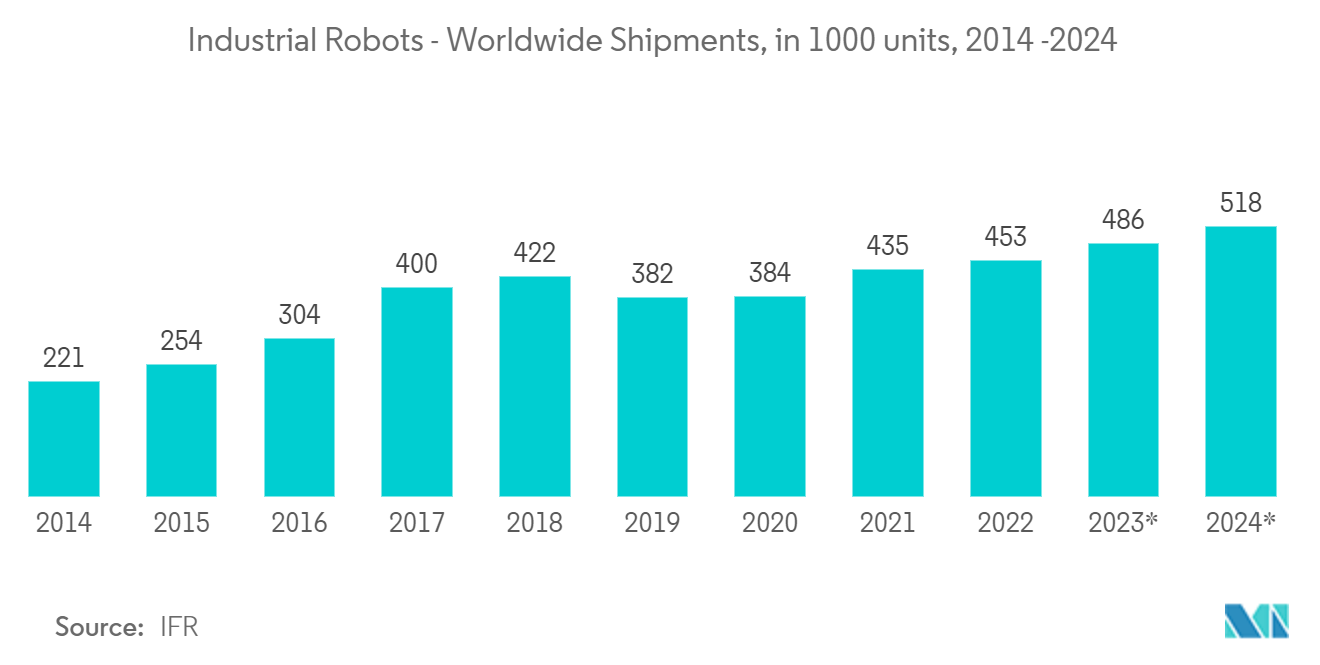

Robots are experiencing a growing number of application areas, especially for operations like welding, material handling, assembly, and grinding. Since there is typically limited human oversite or monitoring, these robots must have reliable encoders to help guide their movement.

As per the IFR, China's massive investment in industrial robotics in recent years has moved its position up among various other countries for robot density, surpassing the United States for the first time. The number of operational industrial robots relative to the number of workers reached 322 units per 10,000 employees in the manufacturing industry in China. South Korea, Singapore, Japan, Germany, and China are the world's top five most automated manufacturing countries. Such an increase in the adoption of automation in the industries is expected to further fuel the demand for encoders in the market.

Comau's robotic welding system enhanced its capability with rotary encoders. The pairing of HEIDENHAIN's ECI 1118 absolute rotary encoder with its EnDat2.2 digital interface enhanced the advanced C5G control and 3D SmartLaser laser welding systems' performance. The ECI 1118 measures 262,144 positions per revolution (18-bit), achieving drive system control at almost all speeds.

Companies, such as Strausak AG, are exploring industrial robotics, specifically in terms of the ways it can accelerate operator-free grinding and re-sharpening tools. In this application, a gripper arm is used to pick small tools from tightly loaded pallets into the fixture and back. Every axis of the arm includes HEIDENHAIN's inductive EQI 1100 rotary encoder. This encoder allows the accuracy of 50 µm at the tip of its gripper for the safe, quick, and precise placement of tools with diameters as small as 10 mm.

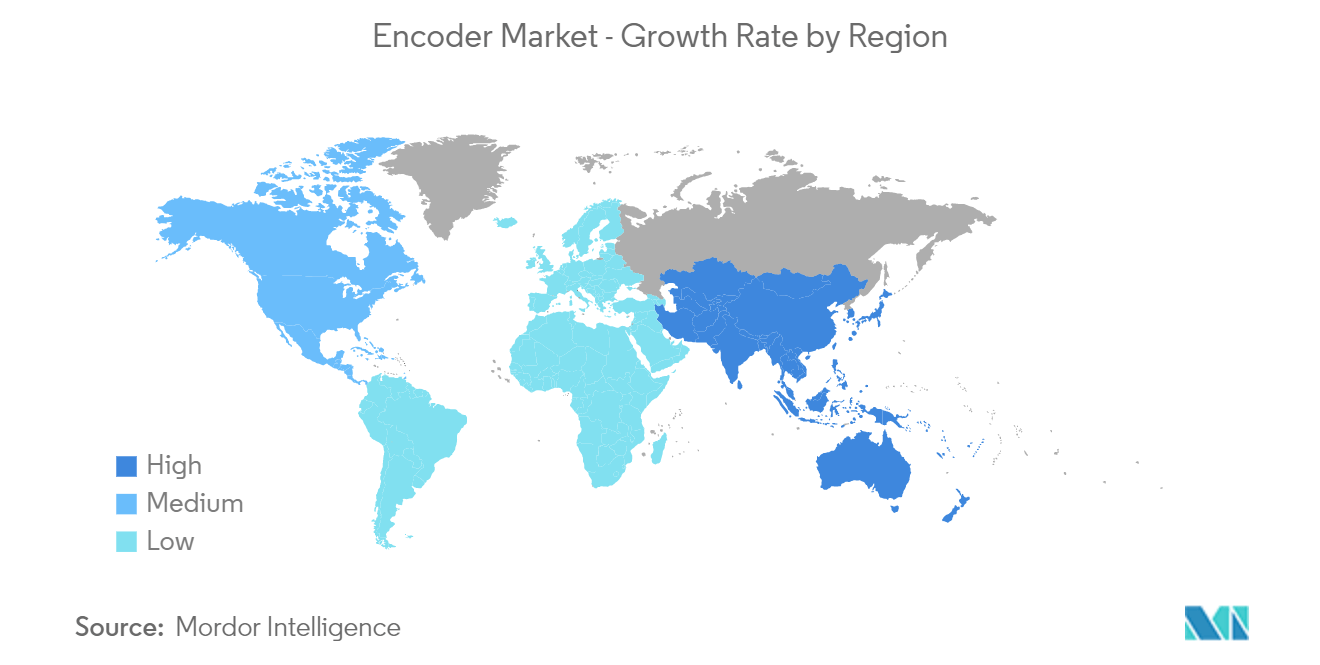

Asia Pacific to Register Fastest Growth

The growing industrialization and demand for better solutions for manufacturing processes are driving the growth of the market at a rapid pace. As Asia is home to large industrial hubs, such as Japan, China, and India, the increasing production facilities and service agreements with businesses are also propelling industry growth. Increasing market rivalry has resulted in the introduction of new items to the market, which has boosted the market’s growth.

According to a report by the IFR (International Federation of Robotics), Asia is the world’s largest market for industrial robots; 74% of all newly deployed robots in 2021 were installed in Asia, compared to 70% in the previous year. Installations for the region’s largest adopter, China, increased by 51%, with 268,195 units shipped.

As per the report, Japan followed China as the largest market for industrial robots; installations increased by 22% in 2021, with 47,182 units. Moreover, the country is the world’s predominant robot manufacturing country, with exports of Japanese industrial robots achieving a new peak level of 186,102 units. Both standard and custom rotary and linear encoders are effectively utilized in electro-medical and laboratory equipment, such as operating and examination tables, Gamma Knife and X-ray, Scanners, and many more.

According to the Indian Brand Equity Foundation 2021, to promote the medical industry, the Government of India (GOI) launched several programs to strengthen the medical device sector, focusing on research and development (R&D) and 100% FDI for medical devices. Between April 2000 and June 2021, FDI in the medical and surgical appliances industry totaled USD 2.23 billion. Such huge investments by the government in the medical sector will drive the market for encoders.

The automotive industry in the region also accounts for a significant share of the total demand for encoders. For instance, as per OICA, China led the market for motor vehicle production in 2021, producing over 26.1 million cars and commercial vehicles that year; the figure was greater than the production values of the other top five countries combined.

South Korea has maintained its position as one of the world’s top automotive manufacturing countries and one of the largest automotive exporters, owing to the presence of many major car makers in the country. Additionally, the trends toward electrification in the region are unlocking new opportunities for the market.

Encoder Industry Overview

The encoder market comprises various players, such as Omron Corporation, Honeywell, Heidenhain GmbH, Baumer Group, and Posital Fraba Inc., among others. The companies have the advantage of a large client base, enabling them to produce large volumes of encoders, a key factor in ensuring better profits and economies of scale in the sensor market. As strong brands are synonymous with good performance, long-standing players are expected to have the upper hand. Owing to their market penetration and the ability to offer advanced products, the competitive rivalry is expected to continue to be high.

In October 2022, Rockwell Automation Inc. acquired CUBIC, a company specializing in modular systems for constructing electrical panels. The company intends to boost its portfolio of leading intelligent motor control technologies with this acquisition.

In March 2022, the explosion-proof IXARC rotary encoders from POSITAL were approved to meet the requirements of the ATEX/IECEx guidelines for Category 3 electrical equipment. These tools are perfect for oil and gas installations, chemical plants, woodworking activities, and grain handling facilities, as they may be used in Zone 2 and Zone 22 conditions (possible exposure to dangerous quantities of explosive gases and combustible dust).

Encoder Market Leaders

Omron Corporation

Honeywell International

Schneider Electric

Rockwell Automation Inc.

Panasonic Corporation

*Disclaimer: Major Players sorted in no particular order

Encoder Market News

- November 2022: Maxon announced the launch of five new products at the upcoming SPS trade fair in Nuremberg. They include the ECX SPEED 8 motors with pin connection, the integrated ENX 32 MILE encoder for drives from the ECX flat motor series with 32 mm diameter, and the powerful IDX 56 and 70 industrial drives.

- September 2022: Celera Motion, a motion control business of Novanta Inc., expanded its robot arm encoder range. The company launched its new encodes with various diameters to enable accurate angular measurement across virtually all types of robot joints. The new encoder range would cover all the typical sizes required in arms, from small end effectors at the end of the arm to the upper shoulder joints. Celera Motion’s range of Aura series rotary encoders can be used by various OEMs designing applications, such as surgical robots, robot joints, grippers, cobots, exoskeletons and wearables, and semiconductors.

Encoder Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 High Adoption in Advanced Automotive Systems

5.1.2 Rising Demand For Industrial Automation

5.2 Market Challenges

5.2.1 Mechanical Failures in Harsh Conditions

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 Rotary Encoder

6.1.2 Linear Encoder

6.2 By Technology

6.2.1 Optical

6.2.2 Magnetic

6.2.3 Photoelectric

6.2.4 Other Technologies

6.3 By End-user Industry

6.3.1 Automotive

6.3.2 Electronics

6.3.3 Textile

6.3.4 Printing Machinery

6.3.5 Industrial

6.3.6 Medical

6.3.7 Other End-user Industries

6.4 By Geography

6.4.1 North America

6.4.2 Europe

6.4.3 Asia-Pacific

6.4.4 Rest of the World (Latin America and Middle East and Africa)

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Omron Corporation

7.1.2 Honeywell International

7.1.3 Schneider Electric

7.1.4 Rockwell Automation Inc.

7.1.5 Panasonic Corporation

7.1.6 Baumer Group

7.1.7 Renishaw PLC

7.1.8 Dynapar Corporation (Fortive Corporation)

7.1.9 FAULHABER Drive Systems

7.1.10 Pepperl+Fuchs International

7.1.11 Hengstler GMBH (Fortive Corporation)

7.1.12 Maxon Motor AG

7.1.13 Dr. Johannes Heidenhain GmbH

7.1.14 POSITAL FRABA Inc. (FRABA BV)

7.1.15 Sensata Technologies

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OUTLOOK OF THE MARKET

Encoder Industry Segmentation

Encoders are components that are added to a direct current motor to convert the mechanical motion into digital pulses that can be interpreted by integrated control electronics. The main purpose of encoders is to transform information from one format to another for standardization, speed adjustment, or safety control.

The encoder market is segmented by type (rotary and linear), technology (optical, magnetic, and photoelectric), end-user industry (automotive, electronics, textile, printing machinery, industrial, and medical), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Type | |

| Rotary Encoder | |

| Linear Encoder |

| By Technology | |

| Optical | |

| Magnetic | |

| Photoelectric | |

| Other Technologies |

| By End-user Industry | |

| Automotive | |

| Electronics | |

| Textile | |

| Printing Machinery | |

| Industrial | |

| Medical | |

| Other End-user Industries |

| By Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Rest of the World (Latin America and Middle East and Africa) |

Encoder Market Research FAQs

How big is the Encoder Market?

The Encoder Market size is expected to reach USD 2.65 billion in 2023 and grow at a CAGR of 7.72% to reach USD 3.85 billion by 2028.

What is the current Encoder Market size?

In 2023, the Encoder Market size is expected to reach USD 2.65 billion.

Who are the key players in Encoder Market?

Omron Corporation, Honeywell International, Schneider Electric, Rockwell Automation Inc. and Panasonic Corporation are the major companies operating in the Encoder Market.

Which is the fastest growing region in Encoder Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2027).

Which region has the biggest share in Encoder Market?

In 2023, the Asia-Pacific accounts for the largest market share in the Encoder Market.

Encoder Industry Report

Statistics for the 2023 Encoder market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Encoder analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.