Interventional Cardiology Devices Market Size

| Study Period | 2018 - 2028 |

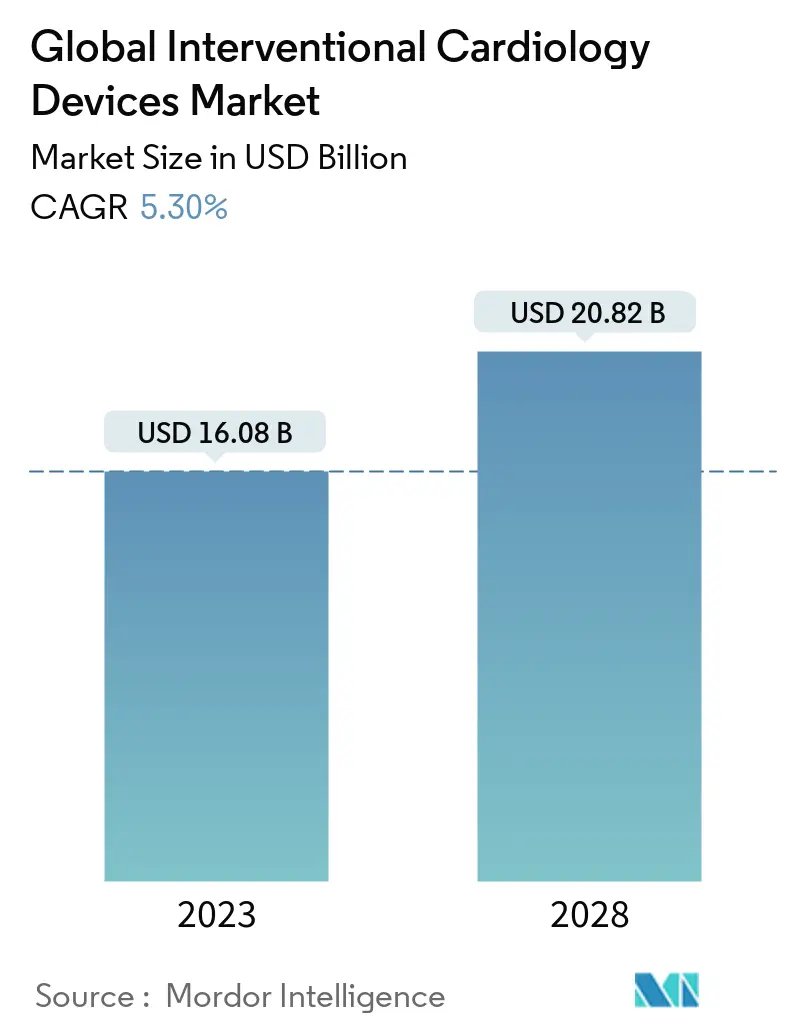

| Market Size (2023) | USD 16.08 Billion |

| Market Size (2028) | USD 20.82 Billion |

| CAGR (2023 - 2028) | 5.30 % |

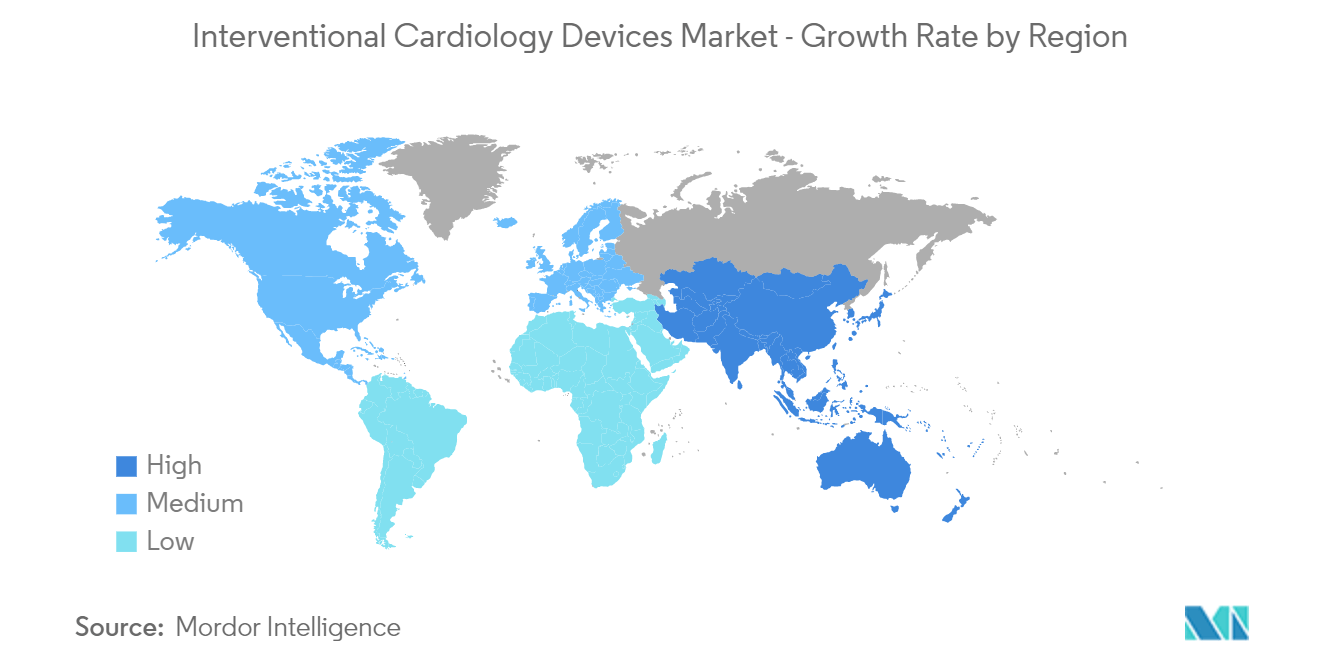

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Interventional Cardiology Devices Market Analysis

The Global Interventional Cardiology Devices Market size is expected to grow from USD 16.08 billion in 2023 to USD 20.82 billion by 2028, at a CAGR of 5.30% during the forecast period (2023-2028).

The interventional cardiology devices market is anticipated to have been significantly impacted by the COVID-19 pandemic as most elective surgeries were deferred to contain the spread of the SARS-Cov2 viral transmission. The article titled "Electrophysiology and Interventional Cardiology Procedure Volumes During the Coronavirus Disease 2019 Pandemic" published in the National Library of Medicine in October 2021, stated the impact of the COVID-19 pandemic on the number of interventional cardiology (IC) and electrophysiology (EP) operations performed globally. Multiple clinical services in the area of interventional cardiology were immediately discontinued upon the onset of the COVID-19 pandemic in order to better allocate resources and prevent potential exposure across numerous countries. All percutaneous coronary interventions (PCI) performed in the United Kingdom during the lockdown imposed by the pandemic were retrospectively studied by the British Cardiovascular Interventional Society and their results were compared to PCI volumes during the pre-pandemic period. The results indicated that PCI volumes decreased by 49%, with the highest decline occurring in PCI for stable angina (66% reduction). Thus, the outbreak has had an adverse impact on the market's growth in its preliminary phase. However, the market is anticipated to gain traction over the coming years as most of elective surgical procedures and treatments have resumed worldwide.

Furthermore, the major factors for the growth of the interventional cardiology devices market include the growing prevalence of coronary artery diseases (CADs), technological advancements in interventional cardiology devices, and the growing demand for minimally invasive treatment globally.

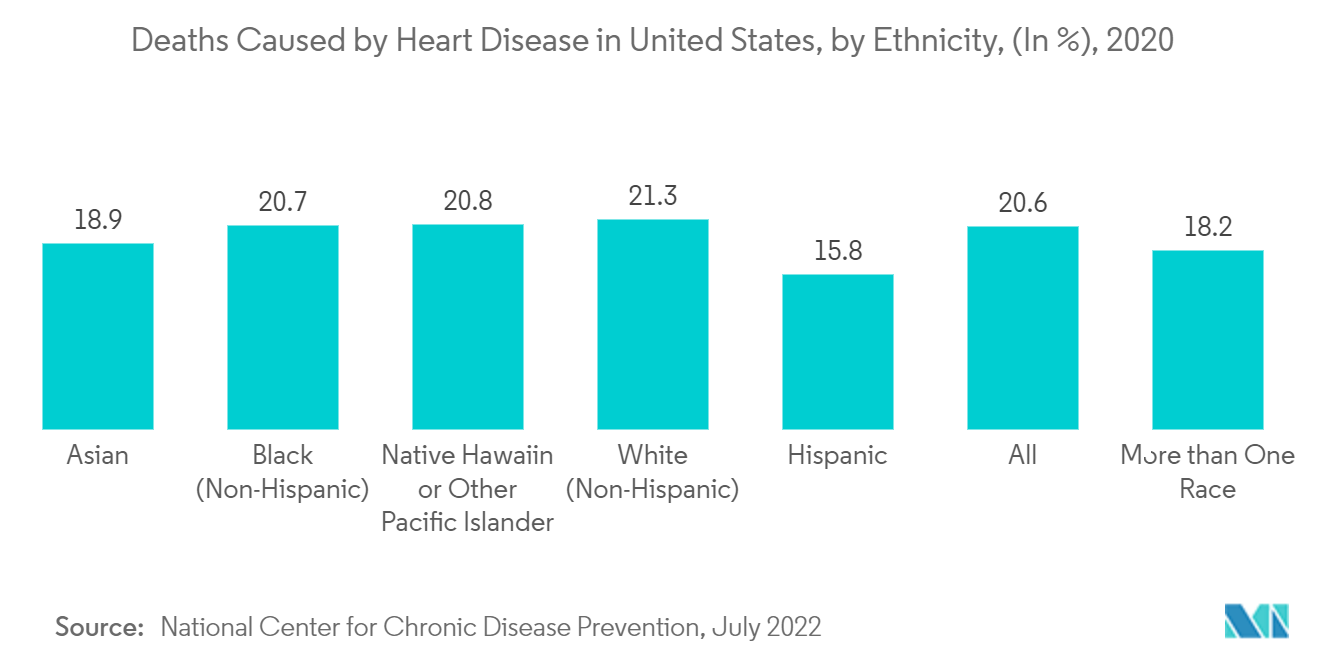

Heart-related diseases are the most serious health conditions and the leading cause of death across the world. Coronary artery disease (CAD) is one of the most common causes of morbidity and mortality in low-income as well as middle-income and developed countries. For instance, according to the World Health Organization data, updated in 2022, an estimated 17.9 million people die due to cardiovascular diseases worldwide each year, amounting to 35% of global deaths. Additionally, 85% of these cardiovascular disease deaths are due to heart attack and stroke. In addition, according to the National Center for Chronic Disease Prevention and Health Promotion, Division for Heart Disease and Stroke Prevention data updated in July 2022, coronary heart disease is the most common type of heart disease. Moreover, every year, about 805,000 people in the United States have a heart attack. People suffering from cardiovascular diseases or those who are at high cardiovascular risk need early detection and intervention to avoid fatal consequences. Therefore, the increasing burden of cardiovascular diseases, including coronary artery diseases, is anticipated to boost the usage of coronary stents, in turn, driving the market growth over the forecast period.

Moreover, market players are competing to launch advanced products for better treatment and have invested in research and development programs to improve their existing product lines and launch new product portfolios. For instance, in February 2022, Cardiovascular Systems, Inc. announced it had partnered with Innova Vascular, Inc. (Innova) to develop a full line of novel thrombectomy devices. Similarly, in July 2021, ORIGIN SC and ORIGIN NC, two high-performance balloons for vessel preparation, were introduced by MedAlliance, a privately held medical technology company dedicated to developing novel drug-eluting balloons (DEBs) for patients suffering from life-threatening coronary and peripheral arterial disease.

Moreover, compared to conventional surgeries, the several advantages of minimally invasive surgeries, such as reduced surgical pain, injury, scarring, hospital stay, higher accuracy, and speedy recovery time, are encouraging an increasing number of patients to opt for minimally invasive balloon angioplasty surgeries. As per an article titled "Percutaneous Transluminal Angioplasty and Balloon Catheters" published in July 2022, the incidence of major complications like myocardial infarction (MI), stroke, and death is variable in various angioplasty procedures. Incidence is as low as (< 1%) in cardiac and femoral artery procedures.

However, a stringent regulatory scenario for manufacturing interventional cardiology devices and the availability of effective first-line treatments are expected to restrain the market's growth.

Interventional Cardiology Devices Market Trends

This section covers the major market trends shaping the Interventional Cardiology Devices Market according to our research experts:

Drug-eluting Stents Segment Is Expected to Witness Significant Growth over the Forecast Period

The drug-eluting stents sub-segment is predicted to observe significant growth over the forecast period. Drug-eluting stents are coated with medication that is slowly released to help prevent the growth of scar tissue in the artery lining. This helps the artery remain smooth and open, ensuring good blood flow. These stents are usually used for the lower extremities, and they provide results that are better than self-expanding and balloon-expanding stents. Thus, the growing adoption of advanced cardiovascular treatments and the increasing technological advancements in the field of drug-eluting stents are expected to be the major drivers of the growth of the segment.

For instance, in August 2021, SINOMED, a medical device company, announced the first commercial implantation of the HT Supreme Drug-eluting Stent (DES) at the University Hospital Galway, in partnership with the National University of Ireland Galway, marking the start of its European launch. Similarly, in May 2022, Medtronic plc announced it had received United States Food and Drug Administration (FDA) approval for the Onyx Frontier drug-eluting stent (DES). As the latest evolution in the Resolute DES family, Onyx Frontier DES leverages the same stent platform as Resolute Onyx DES, with an enhanced delivery system. Likewise, in January 2021, Boston Scientific received FDA approval for its Synergy Megatron Drug Eluting stent system, which is designed for the treatment of large proximal near aorta.

Thus, owing to the aforementioned factors, the drug-eluting stents segment is expected to register healthy growth over the forecast period.

North America Expected to Dominate the Market over the Forecast Period

The presence of sophisticated healthcare infrastructure, favorable government initiatives for product development, and high patient awareness levels, coupled with an increasing target patient population, are expected to be some of the prominent drivers for the growth of the interventional cardiology devices market over the coming years in the region. According to the American Heart Association, by 2035, around 45% of the United States population is likely to suffer from heart disease due to factors like high obesity, high smoking, and unhealthy lifestyles, which may lead to heart attacks and other related issues.

North America has a high consumption rate of premium-priced interventional cardiology devices, and it is the region that can cater to a high rate of innovation in medical devices, thus dominating the market studied. Additionally, a few key market players in the region are developing novel products and technologies to compete with existing products, while others are acquiring and partnering with the other companies trending in the market. For instance, in June 2021, Abbott received the United States Food and Drug Administration’s approval for its XIENCE family of stents for its one-month dual-antiplatelet therapy (DAPT) labeled for high bleeding risk (HBR) patients in the United States. Similarly, in March 2021, the United States Food and Drug Administration approved the first in the world non-surgical heart valve to treat pediatric and adult patients with a native or surgically repaired right ventricular outflow tract (RVOT), the part of the heart that carries blood out of the right ventricle to the lungs.

Thus, owing to the aforementioned factors, the market studied is anticipated to witness steady growth in the North American region over the forecast period.

Interventional Cardiology Devices Industry Overview

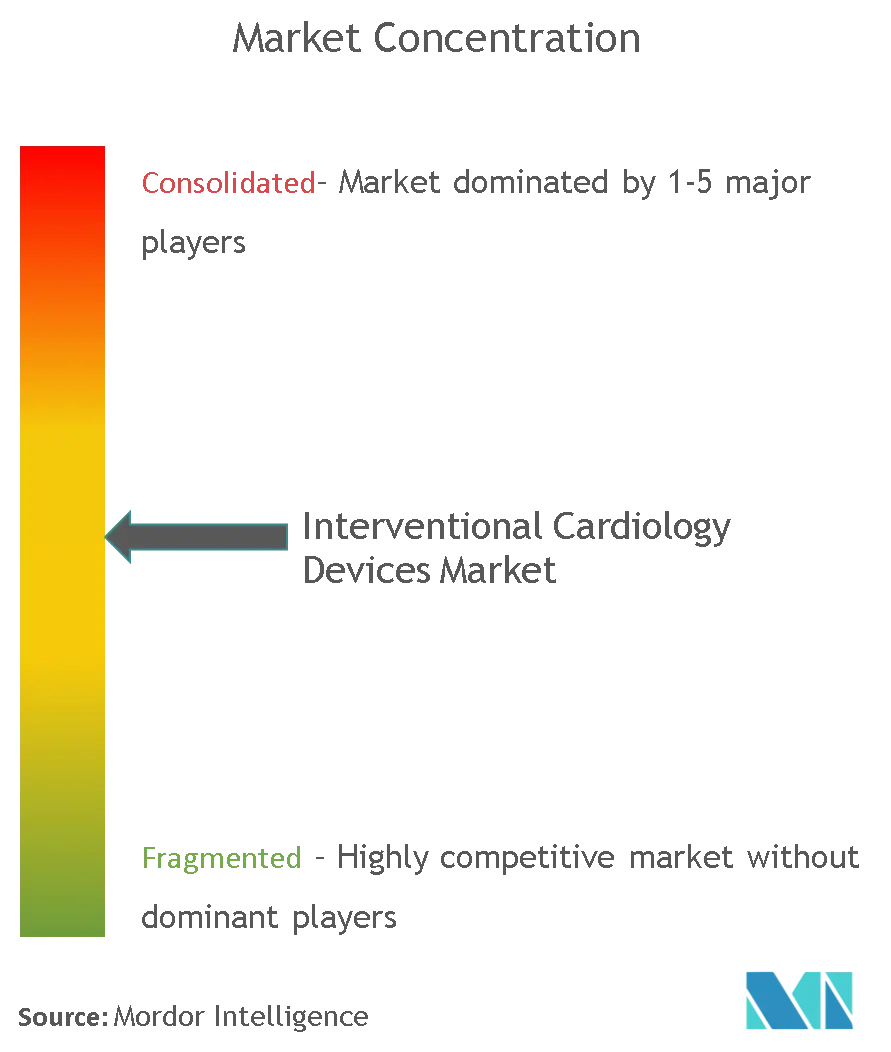

The interventional cardiology devices market is moderately competitive. Some key market players are Abbott Laboratories, B. Braun Melsungen AG, Biosensors International Ltd, Biotronik, Boston Scientific Corporation, Cardinal Health Inc., Cook Medical Inc., Medtronic PLC, and Terumo Medical Corporation. The major players are involved in strategies such as investing in research and development activities and new product launches, along with forming alliances such as acquisitions and collaborations, to secure a position in the global competitive market.

Interventional Cardiology Devices Market Leaders

Cook Medical Inc.

Abbott Laboratories

Boston Scientific Corporation

Terumo Medical Corporation

Medtronic plc

*Disclaimer: Major Players sorted in no particular order

Interventional Cardiology Devices Market News

In July 2021, Abbott launched its XIENCE family of stents, which received the US Food and Drug Administration’s (FDA) approval for one-month DAPT labeling for high bleeding risk (HBR) patients in the United States. In addition, XIENCE stents recently received the CE Mark approval for DAPT in 28 days, thus, ensuring XIENCE stents the shortest DAPT indication in the world.

In May 2021, NiTiDES, a novel polymer-free self-expanding Amphilimus eluting stent from Alvimedica for superficial femoral artery (SFA) lesions, received the CE mark.

Interventional Cardiology Devices Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Growing Prevalence of Coronary Artery Diseases (CADs)

4.2.2 Technological Advancements in Interventional Cardiology Devices

4.2.3 Growing Demand for Minimally Invasive Treatment

4.3 Market Restraints

4.3.1 Stringent Regulatory Scenario

4.3.2 Availability of Effective First-line Treatments

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value – USD million)

5.1 By Product Type

5.1.1 Coronary Stents

5.1.1.1 Bare Stents

5.1.1.2 Drug-eluting Stents

5.1.1.3 Bioabsorbable Stents

5.1.2 Catheters

5.1.2.1 Angiography Catheters

5.1.2.2 Intravascular Ultrasound (IVUS) Catheters

5.1.2.3 Percutaneous Transluminal Coronary Angioplasty (PTCA) Guiding Catheters

5.1.3 Percutaneous Transluminal Coronary Angioplasty (PTCA) Balloons

5.1.4 Percutaneous Transluminal Coronary Angioplasty (PTCA) Guide Wires

5.1.5 Other Product Types

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Mexico

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 United Kingdom

5.2.2.3 France

5.2.2.4 Italy

5.2.2.5 Spain

5.2.2.6 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 Japan

5.2.3.3 India

5.2.3.4 Australia

5.2.3.5 South Korea

5.2.3.6 Rest of Asia-Pacific

5.2.4 Middle-East and Africa

5.2.4.1 GCC

5.2.4.2 South Africa

5.2.4.3 Rest of Middle-East and Africa

5.2.5 South America

5.2.5.1 Brazil

5.2.5.2 Argentina

5.2.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Abbott Laboratories

6.1.2 B. Braun Melsungen AG

6.1.3 Biosensors International Group Ltd

6.1.4 Biotronik SE and Co. KG

6.1.5 Boston Scientific Corporation

6.1.6 Cardinal Health Inc.

6.1.7 Cook Medical Inc.

6.1.8 Medtronic PLC

6.1.9 Terumo Medical Corporation

6.1.10 Edwards Lifesciences Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Interventional Cardiology Devices Industry Segmentation

As per the scope of this report, interventional cardiology is the sub-specialty of cardiology that uses intravascular catheter-based techniques with fluoroscopy to treat coronary artery, valvular, and congenital cardiac diseases. The Interventional Cardiology Devices Market is Segmented by Product Type (Coronary Stents, Catheters, Percutaneous Transluminal Coronary Angioplasty (PTCA) Balloons, Percutaneous Transluminal Coronary Angioplasty (PTCA) Guide Wires, and Other Product Types) and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report offers the value (in USD billion) for the above segments. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD billion) for the above segments.

| By Product Type | |||||

| |||||

| |||||

| Percutaneous Transluminal Coronary Angioplasty (PTCA) Balloons | |||||

| Percutaneous Transluminal Coronary Angioplasty (PTCA) Guide Wires | |||||

| Other Product Types |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Interventional Cardiology Devices Market Research FAQs

How big is the Global Interventional Cardiology Devices Market?

The Global Interventional Cardiology Devices Market size is expected to reach USD 16,080.23 million in 2023 and grow at a CAGR of 5.30% to reach USD 20,817.76 million by 2028.

What is the current Global Interventional Cardiology Devices Market size?

In 2023, the Global Interventional Cardiology Devices Market size is expected to reach USD 16,080.23 million.

Who are the key players in Global Interventional Cardiology Devices Market?

Cook Medical Inc., Abbott Laboratories, Boston Scientific Corporation, Terumo Medical Corporation and Medtronic plc are the major companies operating in the Global Interventional Cardiology Devices Market.

Which is the fastest growing region in Global Interventional Cardiology Devices Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Global Interventional Cardiology Devices Market?

In 2023, the North America accounts for the largest market share in the Global Interventional Cardiology Devices Market.

Global Interventional Cardiology Devices Industry Report

Statistics for the 2023 Global Interventional Cardiology Devices market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Global Interventional Cardiology Devices analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.