Glass Bottle and Container Market Size

| Study Period | 2018 - 2028 |

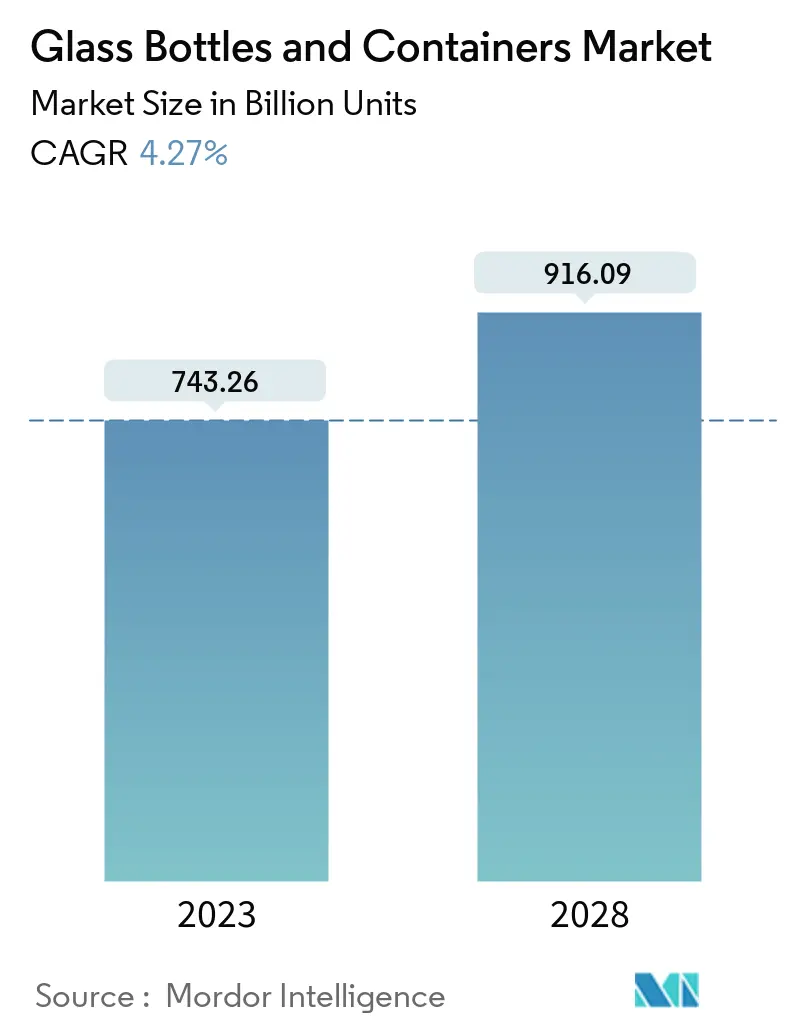

| Market Volume (2023) | 743.26 Billion units |

| Market Volume (2028) | 916.09 Billion units |

| CAGR (2023 - 2028) | 4.27 % |

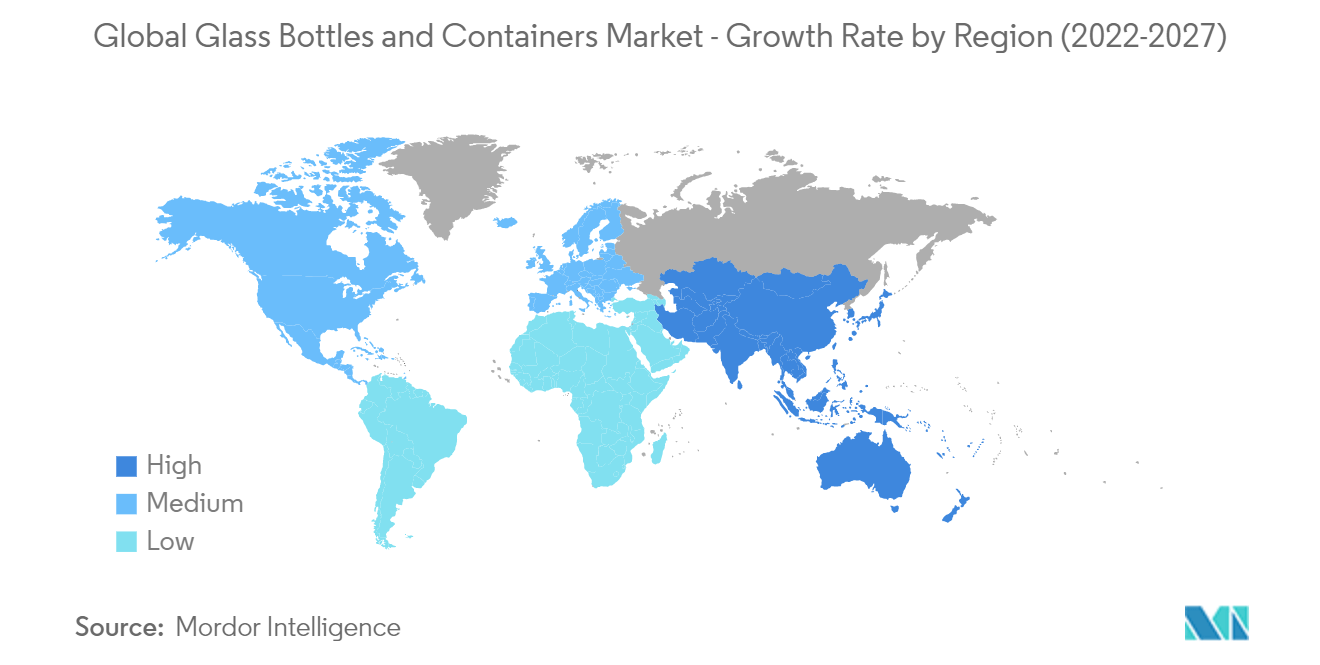

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Glass Bottle and Container Market Analysis

The Glass Bottles, Containers Market size is expected to grow from 743.26 billion units in 2023 to 916.09 billion units by 2028, at a CAGR of 4.27% during the forecast period (2023-2028).

The COVID -19 outbreak created a growing necessity for industries in the food & beverage sector to focus more on hygiene and sanitization. Given the current situation, people opt for a healthy and sustainable lifestyle. As most of the products in this sector are included in essential services, it becomes crucial for the packaging sector to follow conservative practices.

- Alcoholic drinks, like beer, accounted for the largest segment of the market, as glass does not react with the chemicals present in drinks and, therefore, preserves the aroma, strength, and flavor of these beverages, making it a favorable option for packaging. Due to this reason, a majority of the beer volume is transported in glass bottles and is expected to continue over the study period. Glass packaging is 100% recyclable, which makes it a desirable packaging option from the environmental point of view. Six tons of recycled glass directly save 6 tons of resources and reduce the emission of CO2 by 1 ton.

- One of the main factors driving the market's growth is the increase in beer consumption worldwide. Beer is one of the alcoholic beverages that use glass bottles for packaging. It is packed in dark-colored glass bottles to preserve the contents, which are prone to spoilage when exposed to UV light.

- Besides, consumers increasingly prefer craft beer brewed locally by small and large breweries. This trend has led glass packaging manufacturers to adjust their production and, in some cases, even switch to other growth areas, such as food and beverage. Premium food and beverage brands prefer glass (container glass) over other packaging options, such as plastic, as glass is chemically inert, non-porous, and impermeable.

- In February 2021, the Loop Reusable/Returnable Packaging platform was launched in Canada in partnership with Loblaw Inc to bring waste-free shopping for various food and household products. Also, the iconic Heinz Ketchup (Glass) Bottle is made available on the Loop. Additionally, a recent survey (1,521 Canadians were surveyed online from December 9-15, 2020) by Kraft Heinz Canada showcased that Canadians have preferences for more sustainable options, despite an incremental cost. Almost 65% of respondents made an effort to choose brands that come in sustainable packaging options.

- There has been an increasing trend of transparency in food packaging over the past few years. Going beyond the labeled listed ingredients, consumers also want to see the physical product before purchasing. To capture this trend, many companies, especially dairy product companies, have started offering their products in transparent glass containers.

- High competition from substitute packaging like plastic and metal is challenging the market's growth. Incremental advancements in plastic packaging solutions pose a threat to the studied market. This can be primarily attributed to the popularity of plastics, such as polyethylene terephthalate (PET), as substitutes for glass bottle formats.

Glass Bottle and Container Market Trends

This section covers the major market trends shaping the Glass Bottles & Containers Market according to our research experts:

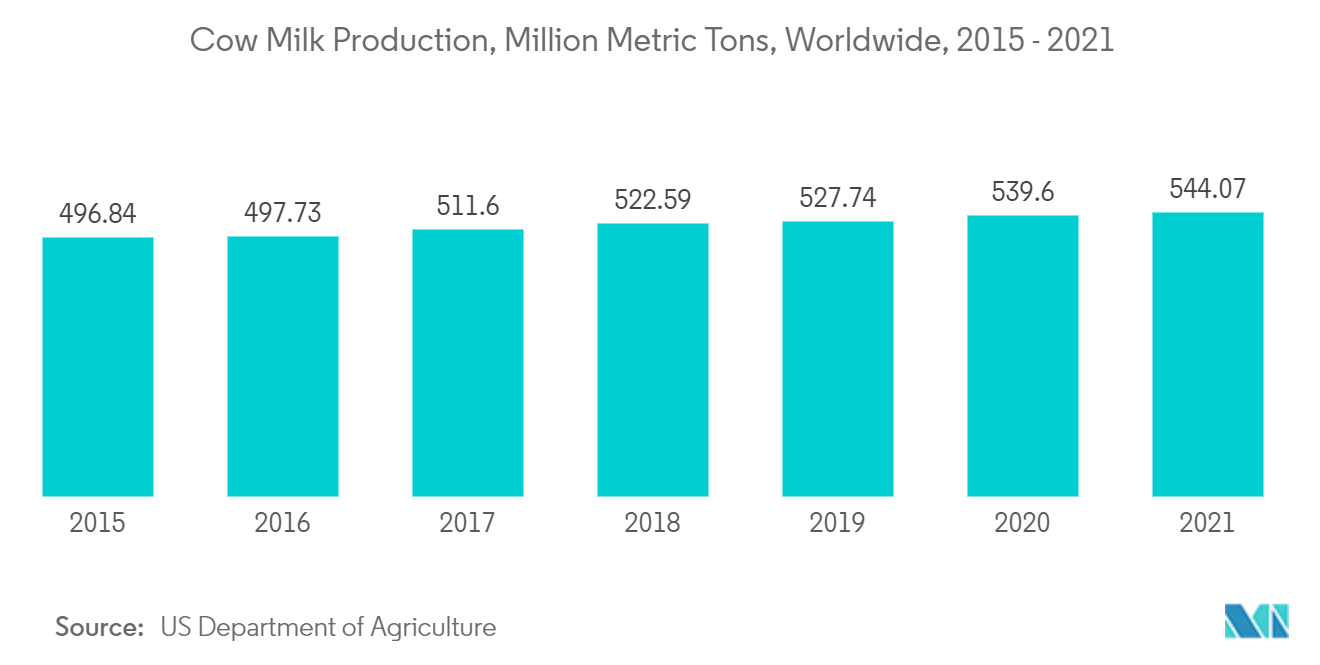

Milk is Expected to Account for a Significant Market Share

- According to several studies by European universities, the old glass milk bottle appears to be returning. Milk vending machines, each containing glass bottles, have been popping up across Northern Ireland over the last two years and continue to do so. Besides sustainability, health consciousness is another factor compelling customers to switch to glass. Studies from authoritative sources, such as National Geographic, Time, Business Insider, The Guardian, and the New York Times, along with countless research papers published by universities across the world and even the US Food and Drug Administration, have highlighted the drawbacks of using plastic bottles when compared to the relatively advantageous traits of glass bottles.

- In June 2021, the UK-based supermarket Morrisons decided to bring traditional glass milk bottles back to the shelves of seven of its Kent stores. The one-pint bottles will be delivered to supermarkets by the dairy farms and, once returned by customers, will be collected and sanitized to enable them to be reused, possibly for up to 10 years. Morrisons says it has committed to a 50% reduction across its own-brand primary plastic packaging by 2025, with over 83% of Morrisons' own-brand plastic packaging now able to be recycled.

- Moreover, the COVID-19 pandemic helped surge demand for doorstep milk delivery in the glass. In August 2021, Britain’s biggest traditional milk delivery company, Milk & More, added 175,000 new online customers, helping sales to grow by 20 % from GBP 156 million to GBP 186 million. The business, which also delivers groceries, now has 400,000 customers across much of England, with 90 % signing up for glass bottles that cost 81p for a pint of milk, more than the average 50p-a-pint in plastic containers. DiaryDrop, based in Alderly Edge, which has 3,000 customers in Cheshire, announced a significant reversal in the glass milk bottle delivery trend. Another Cheshire-based milk supplier, Creamline Dairies, witnessed an increase of 85% in the number of people getting glass bottles delivered since last year.

- The Pan-UK company, Milk & More, and East-London dairy giant, Parker Dairies, witnessed a substantial increase in the demand for glass bottles. Most dairies from London mentioned that the change is mostly from their younger consumers, whose families seem more willing to pay a little extra for the service rather than the plastic in their efforts to help the environment. The company also provides services offering refillable milk bottles. Once finished and rinsed, the bottles can be collected from doorsteps by Milk & More to be refilled and reused.

- Moreover, many dairies have been adopting glass bottle packaging for milk to increase sales and brand recognition. For instance, Mossgiel Farm, a dairy farm in Scotland, has seen an impressive increase in popularity, almost doubling its milk sales, after swapping its plastic milk containers for glass bottles.

Asia-Pacific is Expected to Hold the Largest Market Share

- The Asia-Pacific region is expected to register a significant growth rate compared to other nations owing to an increase in demand for pharmaceutical and chemical industries, which prefer glass packaging because of the inert nature of glass bottles. China, India, Japan, and Australia, among others, are the prominent nations contributing to the growth of the Asia Pacific glass packaging market.

- China is one of the world's largest pharmaceutical markets. Compared to many industrialized countries, healthcare spending in China is still modest. The country is steadily improving its domestic drug research and development skills and its domestic medication production, allowing the government to provide affordable health care to an increasing number of Chinese people. As part of a long-term aim to establish an internationally competitive homegrown biopharmaceutical industry, the Chinese government is granting tax and other financial advantages. Beijing's national health strategy currently places a premium on efficiency and the construction of innovation centers, both of which are aided by financial incentives.

- Three large centers of innovation, the Zhangjiang Hi-Tech Park near Shanghai, the BioBay in Suzhou, and the Shenzhen innovation hub, which is often referred to as China's Silicon Valley for pharma companies because it is already home to global companies such as Huawei – are the main pillars of the government's approach here. Hence, there is a potential growth opportunity for the domestic players in the container market as they might experience an increase in demand for glass bottles and containers from these companies. Additionally, alcohol consumption in China is significantly increasing over the years. As per Brazil-based bank Banco do Nordeste, consumption of alcoholic beverages in China is expected to reach 54.12 billion liters in 2021. Also, many alcoholic beverage companies are seeking to expand in the country to seize the opportunity.

- The popularity of South Korean beauty products is due to their high performance, coupled with fun packaging and sensorial cues, as well as affordable prices. By winning the attention of bloggers, vloggers, and the media, the K-beauty wave is spreading to retailers outside Asia. This has been the primary reason for the increase in exports of the country's cosmetic products, further propelling the market for cosmetic packaging. Thus, growth in the cosmetic sector is driving collaborations and partnerships and is expected to drive the glass bottle and container market in South Korea over the forecast period.

- In March 2021, Verescence, a glass manufacturer for perfumery and cosmetics, acquired Pacifglas, a South Korean glass packager, and formed a long-term partnership with Amorepacific. Verescence's three glass production sites and four decoration locations in Europe and North America manufacture 500 million bottles annually. Verescenceintends to build on this strong foundation to become a pan-Asian leader, investing in technology and capacity to meet the growing demand for high-end glass.

Glass Bottle and Container Industry Overview

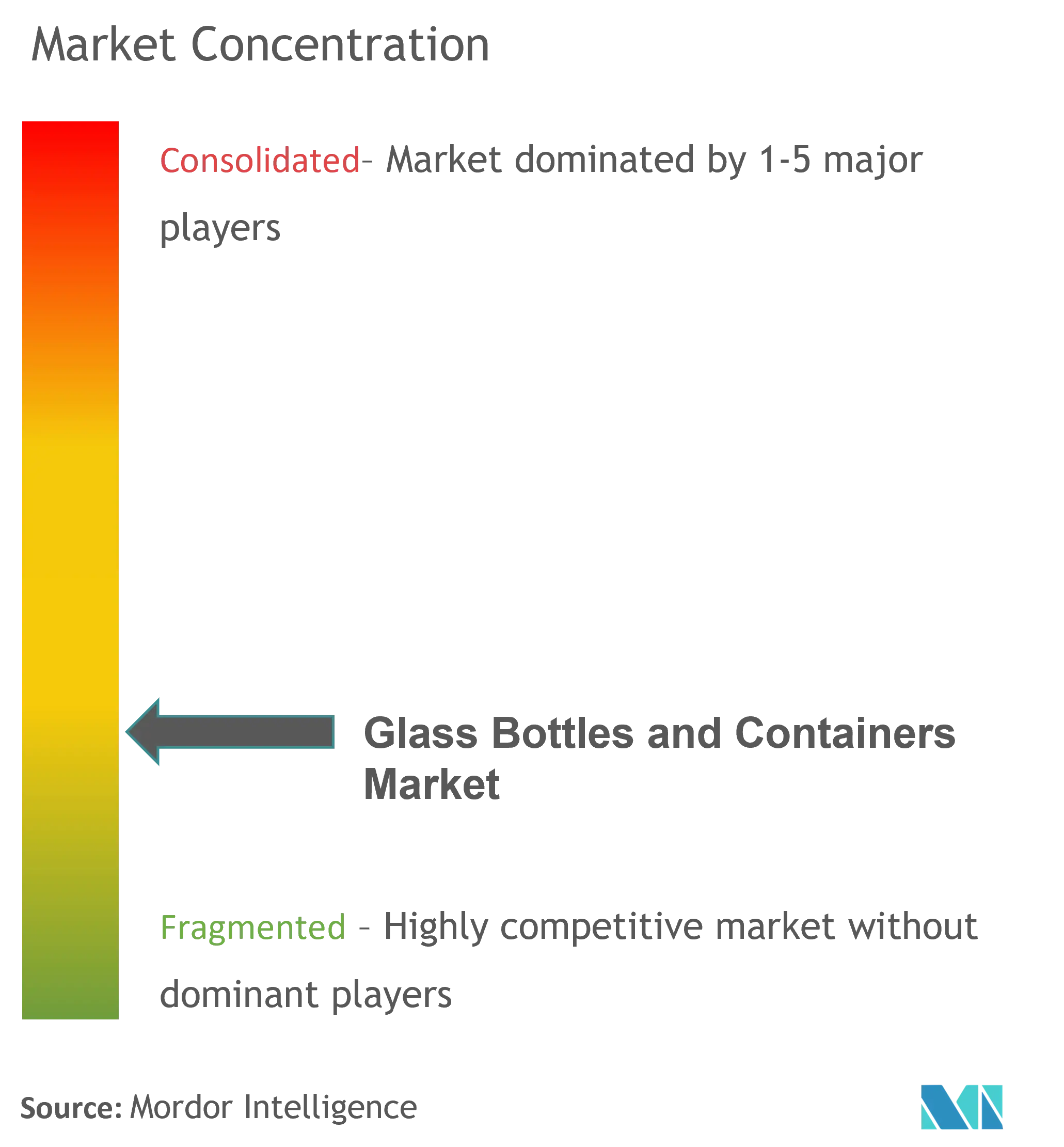

The glass bottles and containers market is highly competitive and fragmented. A few of the major companies in this market are Owens-Illinois Inc., Hindustan National Glass & Industries Ltd, Vitro, S.A.B. De CV, Amcor Ltd, etc. These established vendors with strong access to distribution channels have a strong foothold in the market studied.

- November 2021 - Saverglass opened a new 430,000 square-foot multi-service warehouse in Fairfield, California, to provide wine and alcohol companies fast access to a spectrum of glass bottle services. With more than three decades in California, the company operates multiple warehouses near Napa to meet the customers' increasing demand. This new multi-service warehouse demonstrates the company's dedication to providing exceptional service and creative and modern glass bottle solutions to its clients.

- November 2021 - Verescence announced the launch of Verre Infini 20 (Infinite Glass), a new glass composition designed to expand Verescence's PCR1 glass manufacturing capabilities worldwide. This innovative composition combines 20% PCR with a glass tint designed to meet the visual needs of upscale businesses. This glass composition, already being made in France and Spain, will be gradually implemented in the United States in the first quarter of 2022 and South Korea in 2023.

- October 2021 - Vitro announced an approximately USD 70 million investment for constructing a new Container furnace at the Vitro plant in Toluca, State of Mexico. The new furnace will provide additional capacity to support our customers and their growing requirements for glass containers, providing a higher level of service in the regions and segments where we participate.

Glass Bottle and Container Market Leaders

Owens-Illinois Inc.

Ardagh Packaging Group Plc

Vidrala, S.A.

Verallia Packaging SAS (Horizon Holdings II SAS)

Wiegand-Glas GmBH

*Disclaimer: Major Players sorted in no particular order

Glass Bottle and Container Market News

- February 2022 - Stoelzle Oberglas, headquarters of the Stoelzle Glass Group, completed the rebuild and expansion of its flint furnace, a EUR 22 million investment focused on making the production site more efficient and also more sustainable in terms of energy efficiency and CO2 emissions. The new flint furnace will reach around 270 tons of melted glass daily. The state-of-the-art melting technology will reduce the amount of energy used in the melting process by an estimated 13% per ton of glass.

- October 2021 - Owens-Illinois (O-I), a glass packaging company, announced to spend BRL 990 million (USD 178.8 million) on two new facilities in Brazil. The investment is part of a USD 680 million package from the world's largest container glassmaker that will be made between 2022 and 2024 to enhance production in areas with limited supply and introduce a technology that will alter the glass manufacturing process.

- Aug 2021 - ALPLA Group announced the acquisition of Wolf Plastics Group to expand its product portfolio and increase its presence in Central and Southeastern Europe. The company intends to use Wolf Plastic’s expertise in manufacturing plastic buckets and canisters to expand its product portfolio.

Glass Bottle and Container Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Intensity of Competitive Rivalry

4.3.5 Threat of Substitutes

4.4 Impact of COVID-19 on Glass Bottles and Containers Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Demand from Food and Beverage Industry

5.1.2 Sustainability and Recyclability Initiatives Moving Packagers and Consumer Brands to Glass Packaging

5.2 Market Restraints

5.2.1 High Carbon Footprint due to Glass Manufacturing

5.2.2 Operation and Logistical Concerns

6. MARKET SEGMENTATION

6.1 End-user Vertical

6.1.1 Bevarages

6.1.1.1 Alcoholic

6.1.1.1.1 Beer and Cider

6.1.1.1.2 Wine and Spirits

6.1.1.1.3 Other Alcoholic

6.1.1.2 Non-alcoholic

6.1.1.2.1 Carbonated Soft Drinks

6.1.1.2.2 Milk

6.1.1.2.3 Water and Other Non-alcoholic (Juices, etc.)

6.1.2 Food

6.1.3 Cosmetics

6.1.4 Pharmaceutical

6.1.5 Other End-user Verticals

6.2 Geography

6.2.1 North America

6.2.1.1 United States

6.2.1.2 Canada

6.2.2 Europe

6.2.2.1 United Kingdom

6.2.2.2 Germany

6.2.2.3 France

6.2.2.4 Italy

6.2.2.5 Spain

6.2.2.6 Poland

6.2.2.7 Russia

6.2.2.8 Rest of Europe

6.2.3 Middle-East and Africa

6.2.3.1 United Arab Emirates

6.2.3.2 Saudi Arabia

6.2.3.3 South Africa

6.2.3.4 Rest of Middle-East and Africa

6.2.4 Asia-Pacific

6.2.4.1 China

6.2.4.2 India

6.2.4.3 Japan

6.2.4.4 South Korea

6.2.4.5 Rest of Asia-Pacific (SEA, ANZ etc.)

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Owens-Illinois Inc.

7.1.2 Vidrala SA

7.1.3 Ardagh Packaging Group PLC

7.1.4 Wiegand-Glas GmbH

7.1.5 Verallia Packaging SAS (Horizon Holdings II SAS)

7.1.6 Vetropack Holding Ltd

7.1.7 Stolzle Glass Group (CAG Holding GmbH)

7.1.8 Gaasch Packaging (UK) Ltd

7.1.9 Beatson Clark Limited

7.1.10 Vitro SAB de CV

7.1.11 Consol glass (Pty) Ltd

7.1.12 Glassworks International Limited

7.1.13 Gerresheimer AG

7.1.14 Middle East Glass Manufacturing Co SAE

7.1.15 Crestani SRL

7.1.16 BA VIDRO SA ( BA Glass BV)

7.1.17 PGP Glass Private Limited

7.1.18 Verescence France

7.1.19 SGD SA (SGD Pharma)

7.1.20 Saver Glass SAS

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Glass Bottle and Container Industry Segmentation

Glass bottles and containers provide an ideal way to keep the consumables safe, fresh, and healthy for a longer period and ease of transport. Glass bottles and containers are majorly used in the alcoholic and non-alcoholic beverage industry due to their ability to maintain chemical inertness sterility, and non-permeability. The glass bottles and containers market is segmented by end-user vertical (beverages, food, cosmetics, and pharmaceutical) and geography.

| End-user Vertical | ||||||||||||

| ||||||||||||

| Food | ||||||||||||

| Cosmetics | ||||||||||||

| Pharmaceutical | ||||||||||||

| Other End-user Verticals |

| Geography | ||||||||||

| ||||||||||

| ||||||||||

| ||||||||||

|

Glass Bottle and Container Market Research FAQs

How big is the Glass Bottles and Containers Market?

The Glass Bottles and Containers Market size is expected to reach 743.26 billion units in 2023 and grow at a CAGR of 4.27% to reach 916.09 billion units by 2028.

What is the current Glass Bottles and Containers Market size?

In 2023, the Glass Bottles and Containers Market size is expected to reach 743.26 billion units.

Who are the key players in Glass Bottles and Containers Market?

Owens-Illinois Inc., Ardagh Packaging Group Plc, Vidrala, S.A., Verallia Packaging SAS (Horizon Holdings II SAS) and Wiegand-Glas GmBH are the major companies operating in the Glass Bottles and Containers Market.

Which is the fastest growing region in Glass Bottles and Containers Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Glass Bottles and Containers Market?

In 2023, the Asia-Pacific accounts for the largest market share in the Glass Bottles and Containers Market.

Glass Bottle and Container Industry Report

Statistics for the 2023 Glass Bottle and Container market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Glass Bottle and Container analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.