Europe Crop Protection Chemicals Market Size

| Study Period | 2018 - 2028 |

| Base Year For Estimation | 2022 |

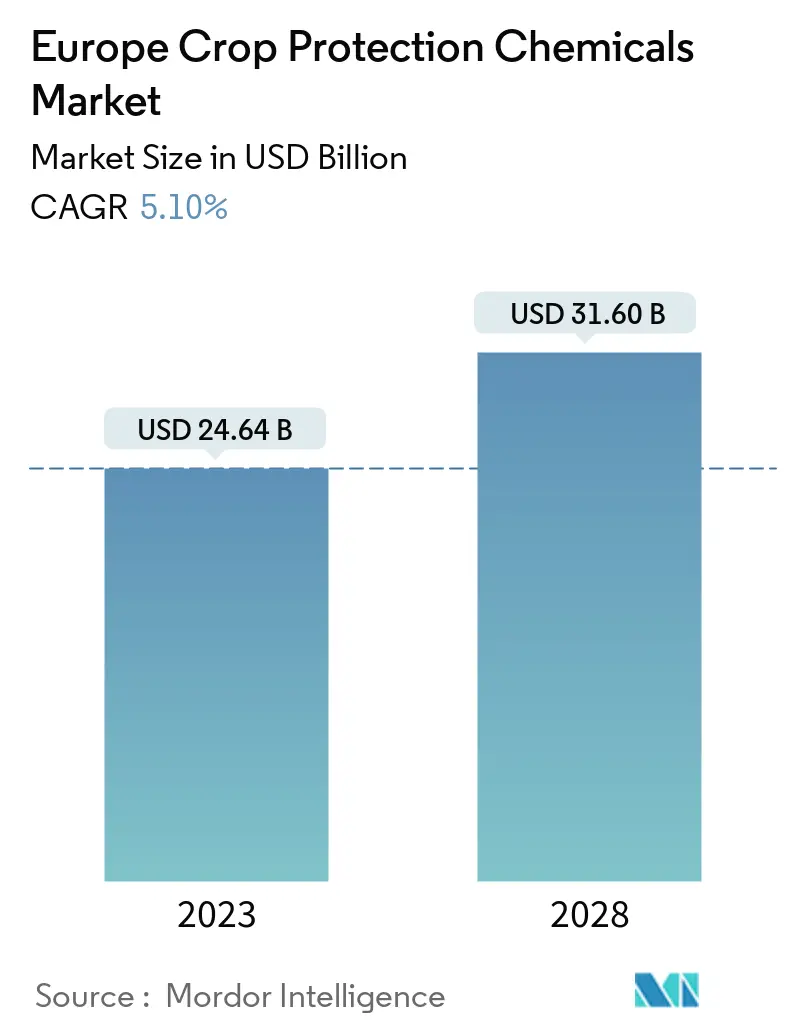

| Market Size (2023) | USD 24.64 Billion |

| Market Size (2028) | USD 31.60 Billion |

| CAGR (2023 - 2028) | 5.10 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Europe Crop Protection Chemicals Market Analysis

The Europe Crop Protection Chemicals Market size is expected to grow from USD 24.64 billion in 2023 to USD 31.60 billion by 2028, at a CAGR of 5.10% during the forecast period (2023-2028).

- Europe's crop protection chemicals market is driven by the need to increase crop yield and efficiency. The region's population is drastically growing, but the farmlands are diminishing. As a result, it is pushing farmers to increase their yield. Therefore, new farming practices are being adopted by farmers to increase crop yield, which is paving the way for the crop protection market.

- Using pesticides over crops is a proven technology to increase global food production. New farming practices require new crop protection products, but the research and development costs are escalating as many pesticides are banned in this region. The costs to register new pesticides for sale are high in these countries. These factors are driving the bio-based market to grow in the region during the forecasting period.

- In 2022, European Commission adopted its proposal for a new regulation on the sustainable use of Plant Protection Products (SUR). The rules encourage reducing pesticides through integrated pest management and alternatives to chemical pesticides. The Plant Protection Products (SUR) is considered a crucial tool for achieving the targets outlined in the European Green Deal and the Farm to Fork Strategy, as it puts forward legally binding pesticide reduction targets to reduce the use and risk of chemical pesticides by 50% by 2030. The proposal is part of the Commission's nature restoration package, including a proposal to restore damaged ecosystems and bring nature back across Europe.

- Increased awareness, advances in farming practices, and technology are reasons for Europe to hold a significant market share in crop protection. According to Eurostat, fungicides and bactericides accounted for more than 45% of the total pesticide sales in the region in 2020, which will drive the fungicides segment in the region in coming years.

Europe Crop Protection Chemicals Market Trends

Growing Organic Food Consumption is Driving Biopesticides

- Biopesticide adoption is occurring all over the region, especially in developed and some developing countries. The ban on using various pesticides such as glyphosate, neonicotinoids, and paraquat is expected to drive the demand for biopesticides in the region. Currently, Europe is the second-largest market for biopesticides globally. Demand for organic and completely natural foods is increasing stably, and biopesticide consumption has inevitably been under various improvisations.

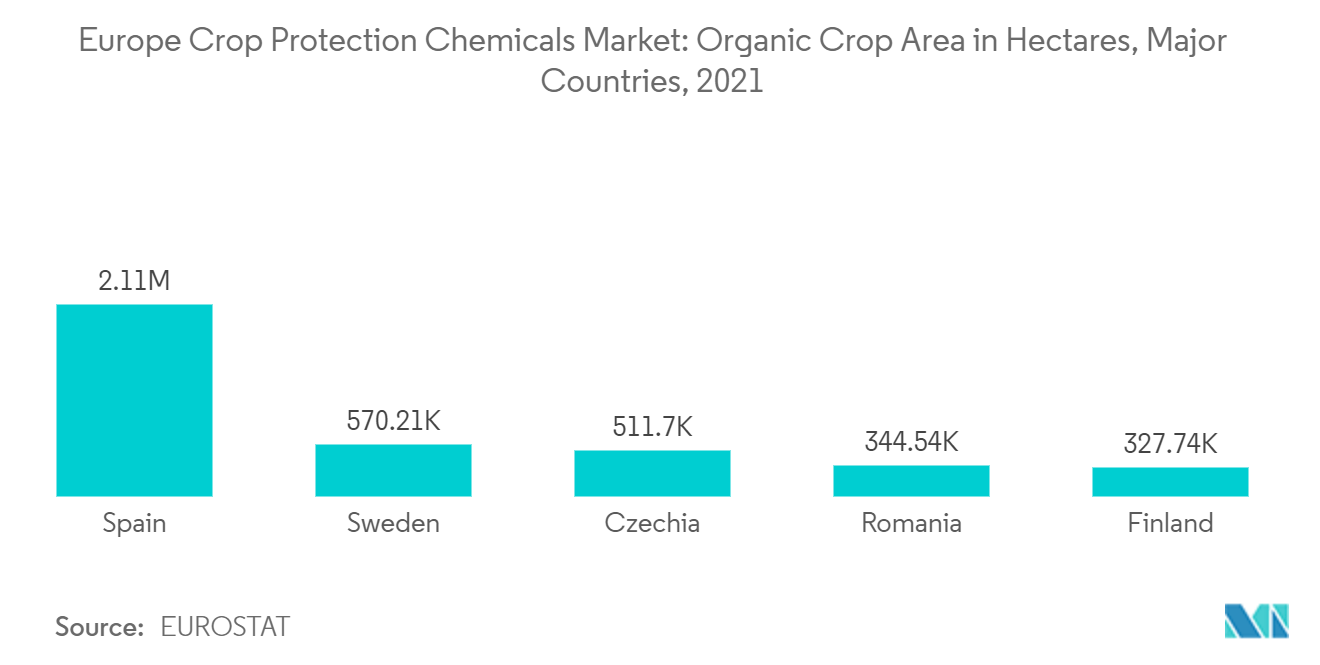

- According to Eurostat, Spain was the largest country in the region in 2021, with 2.1 million hectares of organic crop area, followed by Sweden. Countries such as Spain, Sweden, and Czhezia were the largest utilizers of biopesticides because of the higher organic cultivation area in these countries in 2021, which is expected to drive the market in the region during the forecast period.

- Pesticides help in the optimal usage of resources for plant growth and protect the crop from various pathogens. Some pesticides repel animals coming towards them with the help of pheromones. Biopesticides are regulated in the European Union in the same manner as chemical pesticides. The Organization for Economic Co-operation and Development (OECD), a 34-country group headquartered in Paris, France, assists EU governments in quickly and thoroughly assessing biopesticide risks to humans and the environment.

- In Europe and other advanced countries, there are limits on residue levels present in food. However, no such limits usually exist for most biopesticides due to their comparative safety. Quicker access for farmers to innovative and new technologies such as precision and digital tools, as well as increased use of biopesticides, is expected to drive the market in the following years.

Fungicides is Largest Market in the Region

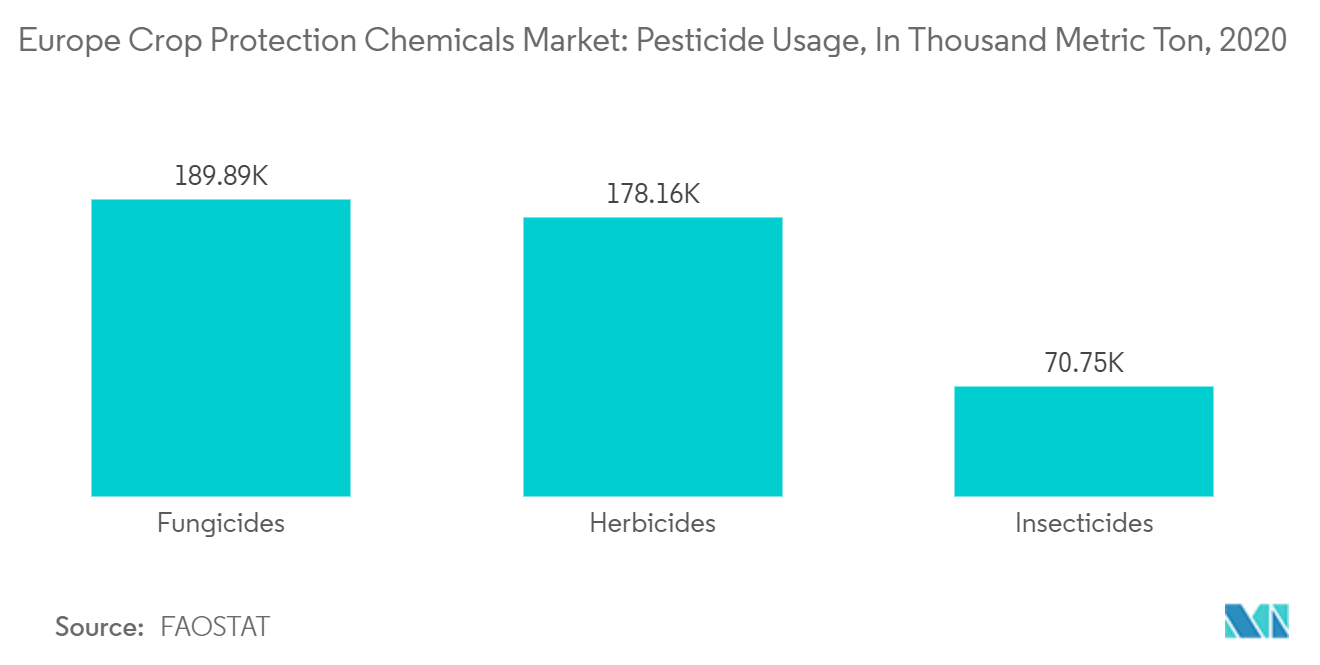

- Chemicals kill or halt the development of fungi that cause plant diseases, such as storage rot; seedling diseases; root rots; vascular wilts; leaf blights, rusts, smuts and mildews, and viral diseases. These can be controlled by the early and continued application of selected fungicides that either kill the pathogens or restrict their development. According to Food and Agriculture Organization Corporate Statistical Database (FAOSTAT), fungicides are the most used segment of the pesticides in the region, with 189,888 metric tons in 2020, which is higher than the previous year, followed by herbicides and insecticides.

- Annual sales of pesticides in the European Union (EU) amounted to almost 360,000 metric tons in 2021, with a 46% share of fungicides as the most sold group. Even with the deployment of resistant cultivars and integrated control strategies, fungicides still contribute heavily to plant disease control in conventional farming. Even organic systems, although promoted for environmental benefits, depend on fungicides. In these systems, the amounts applied are sometimes high to compensate for lower efficacy.

- Recently, new fungal plant diseases have emerged worldwide associated with the globalization of trade and environmental change, thus further increasing farmers’ dependency on fungicides. Nevertheless, their use in agriculture has been associated with growing environmental and public health concerns. In addition to their negative environmental impacts (e.g., on biodiversity), some fungicides have been associated with increased risk to human health, particularly among farmers. And also among people living in agricultural areas. However, the use is expected to grow in the coming years to avoid crop damage.

- One of the most commonly used fungicides in the world, considered by farmers as crucial for resistance management, is no longer approved as an active substance in the EU. The ban on mancozeb was first proposed by the European Commission early in 2020. Many imported products may be affected by MRL reductions because mancozeb is a key pesticide in the production of crops such as bananas, cranberries, and vegetables. Despite the EU clampdown on pesticides, France has approved three years of seeds coated with neonicotinoid insecticides, which are thought harmful to bees. Hence, many major players are innovating new products, fungicides, which are more useful in eradicating diseases and resulting in better performance than bio-based products in the country.

Europe Crop Protection Chemicals Industry Overview

The Europe crop protection chemicals market is highly consolidated. The major companies include Bayer CropScience AG, BASF SE, Syngenta International AG, Corteva AgriSciences, and UPL Limited, accounting for more than 50% of the market share. The research and innovation route is the current trend to survive in the market. All major companies invest profoundly in new product development to keep up with the competition and gain market share.

Europe Crop Protection Chemicals Market Leaders

Bayer CropScience AG

Syngenta International AG

Corteva Agri Science

BASF SE

UPL Limited

*Disclaimer: Major Players sorted in no particular order

Europe Crop Protection Chemicals Market News

- December 2022: BASF Agricultural Solutions started to convert its product packaging for liquid crop protection products in the first European countries (France, Germany, and Netherlands) to enable the easy-to-connect closed transfer system (CTS). A new generation of filling methods will make farm operations safer for users and the environment.

- January 2022: Syngenta Crop Protection acquired two next-generation bioinsecticides, NemaTrident and UniSpore, to combat increasing resistance and a wide range of insects and pests across horticulture and ornamentals, turf amenity, and forestry where growers across Europe have limited insecticide options.

- June 2021: UPL has launched a new business unit, Natural Plant Protection (NPP), to enhance the bio solutions offering at a global level quickly. This new business unit was included with all the company's natural and biologically derived inputs and technologies.

Europe Crop Protection Chemicals Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Origin

5.1.1 Synthetic

5.1.2 Bio-based

5.2 Type

5.2.1 Herbicide

5.2.2 Fungicide

5.2.3 Insecticide

5.2.4 Nematicide

5.2.5 Molluscicide

5.2.6 Other Types

5.3 Application

5.3.1 Grains and Cereals

5.3.2 Pulses and Oilseeds

5.3.3 Fruits and Vegetables

5.3.4 Commercial Crops

5.3.5 Other Applications

5.4 Geography

5.4.1 Europe

5.4.1.1 Germany

5.4.1.2 Italy

5.4.1.3 United Kingdom

5.4.1.4 France

5.4.1.5 Russia

5.4.1.6 Spain

5.4.1.7 Rest of Europe

6. COMPETITIVE LANDSCAPE

6.1 Most Adopted Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 Syngenta International AG

6.3.2 BASF SE

6.3.3 Corteva AgriSciences

6.3.4 UPL Limited

6.3.5 Bayer CropScience AG

6.3.6 Adama Agricultural Solutions Ltd

6.3.7 Huapont Life Sciences

6.3.8 FMC Corporation

6.3.9 Nufarm Ltd

6.3.10 Sumitomo Chemicals

6.3.11 AGRO International Ltd

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Europe Crop Protection Chemicals Industry Segmentation

Crop protection chemicals, also called pesticides, constitute a class of agrochemicals used to kill plant-harming organisms, like pests, weeds, rodents, nematodes, etc.,and prevent the destruction of crops.

The Europe crop protection chemicals market is segmented by origin (synthetic, bio-based), type (herbicides, insecticides, fungicides, nematicides, other types), application (grains and cereals, pulses and oilseeds, commercial crops, fruits and vegetables, other applications), and geography (Europe (Germany, Italy, United Kingdom, France, Russia, Spain) and Rest of Europe).

The report also offers the market sizing in terms of value (USD million).

| Origin | |

| Synthetic | |

| Bio-based |

| Type | |

| Herbicide | |

| Fungicide | |

| Insecticide | |

| Nematicide | |

| Molluscicide | |

| Other Types |

| Application | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Fruits and Vegetables | |

| Commercial Crops | |

| Other Applications |

| Geography | |||||||||

|

Europe Crop Protection Chemicals Market Research FAQs

How big is the Europe Crop Protection Chemicals Market?

The Europe Crop Protection Chemicals Market size is expected to reach USD 24.64 billion in 2023 and grow at a CAGR of 5.10% to reach USD 31.60 billion by 2028.

What is the current Europe Crop Protection Chemicals Market size?

In 2023, the Europe Crop Protection Chemicals Market size is expected to reach USD 24.64 billion.

Who are the key players in Europe Crop Protection Chemicals Market?

Bayer CropScience AG, Syngenta International AG, Corteva Agri Science, BASF SE and UPL Limited are the major companies operating in the Europe Crop Protection Chemicals Market.

Europe Crop Protection Chemicals Industry Report

Statistics for the 2023 Europe Crop Protection Chemicals market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Europe Crop Protection Chemicals analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.