Pet Food Market Size

| Study Period | 2018 - 2028 |

| Market Size (2023) | USD 119.59 Billion |

| Market Size (2028) | USD 153.36 Billion |

| CAGR (2023 - 2028) | 5.10 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Pet Food Market Analysis

The Pet Food Market size is expected to grow from USD 119.59 billion in 2023 to USD 153.36 billion by 2028, at a CAGR of 5.10% during the forecast period (2023-2028).

The COVID-19 pandemic negatively impacted supply chains globally. Owing to the restrictions in the movement of raw materials, the pet food industry suffered initially in terms of supply and cash flow. On the other hand, demand for the pet food segment witnessed a steady growth in many parts of the world as people adopted more pets in line with the growing desire for companionship during the lockdown. To address this demand, market players shifted their focus from retail stores to e-commerce platforms by increasing their investments in developing their websites.

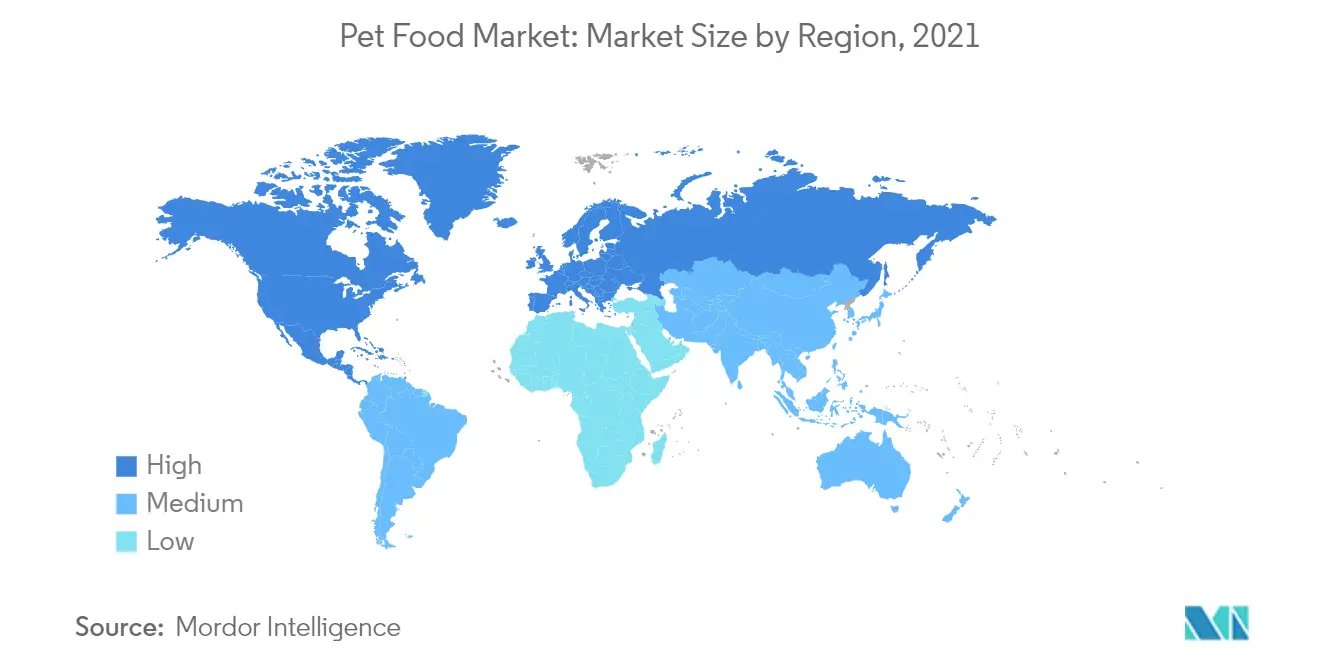

In 2021, North America held the largest share of the market studied and accounted for around 41.7% of the overall market. The pet food industry is one of those industries that have been performing well, despite the economic downturn. The world's largest pet food markets are the US, the UK, France, Brazil, Russia, Germany, and Japan. Pet food manufacturers are offering premium products targeted toward pet owners due to the increased parenting of pets. Young pet owners are willing to spend more on healthy and natural pet food to maintain the well-being of their companion animals. The popularity of premium pet food among pet owners positively impacts the pet food market, and it is expected to contribute to significant growth during the forecast period.

The global pet food market is anticipated to grow over the forecast period due to increasing pet parenting and growing awareness of feeding pets with premium and packed pet food. Over the long term, premiumization and humanization trends are anticipated to remain the key drivers for market growth during the forecast period. Due to the rising pet humanization trend globally, there is a growing interest among pet owners in their pet health and nutrition, which is expected to boost the sales of organic, premium, and custom-made products over the forecast period.

Pet Food Market Trends

This section covers the major market trends shaping the Pet Food Market according to our research experts:

Rising Trend of Pet Humanization

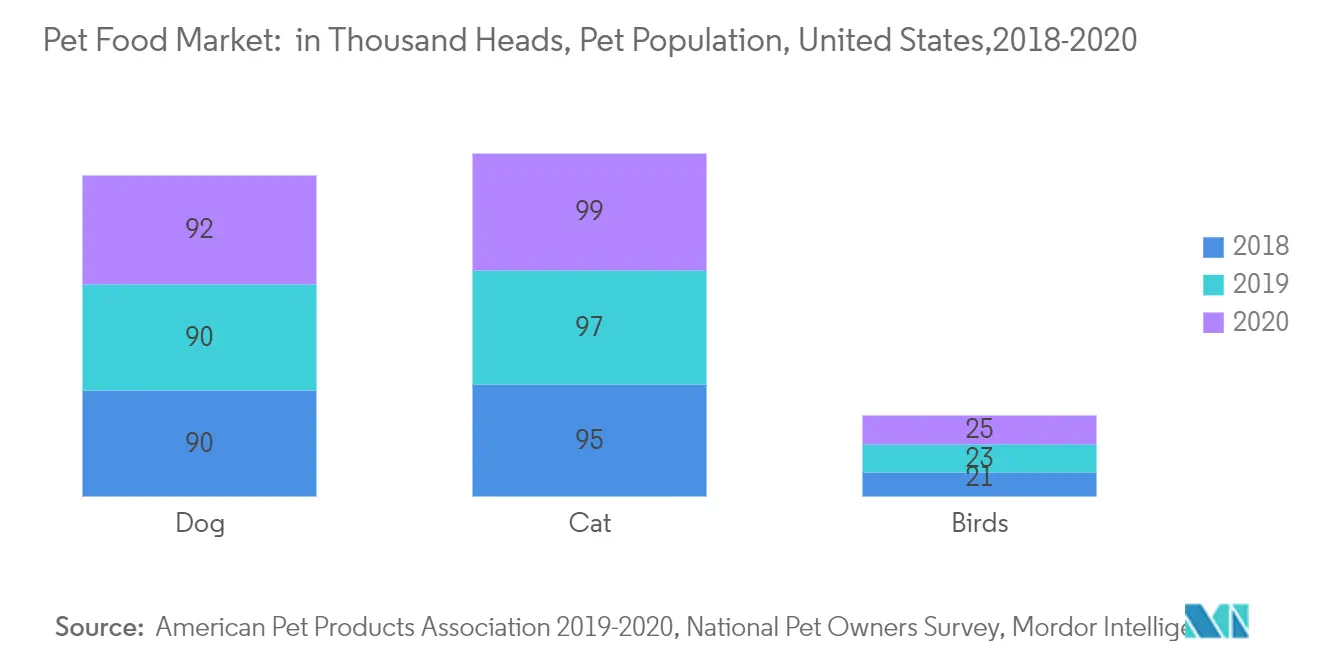

Globally, pet humanization has received a lot of attention in mainstream media in the recent past. The shift from pet ownership to pet parenting has been a crucial and defining trend in the pet food market, especially in developed countries. Over one-third of the households in developed countries own a pet. A study conducted by the American Pet Products Association (APPA), under the National Pet Owners Survey (2019-20), revealed that more than 85 million households in the US had one or more pets, the majority of them being dogs. Thus, increasing pet humanization is anticipated to drive the pet food industry.

As a part of this pet humanization trend, nowadays, pets are considered a part of the family. The growing bond between pet owners and their pets shapes consumers’ willingness to spend more on pet food. Consumers are now becoming aware of their pet’s health and are buying pet food rich in nutritional value for the betterment of their beloved pets. Nowadays, pet owners are not just looking for basic food products but also for pet consumables that are locally produced and natural or have specific health benefits.

Additionally, the pet humanization trend has led to increased health consciousness and has generated demand for pet food free from sugar, grain, dye, and other chemical additives. Hence, with the emerging pet humanization and premiumization trends, the pet food demand is anticipated to grow further over the coming years.

North America Dominates the Market

Increasing pet humanization and pet ownership, the emergence of private label store brands, and growing urbanization accompanied by increased disposable incomes are some of the major forces propelling the North American pet food market's growth. The market is driven by heavy influences from human nutrition, driving research toward better and safer food for pets with high nutritional and dietary benefits. Additionally, locally-sourced products and ethically-sourced products are propelling the market, as local manufacturers are expanding their presence in the domestic market. According to the American Pet Products Association’s (APPA) National Pet Owners Survey 2019-20, 63.4 million households own dogs as pets, which is about 74.6% of the country's total pet-owning households. This, accompanied by dog owners' rising focus on purchasing healthy and nutritious food for their pets, is helping drive the sales of different types of dog foods in the US.

Pet owners are showing a preference for functional treats compared to other treats, as the former offer additional health benefits for their pets. Owing to this trend, major players in the market are developing new functional treats to meet the pet owners’ demand. For instance, in 2019, Hill’s Pet Nutrition launched its new range of functional dog treats specifically designed to aid dogs' weight, mobility, food allergies, and dental problems.

Pet Food Industry Overview

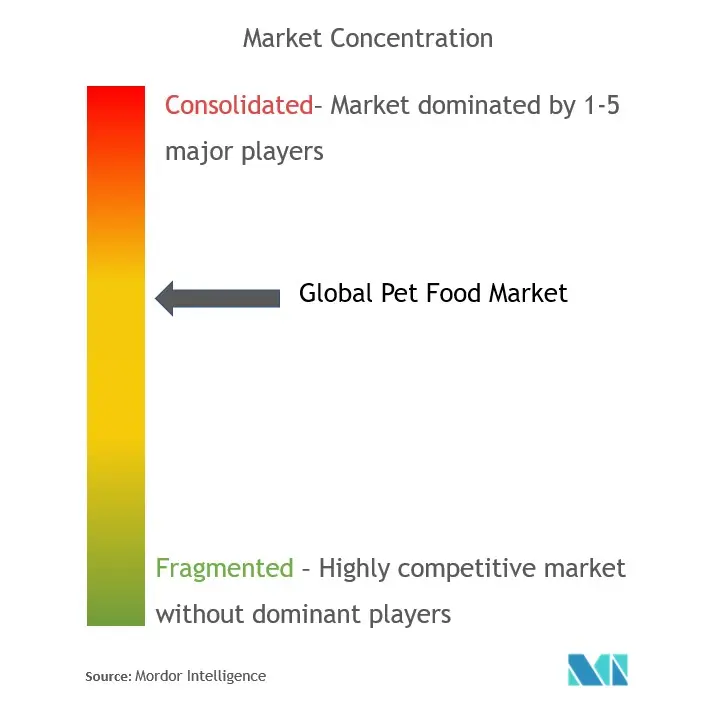

The global pet food market is moderately consolidated in nature. The significant players accounted for the majority of the market share in 2021. The adoption of new strategies by existing players has resulted in the domination by a few players in the market. In 2021, Mars Incorporated dominated the market studied, followed by Nestle Purina Pet Food, Colgate Palmolive, JM Smucker Company, and Diamond Pet Foods.

Pet Food Market Leaders

Mars, Inc.

The J.M. Smucker Company (Big Heart Pet Brands, Inc.)

Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

Nestle Purina Petcare Company

Schell & Kampeter, Inc. (Diamond Pet Food)

*Disclaimer: Major Players sorted in no particular order

Pet Food Market News

In July 2021, Nestlé Purina PetCare Co. invested USD 182 million to expand its pet care products’ manufacturing facility in King William County, Virginia, US. The factory expansion, which is scheduled to be completed by late 2023, will include a 138,000 square foot buildout to increase manufacturing capacity for the company’s Tidy Cat litter products line.

In June 2021, Mars Inc. launched wet cat food under its Whiskas brand, expanding its product range in India. The new product range is available across pet shops, grocery stores, and e-commerce sites.

In June 2021, Hill's Pet Nutrition opened a 25,000 square foot nutrition innovation center in the US. This center would enable the company to develop innovative products specially designed for small and mini dogs.

Pet Food Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitutes

4.4.5 Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Animal Type

5.1.1 Dogs

5.1.2 Cats

5.1.3 Birds

5.1.4 Other Animal Types

5.2 Product Type

5.2.1 Dry Pet Food

5.2.2 Wet Pet Food

5.2.3 Veterinary Diets

5.2.4 Treats and Snacks

5.2.5 Organic Products

5.3 Ingredient Type

5.3.1 Animal-derived

5.3.2 Plant-derived

5.3.3 Cereals and Cereal Derivatives

5.3.4 Other Ingredient Types

5.4 Distribution Channel

5.4.1 Specialized Pet Shops

5.4.2 Supermarkets/Hypermarkets

5.4.3 Online Channel

5.4.4 Other Distribution Channels

5.5 Geography

5.5.1 North America

5.5.1.1 US

5.5.1.2 Canada

5.5.1.3 Mexico

5.5.1.4 Rest of North America

5.5.2 Europe

5.5.2.1 Germany

5.5.2.2 UK

5.5.2.3 France

5.5.2.4 Italy

5.5.2.5 Spain

5.5.2.6 Russia

5.5.2.7 Rest of Europe

5.5.3 Asia-Pacific

5.5.3.1 China

5.5.3.2 Japan

5.5.3.3 India

5.5.3.4 Australia

5.5.3.5 Rest of Asia-Pacific

5.5.4 South America

5.5.4.1 Brazil

5.5.4.2 Argentina

5.5.4.3 Rest of South America

5.5.5 Middle-East and Africa

5.5.5.1 South Africa

5.5.5.2 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Most Adopted Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 Mars Incorporated

6.3.2 Nestle Purina Petcare Company

6.3.3 The JM Smucker Company (Big Heart Pet Brands Inc.)

6.3.4 Nutriara Alimentos Ltda

6.3.5 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

6.3.6 General Mills Blue Buffalo Pet Products Inc.

6.3.7 Clearlake Capital Group (WellPet LLC)

6.3.8 Yamahisa Pet Care (Petio)

6.3.9 ADM Animal Nutrition (InVivo NSA)

6.3.10 Schell & Kampeter Inc. (Diamond Pet Foods)

6.3.11 Alltech Inc.

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. AN ASSESSMENT OF THE IMPACT OF COVID-19

Pet Food Industry Segmentation

Pet food refers to food, either plant-based or animal-based, specifically formulated and intended for consumption by pets. The pet food market is segmented by animal type (dogs, cats, birds, and other animal types), product type (dry pet food, wet pet food, veterinary diets, treats and snacks, and organic products), ingredient type (animal-derived, plant-derived, cereals and cereal derivatives, and other ingredient types), distribution channel (specialized pet shops, supermarkets/hypermarkets, online channel, and other distribution channels), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers the market size for all the above segments in terms of value (USD million).

| Animal Type | |

| Dogs | |

| Cats | |

| Birds | |

| Other Animal Types |

| Product Type | |

| Dry Pet Food | |

| Wet Pet Food | |

| Veterinary Diets | |

| Treats and Snacks | |

| Organic Products |

| Ingredient Type | |

| Animal-derived | |

| Plant-derived | |

| Cereals and Cereal Derivatives | |

| Other Ingredient Types |

| Distribution Channel | |

| Specialized Pet Shops | |

| Supermarkets/Hypermarkets | |

| Online Channel | |

| Other Distribution Channels |

| Geography | |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

|

Pet Food Market Research FAQs

How big is the Pet Food Market?

The Pet Food Market size is expected to reach USD 119.59 billion in 2023 and grow at a CAGR of 5.10% to reach USD 153.36 billion by 2028.

What is the current Pet Food Market size?

In 2023, the Pet Food Market size is expected to reach USD 119.59 billion.

Who are the key players in Pet Food Market?

Mars, Inc., The J.M. Smucker Company (Big Heart Pet Brands, Inc.), Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), Nestle Purina Petcare Company and Schell & Kampeter, Inc. (Diamond Pet Food) are the major companies operating in the Pet Food Market.

Which is the fastest growing region in Pet Food Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Pet Food Market?

In 2023, the North America accounts for the largest market share in the Pet Food Market.

Pet Food Industry Report

Statistics for the 2023 Pet Food market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Pet Food analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.