Functional Safety Market Size

| Study Period | 2018 - 2028 |

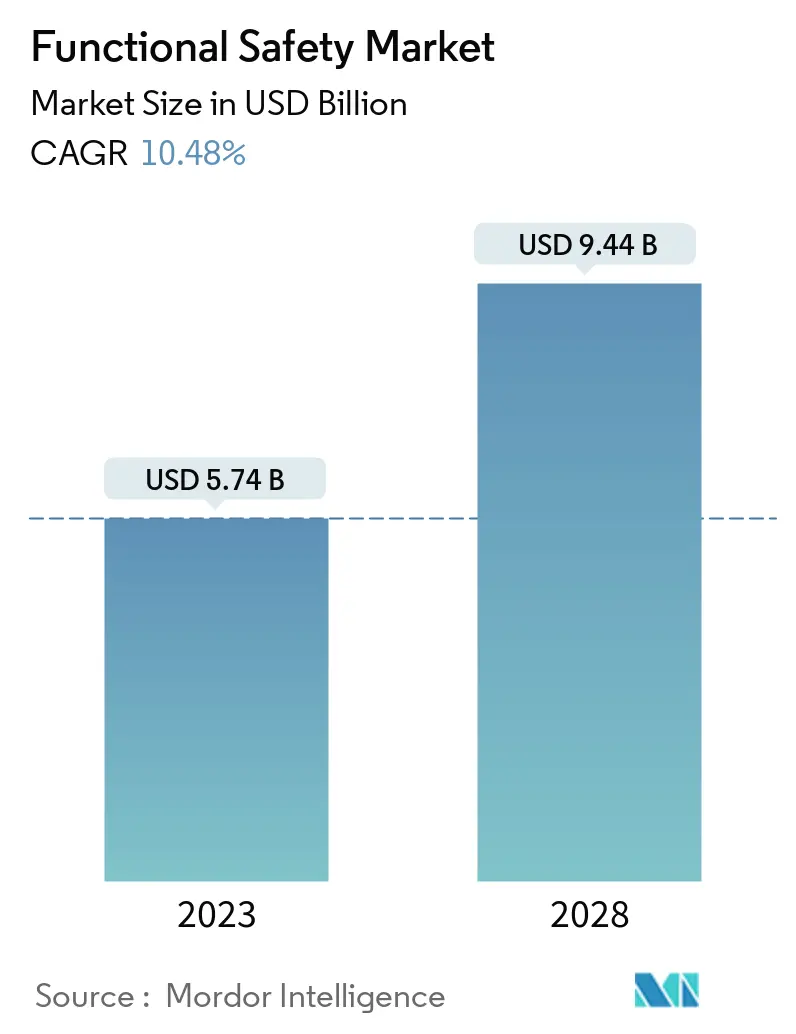

| Market Size (2023) | USD 5.74 Billion |

| Market Size (2028) | USD 9.44 Billion |

| CAGR (2023 - 2028) | 10.48 % |

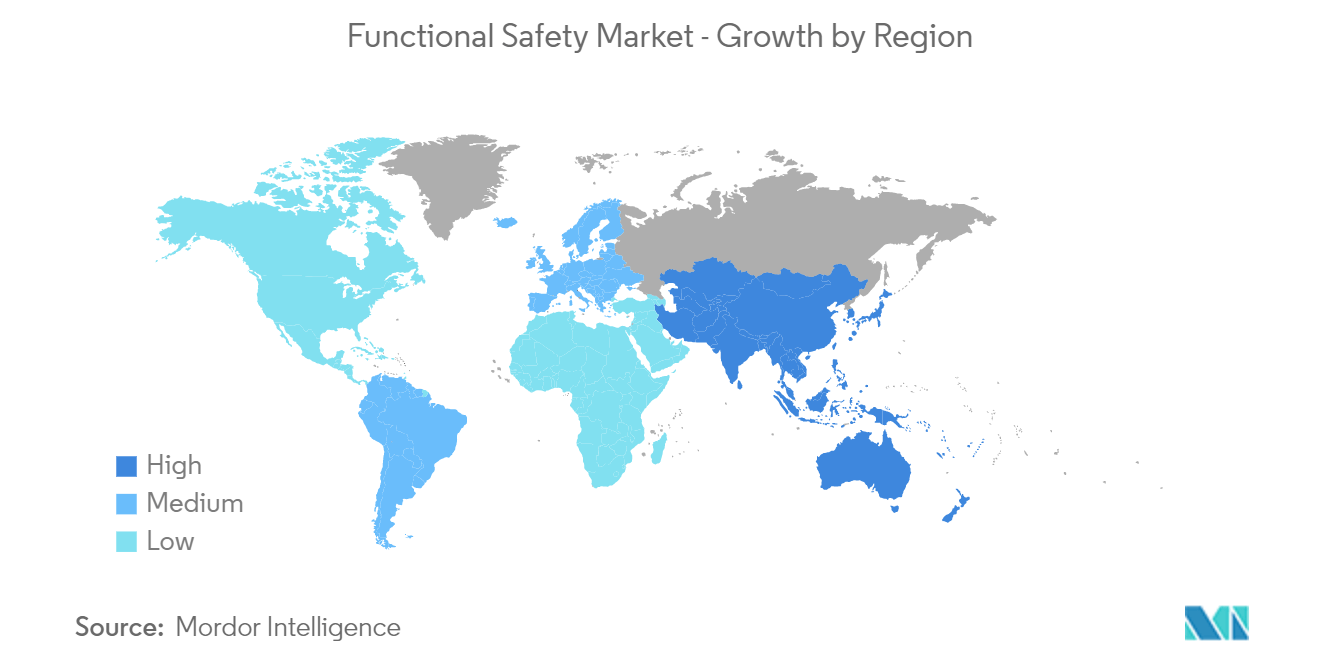

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Functional Safety Market Analysis

The Functional Safety Market size is expected to grow from USD 5.74 billion in 2023 to USD 9.44 billion by 2028, at a CAGR of 10.48% during the forecast period (2023-2028).

The increasing adoption of functional safety systems in a wide range of industries and the growing industrial safety standards are the factors driving the market growth.

- Oil and gas facilities are prone to accidents that can negatively impact society and the environment. Functional safety measures, including emergency shutdown systems, can significantly minimize the risk of disasters in oil and gas facilities.

- The increasing use of connected devices and the rapid installation of software solutions using over-the-air (OTA) are also expected to drive the demand for functional safety systems. Industrial Revolution 4.0 has increased the need for reliable security systems to protect individuals and property. These are the factors anticipated to contribute to the market's revenue growth during the forecast period.

- The adoption of functional safety systems and a datacentric approach provides enterprises in a wide range of industries with the required functionality that enables automatic prevention of dangerous failures and control in instances of such occurrences. They also offer facilities that humans cannot mimic.

- Although functional safety systems are driving the demand for the market across the world, the increasing complexity of these systems, coupled with high maintenance costs and the high initial cost of setting up these systems, is dissuading enterprises from investing in functional safety systems technology, thus leading to slow market penetration.

- The COVID-19 pandemic and lockdown restrictions around the world were impacting industrial activity. The lockdown impacts include supply chain disruptions, unavailability of raw materials used in the manufacturing process, labor shortages, price volatility that can cause end-product production to inflate, budget overruns, and shipping issues.

Functional Safety Market Trends

This section covers the major market trends shaping the Functional Safety Market according to our research experts:

Automation to be the Fastest-growing End-user Sector

- The automotive industry has undergone various changes over the past few years, integrating technological advancements into multiple types of vehicles. Previously, cars were mechanical, mostly with basic electrical systems that offered power for headlights and spark plugs. As technology progressed, vehicles were now equipped with advanced safety purposes, such as airbag deployment systems.

- The increase in these sensor-dependent features has driven engineers to develop more accurate sensors with automotive applications in mind. The industry's adoption of functional safety is predicted to increase due to these trends. It will enable automakers to react faster to market requirements, reduce manufacturing downtimes, enhance supply chains' efficiency, and expand productivity.

- The widespread use of modern vehicles powered by automotive electronic control units (ECU) has necessitated sophisticated safety measures. The process of functional safety has grown to be crucial to the process of developing ECU software. To reduce risks and damage in software or hardware failures, functional safety schemes for automobiles help diagnose malfunctions (electric and electronic) and specify the actions and procedures to be used.

- Electrification and automation are the two significant trends in the automotive sector. The emergence of electric vehicles in the industry has dramatically impacted the demand for sensors in the long term. More electric cars mean increased demand for sensors and a rise in sensors for applications, such as battery monitoring, various positioning, and detection of moving parts of automobiles.

- The automotive industry is among the prominent sectors that hold a significant share of the world's automated manufacturing facilities. The production facilities of various automakers are automated to maintain efficiency. The growing trend of replacing conventional vehicles with EVs is expected to augment the automotive industry's demand further.

North America Expected to Hold Significant Market Share

- The United States is one of the largest markets for functional safety systems globally. The country is renowned for its innovation capabilities and is at the forefront of significant developments surrounding the emerging technologies of the 4th Industrial Revolution. Newfound shale resources in the United States and an increasing number of oil and gas projects are additional indicators of market potential. Prominent vendors such as Honeywell International, Rockwell Automation, Banner Engineering Corp, and General Electric are headquartered in the country.

- The government is also focusing on increasing its energy generation capacity and is investing in such projects. For instance, in October 2022, the US Department of Energy (DOE) announced that the Idaho National Laboratory (INL) would receive USD 150 million in financing from the President's Inflation Reduction Act to modernize its infrastructure and advance nuclear energy research and development. The funding will help almost a dozen projects at INL's Advanced Test Reactor (ATR) and Materials Fuels Complex (MFC), both of which have been in operation for more than 50 years and play a critical role in developing nuclear technologies for governmental organizations, business, and global collaborations. With nuclear energy accounting for approximately 5% of domestic electricity production and 50% of all domestic clean energy production, it is essential to achieving President Biden's target of 100% clean electricity by 2035.

- Furthermore, in October 2022, the United States Department of Energy (DOE) announced more than USD 28 million across three funding opportunities to support research and development initiatives that promote and sustain hydropower as a crucial source of clean energy. The expansion of low-impact hydropower and pumped storage hydropower, the construction of new pumped storage hydropower facilities, and engagement with influential voices on issues like hydropower fleet modernization, sustainability, and environmental impacts will all be supported by funding provided by Bipartisan Infrastructure Law. Such initiatives of power-generating project investments certainly increase the demand for functional safety devices in the country.

- The US Energy Information Administration Stated that, in 2021, petroleum accounted for around 36% of American energy consumption. Still, it was also the main contributor to 46% (about 2,241 million metric tons) of all American energy-related CO2emissions. As government laws become more stringent, several firms focus on tracking and reducing their carbon emissions per product, which is anticipated to increase demand for fire and gas monitoring systems nationwide.

- According to the Government of Canada, the Canadian manufacturing industry accounts for approximately CAD 174 billion of its GDP, representing more than 10% of the country's total GDP. The manufacturing sector is the largest investor in R&D and implements new technologies that are expected to create scope for the market.

Functional Safety Industry Overview

The functional safety market comprises several global players vying for attention in a reasonably competitive market space, such as Rockwell Automation Inc., Emerson Electric Company, and Honeywell International Inc. The players in the market studied are looking to strengthen their competitiveness through various efforts, such as the innovation of products. Overall, the intensity of competitive rivalry is expected to be high.

- October 2022: Emerson launched its PlantWeb digital ecosystem to incorporate the AspenTech portfolio of asset-optimizing software powered by industrial artificial intelligence, creating the industry's most comprehensive digital transformation portfolio.

- September 2022: Votiva Singapore Pte Ltd, a Southeast Asian IT consultant that offers services for the deployment of enterprise resource planning (ERP) and customer relationship management (CRM) software, was acquired by Yokogawa Electric Corporation. ERP systems are at the heart of the solutions that Yokogawa offers to customers in the manufacturing industry to support smart manufacturing and digital transformation (DX). With this acquisition, the business will be able to increase the geographic scope of its Southeast Asian consulting, implementation, and technical support services for ERP solutions. Votiva will become Yokogawa Votiva Solutions as a result of the transaction.

Functional Safety Market Leaders

Rockwell Automation Inc.

Emerson Electric Company

Honeywell International Inc.

Yokogawa Electric Corporation

ABB Ltd

*Disclaimer: Major Players sorted in no particular order

Functional Safety Market News

- October 2022: Schneider Electric unveiled the newest generation of industrial technology to empower people and promote sustainable economic growth. The most recent version of EcoStruxure Automation Expert, the world's first software-centric industrial automation system, EcoStruxure Automation Expert 22.1, further integrates with the AVEVA System Platform so that users can access AVEVA's substantial asset library based on the most current situational awareness standards and design graphics using the Operations Management Interface. By developing AVEVA graphics and control applications in the same environment, training time is reduced by more than half while quality increases.

- September 2022: Siemens unveiled Fire Safety Digital Services, a new portfolio of digital and managed services that link fire safety devices to the cloud, to assist organizations in transitioning from a compliance-driven, reactive approach to total protection through intelligent safety. Through adopting digital services in operation, event management, and maintenance, customers may improve risk identification and prevention, make better risk-control decisions, ensure business continuity, and establish a secure environment for people and assets.

Functional Safety Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Assessment of Impact of COVID-19 on the Industry

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Standards of Industrial Safety

5.1.2 Increasing Adoption of Functional Safety Systems in Industries

5.2 Market Restraints

5.2.1 Increasing Complexity, High Initial Costs and Maintenance Costs

6. MARKET SEGMENTATION

6.1 Device Type

6.1.1 Safety Sensors

6.1.2 Safety Controllers/Modules/Relays

6.1.3 Safety Switches

6.1.4 Programmable Safety Systems

6.1.5 Emergency Stop Devices

6.1.6 Final Control Elements (Valves, Actuators)

6.1.7 Other Device Types

6.2 Safety Systems

6.2.1 Burner Management Systems (BMS)

6.2.2 Turbomachinery Control (TMC) Systems

6.2.3 High-Integrity Pressure Protection Systems (HIPPS)

6.2.4 Fire and Gas Monitoring Control Systems

6.2.5 Emergency Shutdown Systems (ESD)

6.2.6 Supervisory Control and Data Acquisition (SCADA) Systems

6.2.7 Distributed Control Systems (DCS)

6.3 End-user Industry

6.3.1 Oil and Gas

6.3.2 Power Generation

6.3.3 Food and Beverage

6.3.4 Pharmaceutical

6.3.5 Automotive

6.3.6 Other End-user Industries

6.4 Geography

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 United Kingdom

6.4.2.2 Germany

6.4.2.3 France

6.4.2.4 Rest of Europe

6.4.3 Asia Pacific

6.4.3.1 China

6.4.3.2 Japan

6.4.3.3 India

6.4.3.4 Rest of Asia-Pacific

6.4.4 Latin America

6.4.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Rockwell Automation Inc.

7.1.2 Emerson Electric Company

7.1.3 Honeywell International Inc.

7.1.4 Yokogawa Electric Corporation

7.1.5 ABB Ltd

7.1.6 Schneider Electric SE

7.1.7 Siemens AG

7.1.8 General Electric Company

7.1.9 Omron Corporation

7.1.10 SICK AG

7.1.11 Panasonic Industry Europe GmbH (Panasonic Corporation)

7.1.12 Pepperl+Fuchs

7.1.13 Banner Engineering Corporation

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Functional Safety Industry Segmentation

Functional safety is part of the overall safety of the system or piece of equipment, which depends on automatic protection. Functional safety systems are composed of electrical and electronic elements that are used for the fulfillment of safety functions in most of the related sectors in several industries, as there is a high risk of related injuries.

The scope of the study includes safety systems, such as burner management systems, turbomachinery control systems, and emergency shutdown systems, which are used in a range of end-user industries such as oil and gas, power generation, food and beverage, pharmaceutical, automotive, and other end-user industries in various regions worldwide. The study also includes an assessment of the impact of COVID-19 on the market. Furthermore, the research examines the underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates during the forecast period.

| Device Type | |

| Safety Sensors | |

| Safety Controllers/Modules/Relays | |

| Safety Switches | |

| Programmable Safety Systems | |

| Emergency Stop Devices | |

| Final Control Elements (Valves, Actuators) | |

| Other Device Types |

| Safety Systems | |

| Burner Management Systems (BMS) | |

| Turbomachinery Control (TMC) Systems | |

| High-Integrity Pressure Protection Systems (HIPPS) | |

| Fire and Gas Monitoring Control Systems | |

| Emergency Shutdown Systems (ESD) | |

| Supervisory Control and Data Acquisition (SCADA) Systems | |

| Distributed Control Systems (DCS) |

| End-user Industry | |

| Oil and Gas | |

| Power Generation | |

| Food and Beverage | |

| Pharmaceutical | |

| Automotive | |

| Other End-user Industries |

| Geography | ||||||

| ||||||

| ||||||

| ||||||

| Latin America | ||||||

| Middle East and Africa |

Functional Safety Market Research FAQs

How big is the Functional Safety Market?

The Functional Safety Market size is expected to reach USD 5.74 billion in 2023 and grow at a CAGR of 10.48% to reach USD 9.44 billion by 2028.

What is the current Functional Safety Market size?

In 2023, the Functional Safety Market size is expected to reach USD 5.74 billion.

Who are the key players in Functional Safety Market?

Rockwell Automation Inc., Emerson Electric Company, Honeywell International Inc., Yokogawa Electric Corporation and ABB Ltd are the major companies operating in the Functional Safety Market.

Which is the fastest growing region in Functional Safety Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Functional Safety Market?

In 2023, the North America accounts for the largest market share in the Functional Safety Market.

Functional Safety Industry Report

Statistics for the 2023 Functional Safety market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Functional Safety analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.