Europe Military Aviation Market Size

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2016 - 2028 |

|

|

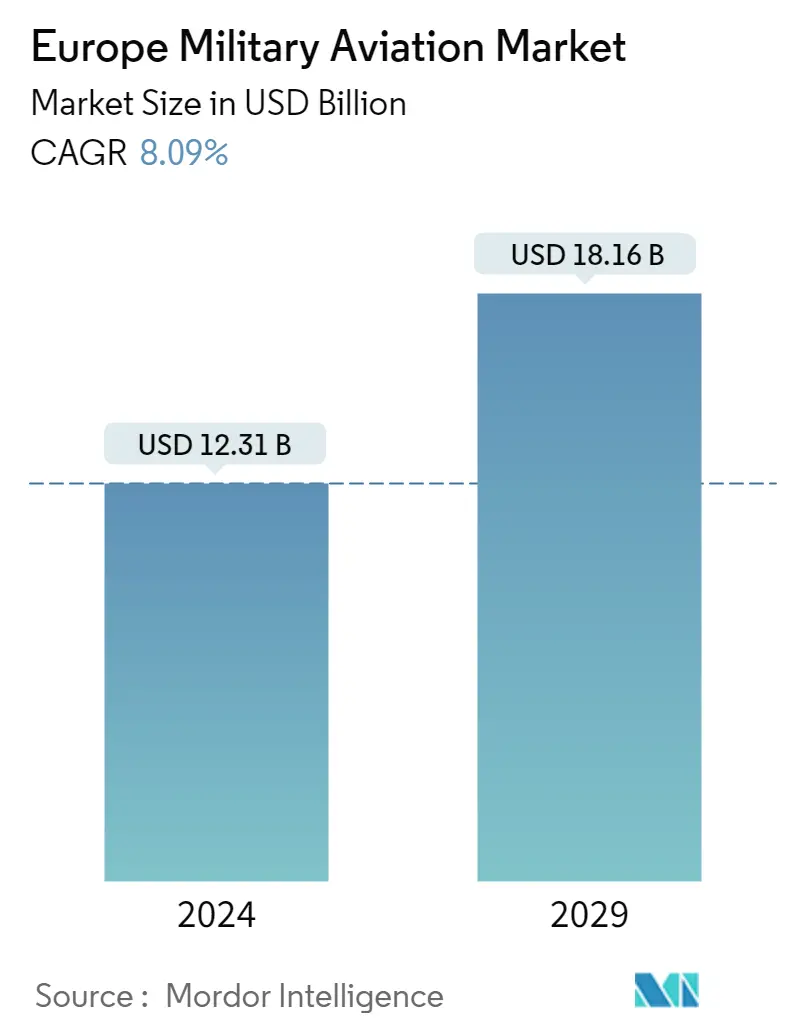

Market Size (2023) | USD 12.30 Billion |

|

|

Market Size (2028) | USD 18.16 Billion |

|

|

CAGR (2023 - 2028) | 8.10 % |

|

|

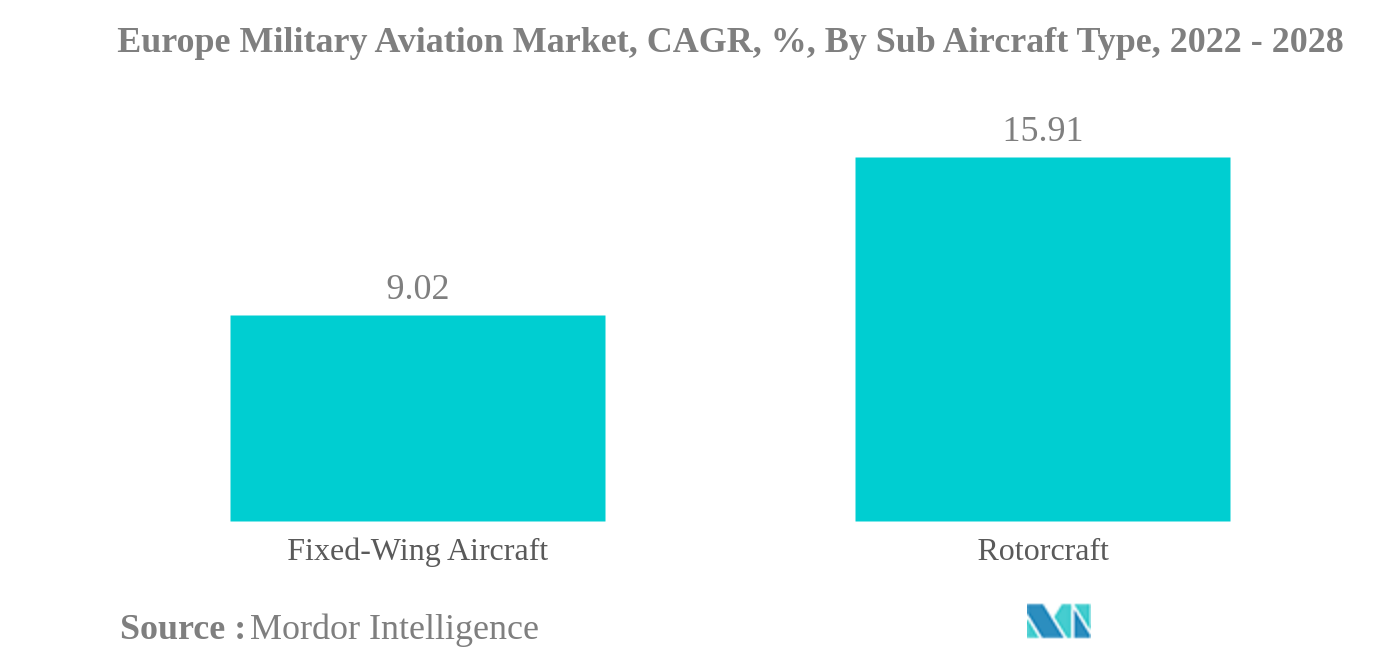

Largest Share by Sub Aircraft Type | Fixed-Wing Aircraft |

|

|

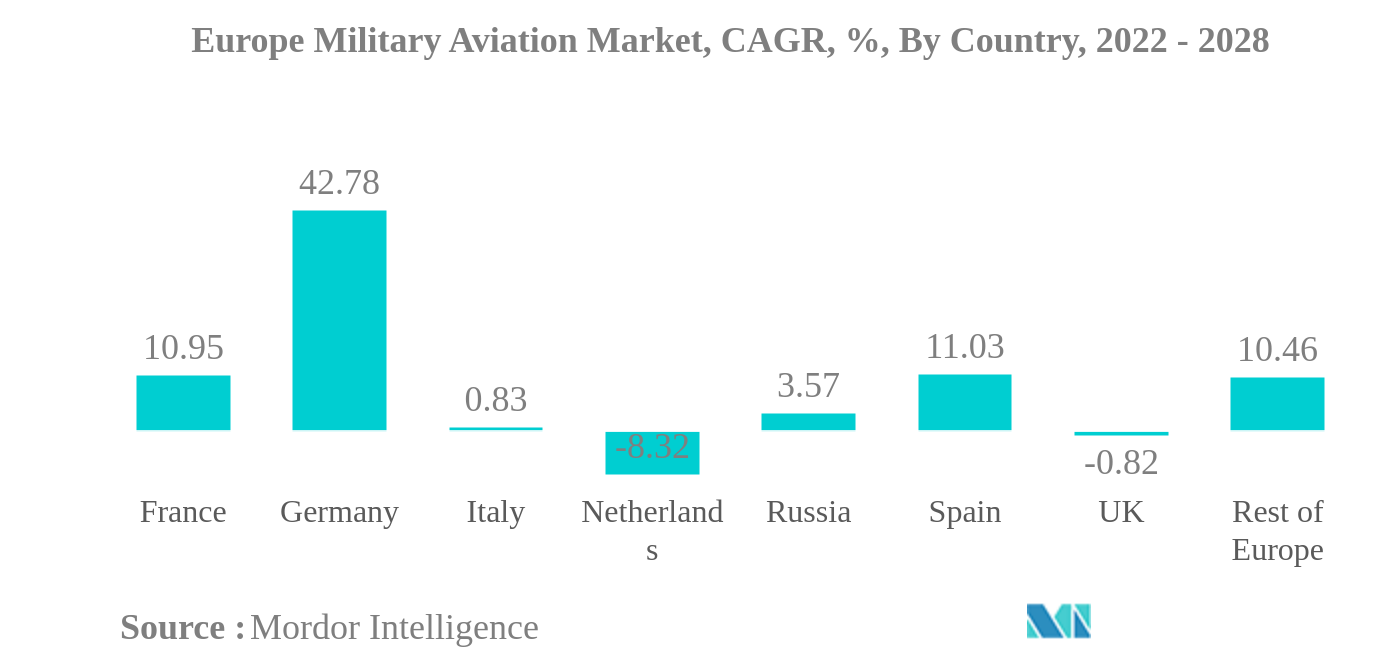

Largest Share by Country | France |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Europe Military Aviation Market Analysis

The Europe Military Aviation Market size is expected to grow from USD 12.30 billion in 2023 to USD 18.16 billion by 2028, at a CAGR of 8.10% during the forecast period (2023-2028).

- Largest Market by Sub-Aircraft Type - Fixed-Wing Aircraft : The countries' aim to meet the NATO standards in defense spending is driving the fixed-wing aircraft market growth in the region.

- Fastest-growing Market by Sub-Aircraft Type - Rotorcraft : The countries' aim to meet the NATO standards in defense spending is driving the rotorcraft market growth in the region.

- Largest Market by Body Type - Multi-Role Aircraft : Countries in the region are opting for multi-role aircraft to perform ground strikes, air superiority, and suppress the enemy air defenses.

- Largest Market by Country - France : The country's six-year defense spending framework is being adjusted and increased according to the current geopolitical situation to counter the threats.

Europe Military Aviation Market Trends

This section covers the major market trends shaping the Europe Military Aviation Market according to our research experts:

Fixed-Wing Aircraft is the largest Sub Aircraft Type

- The defense expenditure of the European region surged by around 3% during 2020-2021, to USD 415 billion in 2021. Military R&D and weaponry purchases accounted for most of the rise in defense expenditure in Europe.

- The Russia-Ukraine conflict became the center stage in Europe in 2022. The armed conflict worsened in March and April 2021, when Russia deployed thousands of additional troops on the border with Ukraine. In February 2022, a full-fledged war started between the two countries. By the end of March 2022, numerous European NATO member nations had announced plans to increase military expenditures in reaction to the Russian-Ukraine war, aiming to meet or exceed the NATO spending target of 2% of the GDP or higher.

- In total, 26 of the 27 European NATO nations had available financing for their armed forces in 2021. The SIPRI Military Expenditure Database shows that, among the 26 countries, eight spent at least 2% of their GDP on the military in 2021, a decrease from 9 in 2020.

- In the fixed-wing segment, 40 procurements of Rafale fighter jets by France, 74 F-35 fighter jets by the UK worth USD 4.5 billion, and 15 Eurofighter jets and up to 35 US-made F-35 fighter jets by Germany are some of the major contracts that took place in the region during 2016-2021. In the rotorcraft segment, a total of 901 helicopters are expected to be delivered in the region during the forecast period.

France is the largest Country

- The defense expenditure of the European region surged around 3% during 2020-2021, to USD 415 billion in 2021. Military R&D and weaponry purchases accounted for most of Europe's defense expenditure rise.

- The Russia-Ukraine conflict became the center stage in Europe in 2022. After festering at a lower level for months, the armed conflict worsened again in March and April 2021 when Russia deployed thousands of additional troops sideways the border with Ukraine. In February 2022, a full-fledged war started between the two countries. By the end of March 2022, numerous European NATO member nations had announced plans to increase military expenditures in reaction to the Russian-Ukraine war in February 2022, aiming to meet or exceed the NATO spending target of 2% of GDP or higher.

- In total, 26 of the 27 European NATO nations will have financing available for their armed forces in 2021. The SIPRI Military Expenditure Database shows that, among the 26 countries, 8 spent at least 2% of their GDP on the military in 2021, a decrease from 9 in 2020.

- The major procurements, such as 40 Rafale fighter jets by France, the procurement of 74 F-35 fighter jets by the UK worth USD 4.5 billion, and the procurement of 15 Eurofighter jets and up to 35 US-made F-35 fighter jets by Germany are some of the major contracts that happened in the region during 2016-2021. The active aircraft fleet will increase in the region as countries like Germany, France, Italy, and the UK are expected to procure new aircraft for fleet expansion during the forecast period.

Europe Military Aviation Industry Overview

The Europe Military Aviation Market is fairly consolidated, with the top five companies occupying 91.20%. The major players in this market are Airbus SE, Dassault Aviation, Lockheed Martin Corporation, Russian Helicopters and United Aircraft Corporation (sorted alphabetically).

Europe Military Aviation Market Leaders

Airbus SE

Dassault Aviation

Lockheed Martin Corporation

Russian Helicopters

United Aircraft Corporation

*Disclaimer: Major Players sorted in no particular order

Europe Military Aviation Market News

- June 2022: Lockheed Martin and Korea Aerospace Industries (KAI) have signed a teaming agreement to explore future opportunities for the T-50 advanced jet trainer. As part of the agreement, KAI and Lockheed Martin will offer T-50s for training aircraft programs worldwide.

- March 2022: Airbus Helicopters has been awarded a contract by OCCAR (Organisation for Joint Armament Cooperation) on behalf of the French and Spanish Armament General Directorates, the DGA and the DGAM for the development, production, and initial in-service support of the Tiger MkIII attack helicopter upgrade programme.

- January 2022: In January 2022, Airbus Helicopters announced that it had received orders for 30 H160M helicopters from the French armed forces taking the total order to 169. Also, the OEM received orders for 36 H135 helicopters from the Spanish Ministries of Defence and Interior.

Europe Military Aviation Market Report - Table of Contents

1. INTRODUCTION

1.1. Study Assumptions & Market Definition

1.2. Scope of the Study

1.3. Research Methodology

2. KEY INDUSTRY TRENDS

2.1. Gross Domestic Product

2.2. Active Fleet Data

2.3. Defense Spending

2.4. Regulatory Framework

2.5. Value Chain Analysis

3. MARKET SEGMENTATION

3.1. Sub Aircraft Type

3.1.1. Fixed-Wing Aircraft

3.1.1.1. Multi-Role Aircraft

3.1.1.2. Training Aircraft

3.1.1.3. Transport Aircraft

3.1.1.4. Others

3.1.2. Rotorcraft

3.1.2.1. Multi-Mission Helicopter

3.1.2.2. Transport Helicopter

3.1.2.3. Others

3.2. Country

3.2.1. France

3.2.2. Germany

3.2.3. Italy

3.2.4. Netherlands

3.2.5. Russia

3.2.6. Spain

3.2.7. UK

3.2.8. Rest Of Europe

4. COMPETITIVE LANDSCAPE

4.1. Key Strategic Moves

4.2. Market Share Analysis

4.3. Company Landscape

4.4. Company Profiles

4.4.1. Airbus SE

4.4.2. ATR

4.4.3. Dassault Aviation

4.4.4. Hughes Helicopters

4.4.5. Leonardo S.p.A

4.4.6. Lockheed Martin Corporation

4.4.7. MD Helicopters LLC.

4.4.8. Pilatus Aircraft Ltd

4.4.9. Russian Helicopters

4.4.10. Textron Inc.

4.4.11. The Boeing Company

4.4.12. United Aircraft Corporation

5. KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

6. APPENDIX

6.1. Global Overview

6.1.1. Overview

6.1.2. Porter’s Five Forces Framework

6.1.3. Global Value Chain Analysis

6.1.4. Market Dynamics (DROs)

6.2. Sources & References

6.3. List of Tables & Figures

6.4. Primary Insights

6.5. Data Pack

6.6. Glossary of Terms

List of Tables & Figures

- Figure 1:

- EUROPE MILITARY AVIATION MARKET, GROSS DOMESTIC PRODUCT, VALUE, USD, 2016 – 2028

- Figure 2:

- EUROPE MILITARY AVIATION MARKET, ACTIVE FLEET DATA, NUMBER OF AIRCRAFT, 2016 – 2028

- Figure 3:

- EUROPE MILITARY AVIATION MARKET, DEFENSE SPENDING, VALUE, USD, 2016 – 2028

- Figure 4:

- EUROPE MILITARY AVIATION MARKET, VOLUME, UNITS, 2016 - 2028

- Figure 5:

- EUROPE MILITARY AVIATION MARKET, VALUE, USD, 2016 - 2028

- Figure 6:

- EUROPE MILITARY AVIATION MARKET, BY SUB AIRCRAFT TYPE, VOLUME, UNITS, 2016 - 2028

- Figure 7:

- EUROPE MILITARY AVIATION MARKET, BY SUB AIRCRAFT TYPE, VALUE, USD, 2016 - 2028

- Figure 8:

- EUROPE MILITARY AVIATION MARKET, BY SUB AIRCRAFT TYPE, VOLUME, %, 2016 VS 2022 VS 2028

- Figure 9:

- EUROPE MILITARY AVIATION MARKET, BY SUB AIRCRAFT TYPE, VALUE, %, 2016 VS 2022 VS 2028

- Figure 10:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VOLUME, UNITS, 2016 - 2028

- Figure 11:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VALUE, USD, 2016 - 2028

- Figure 12:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VOLUME, %, 2016 VS 2022 VS 2028

- Figure 13:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VALUE, %, 2016 VS 2022 VS 2028

- Figure 14:

- EUROPE MILITARY AVIATION MARKET, BY MULTI-ROLE AIRCRAFT, VOLUME, UNITS, 2016 - 2028

- Figure 15:

- EUROPE MILITARY AVIATION MARKET, BY MULTI-ROLE AIRCRAFT, VALUE, USD, 2016 - 2028

- Figure 16:

- EUROPE MILITARY AVIATION MARKET, BY MULTI-ROLE AIRCRAFT, VALUE, %, 2021 VS 2028

- Figure 17:

- EUROPE MILITARY AVIATION MARKET, BY TRAINING AIRCRAFT, VOLUME, UNITS, 2016 - 2028

- Figure 18:

- EUROPE MILITARY AVIATION MARKET, BY TRAINING AIRCRAFT, VALUE, USD, 2016 - 2028

- Figure 19:

- EUROPE MILITARY AVIATION MARKET, BY TRAINING AIRCRAFT, VALUE, %, 2021 VS 2028

- Figure 20:

- EUROPE MILITARY AVIATION MARKET, BY TRANSPORT AIRCRAFT, VOLUME, UNITS, 2016 - 2028

- Figure 21:

- EUROPE MILITARY AVIATION MARKET, BY TRANSPORT AIRCRAFT, VALUE, USD, 2016 - 2028

- Figure 22:

- EUROPE MILITARY AVIATION MARKET, BY TRANSPORT AIRCRAFT, VALUE, %, 2021 VS 2028

- Figure 23:

- EUROPE MILITARY AVIATION MARKET, BY OTHERS, VOLUME, UNITS, 2016 - 2028

- Figure 24:

- EUROPE MILITARY AVIATION MARKET, BY OTHERS, VALUE, USD, 2016 - 2028

- Figure 25:

- EUROPE MILITARY AVIATION MARKET, BY OTHERS, VALUE, %, 2021 VS 2028

- Figure 26:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VOLUME, UNITS, 2016 - 2028

- Figure 27:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VALUE, USD, 2016 - 2028

- Figure 28:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VOLUME, %, 2016 VS 2022 VS 2028

- Figure 29:

- EUROPE MILITARY AVIATION MARKET, BY BODY TYPE, VALUE, %, 2016 VS 2022 VS 2028

- Figure 30:

- EUROPE MILITARY AVIATION MARKET, BY MULTI-MISSION HELICOPTER, VOLUME, UNITS, 2016 - 2028

- Figure 31:

- EUROPE MILITARY AVIATION MARKET, BY MULTI-MISSION HELICOPTER, VALUE, USD, 2016 - 2028

- Figure 32:

- EUROPE MILITARY AVIATION MARKET, BY MULTI-MISSION HELICOPTER, VALUE, %, 2021 VS 2028

- Figure 33:

- EUROPE MILITARY AVIATION MARKET, BY TRANSPORT HELICOPTER, VOLUME, UNITS, 2016 - 2028

- Figure 34:

- EUROPE MILITARY AVIATION MARKET, BY TRANSPORT HELICOPTER, VALUE, USD, 2016 - 2028

- Figure 35:

- EUROPE MILITARY AVIATION MARKET, BY TRANSPORT HELICOPTER, VALUE, %, 2021 VS 2028

- Figure 36:

- EUROPE MILITARY AVIATION MARKET, BY OTHERS, VOLUME, UNITS, 2016 - 2028

- Figure 37:

- EUROPE MILITARY AVIATION MARKET, BY OTHERS, VALUE, USD, 2016 - 2028

- Figure 38:

- EUROPE MILITARY AVIATION MARKET, BY OTHERS, VALUE, %, 2021 VS 2028

- Figure 39:

- EUROPE MILITARY AVIATION MARKET, BY COUNTRY, VOLUME, UNITS, 2016 - 2028

- Figure 40:

- EUROPE MILITARY AVIATION MARKET, BY COUNTRY, VALUE, USD, 2016 - 2028

- Figure 41:

- EUROPE MILITARY AVIATION MARKET, BY COUNTRY, VOLUME, %, 2016 VS 2022 VS 2028

- Figure 42:

- EUROPE MILITARY AVIATION MARKET, BY COUNTRY, VALUE, %, 2016 VS 2022 VS 2028

- Figure 43:

- EUROPE MILITARY AVIATION MARKET, BY FRANCE, VOLUME, UNITS, 2016 - 2028

- Figure 44:

- EUROPE MILITARY AVIATION MARKET, BY FRANCE, VALUE, USD, 2016 - 2028

- Figure 45:

- EUROPE MILITARY AVIATION MARKET, BY FRANCE, VALUE, %, 2021 VS 2028

- Figure 46:

- EUROPE MILITARY AVIATION MARKET, BY GERMANY, VOLUME, UNITS, 2016 - 2028

- Figure 47:

- EUROPE MILITARY AVIATION MARKET, BY GERMANY, VALUE, USD, 2016 - 2028

- Figure 48:

- EUROPE MILITARY AVIATION MARKET, BY GERMANY, VALUE, %, 2021 VS 2028

- Figure 49:

- EUROPE MILITARY AVIATION MARKET, BY ITALY, VOLUME, UNITS, 2016 - 2028

- Figure 50:

- EUROPE MILITARY AVIATION MARKET, BY ITALY, VALUE, USD, 2016 - 2028

- Figure 51:

- EUROPE MILITARY AVIATION MARKET, BY ITALY, VALUE, %, 2021 VS 2028

- Figure 52:

- EUROPE MILITARY AVIATION MARKET, BY NETHERLANDS, VOLUME, UNITS, 2016 - 2028

- Figure 53:

- EUROPE MILITARY AVIATION MARKET, BY NETHERLANDS, VALUE, USD, 2016 - 2028

- Figure 54:

- EUROPE MILITARY AVIATION MARKET, BY NETHERLANDS, VALUE, %, 2021 VS 2028

- Figure 55:

- EUROPE MILITARY AVIATION MARKET, BY RUSSIA, VOLUME, UNITS, 2016 - 2028

- Figure 56:

- EUROPE MILITARY AVIATION MARKET, BY RUSSIA, VALUE, USD, 2016 - 2028

- Figure 57:

- EUROPE MILITARY AVIATION MARKET, BY RUSSIA, VALUE, %, 2021 VS 2028

- Figure 58:

- EUROPE MILITARY AVIATION MARKET, BY SPAIN, VOLUME, UNITS, 2016 - 2028

- Figure 59:

- EUROPE MILITARY AVIATION MARKET, BY SPAIN, VALUE, USD, 2016 - 2028

- Figure 60:

- EUROPE MILITARY AVIATION MARKET, BY SPAIN, VALUE, %, 2021 VS 2028

- Figure 61:

- EUROPE MILITARY AVIATION MARKET, BY UK, VOLUME, UNITS, 2016 - 2028

- Figure 62:

- EUROPE MILITARY AVIATION MARKET, BY UK, VALUE, USD, 2016 - 2028

- Figure 63:

- EUROPE MILITARY AVIATION MARKET, BY UK, VALUE, %, 2021 VS 2028

- Figure 64:

- EUROPE MILITARY AVIATION MARKET, BY REST OF EUROPE, VOLUME, UNITS, 2016 - 2028

- Figure 65:

- EUROPE MILITARY AVIATION MARKET, BY REST OF EUROPE, VALUE, USD, 2016 - 2028

- Figure 66:

- EUROPE MILITARY AVIATION MARKET, BY REST OF EUROPE, VALUE, %, 2021 VS 2028

- Figure 67:

- EUROPE MILITARY AVIATION MARKET, MOST ACTIVE COMPANIES, BY NUMBER OF STRATEGIC MOVES, 2018 - 2021

- Figure 68:

- EUROPE MILITARY AVIATION MARKET, MOST ADOPTED STRATEGIES, 2018 - 2021

- Figure 69:

- EUROPE MILITARY AVIATION MARKET SHARE(%), BY MAJOR PLAYERS, 2021

Europe Military Aviation Industry Segmentation

Fixed-Wing Aircraft, Rotorcraft are covered as segments by Sub Aircraft Type. France, Germany, Italy, Netherlands, Russia, Spain, UK are covered as segments by Country.| Sub Aircraft Type | ||||||

| ||||||

|

| Country | |

| France | |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| UK | |

| Rest Of Europe |

Market Definition

- Aircraft Type - All the military aircraft and rotorcraft which are used for various applications are included in this study.

- Body Type - Multi-Role Aircraft, Transport, Training Aircraft, Bombers, Reconnaissance Aircraft, Multi-Mission Helicopters, Transport Helicopters and various other aircraft and rotorcraft are considered in this study.

- Sub-Aircraft Type - For this study, sub-aircraft types such as fixed-wing aircraft and rotorcraft based on their application are considered.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms