Hazardous Goods Logistics Market Size

| Study Period | 2019-2028 |

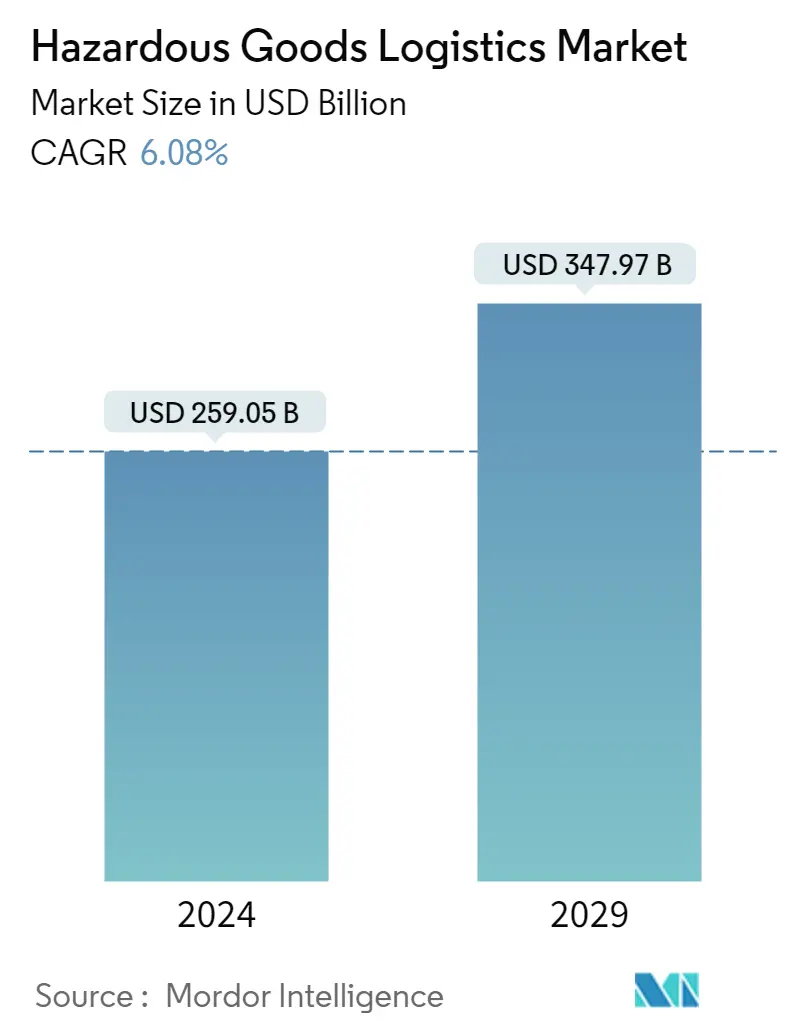

| Market Size (2023) | USD 244.20 Billion |

| Market Size (2028) | USD 328.03 Billion |

| CAGR (2023 - 2028) | 6.08 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Hazardous Goods Logistics Market Analysis

The Hazardous Goods Logistics Market size is expected to grow from USD 244.20 billion in 2023 to USD 328.03 billion by 2028, at a CAGR of 6.08% during the forecast period (2023-2028).

- The requirement to ship dangerous goods is anticipated to increase yearly, in addition to the numerous dangerous goods rules being updated annually. The need for UN packaging, training, labels, and placards will rise as a result of the growing requirement to move lithium batteries and the region's well-established gas and oil businesses, which are both driving the dangerous goods market to record highs.

- Around 4% of the transit of risky items took place at the EU level in both 2021 and 2020. The EU Member States with the highest percentages of dangerous commodities in their road transportation were Finland (7.4% in 2020 and 6.9% in 2021) and Cyprus (12.3% in 2020 and 10.9% in 2021). These two countries were followed by Belgium (9.4% in 2020 and 8.3% in 2021). Several EU nations, including the large nations of France, Spain, and Italy, reported statistics that fell between the range of 4% and 7%. Poland had shares of 2.3% in 2020 and 2.4% in 2021, compared to Germany's 3.9% in 2020 and 3.8% in 2021. Slovakia, Lithuania, and Ireland, in contrast, saw proportions of harmful goods fall below 2% in 2020.

- The key to successfully transporting hazardous goods is digitization. A digital supply network serves as a technology platform for supply chain linkages and cross-business processes in transportation operations. It links suppliers, customers, shippers, and third-party logistics providers so they can work together more effectively and conduct business. Automated systems translate paper or email into the proper forms so that the document can be shared electronically with other people. This includes manual operations like completing a purchase order, recognizing the receipt of the order, and shipping confirmation.

- The lockdown during the COVID-19 pandemic created impediments to transporting chemicals and other dangerous goods, thereby hampering the growth of the hazardous goods logistics market. However, the demand from the pharmaceutical sector during COVID-19 had a positive impact on the market.

Hazardous Goods Logistics Market Trends

This section covers the major market trends shaping the Hazardous Goods Logistics Market according to our research experts:

Increase in shipment of flammable liquids driving the market

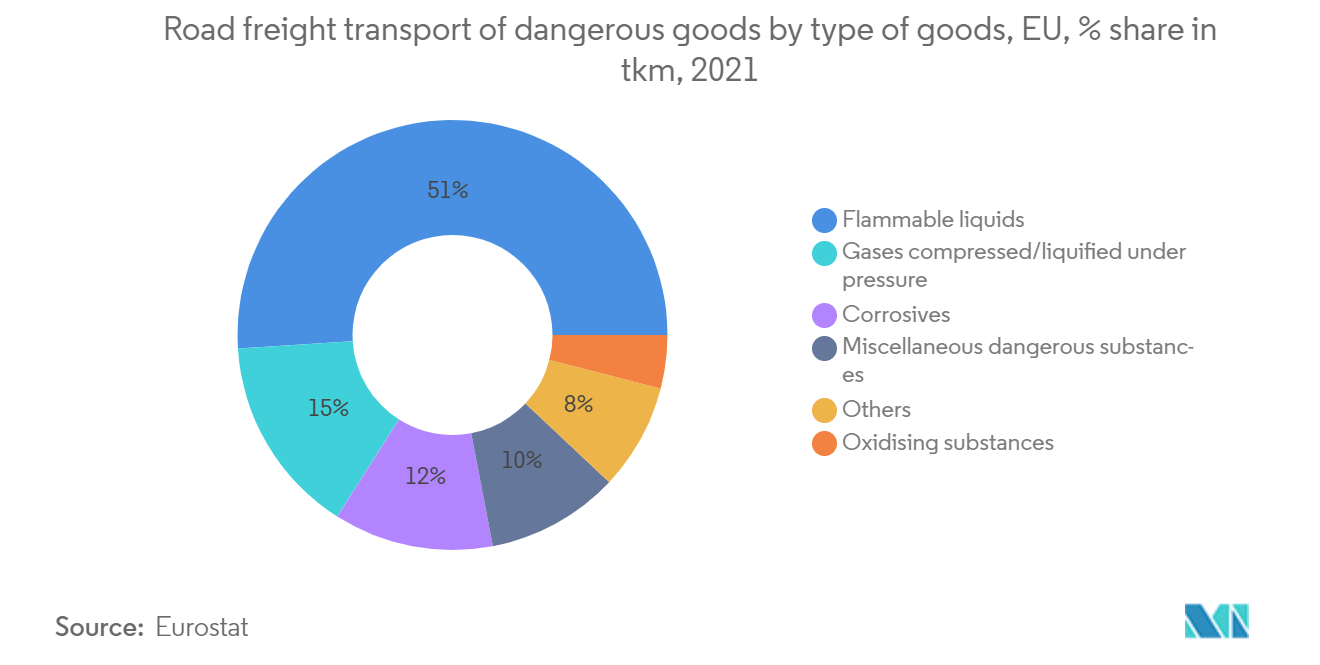

The share of hazardous chemicals in all freight traffic is rising quickly due to the chemical industry's tremendous growth. About two-thirds of the carriers that transport hazardous commodities also transport flammable petroleum liquids, including kerosene, petrol, LPG, naphtha, etc. Such compounds are more likely to be involved in accidents during transportation than other types of cargo. Involvement in a traffic accident can have disastrous results, including fire, explosion, injury, loss of property, and environmental damage.

The flammable liquid shipments account for most of the demand. For instance, in 2021, more than half of the freight traffic in dangerous goods transportation by road in Europe will be related to flammable liquids, followed by compressed gasses and corrosives.

57% of all rail tank cars in the United States carrying Class 3 flammable liquids were constructed in 2021 to the new DOT-117 or DOT-117R criteria. In 2021, there were no phase-out deadlines. The next significant deadline comes in 2023, when the transport of ethanol will be restricted on all DOT-111 and CPC-1232 tank cars. By 2021, the vast majority (78%) of ethanol-carrying vehicles would have met the new DOT-117 requirements.7,473 tank cars carrying ethanol were in service under the DOT-111 and CPC-1232 standards; these vehicles will be replaced by DOT-117 vehicles. According to survey findings, 8,322 DOT-117 and DOT-117R tank cars are expected to be produced or upgraded in 2022.

Class 3 flammable substances were transported in 103,312 rail tank cars in 2021, up 57% from just five years earlier. The percentage of DOT-117 tank cars in the fleet for crude oil alone increased from 81% in 2020 to 87% in 2021.

Increase in chemical production driving the market

The growth in the output of chemical manufacturing from countries across the world is expected to drive the demand for dangerous goods logistics over the forecast period. The U.S. chemical industry was ready for significant production increases in 2021 after two years of weakness attributed to trade tensions and COVID-19. But in February, a huge swath of chemical and other industrial capacity was shut down when winter storm Uri brought icy conditions and power outages to the Gulf Coast. Due to a lack of raw materials, some other facilities had to shut down or scale back their operations. The manufacture of numerous essential chemicals was halted for more than a month in August due to Hurricane Ida. This year's lower demand for some chemicals was also influenced by supply chain problems in significant end-use areas. In the future, things look promising.

Exports of organic compounds from the United States in December 2022 were up toUSD 4.4 billion, while imports were up to USD 5.44 billion, resulting in a USD 1.04 billion trade deficit. The exports of organic chemicals from the United States rose by USD 338 million (8.32%) between December 2021 and December 2022, from USD 4.06 billion to USD 4.4 billion, while imports fell by USD 143 million (-2.57%), from USD 5.58 billion to USD 5.44 billion. In December 2022, organic chemicals were primarily imported from Ireland (USD 1.75B), China (USD 962M), Mexico (USD 526M), Switzerland (USD 360M), Germany (USD 278M), and India (USD 264M). They were primarily shipped to Austria (USD 606M), Mexico (USD 526M), China (USD 395M), Belgium (USD 345M), and Canada (USD 344M).

In December 2022, a rise in exports to Mexico (USD 222M or 53.5%), Belgium (USD 203M or 71%), and South Korea (USD 144M or 82.3%) was the main factor contributing to an increase in Organic chemicals' year-over-year exports. The decline in imports of organic chemicals from Singapore (USD 190M or -49.3%), Argentina (USD -38.7M or -96.4%), and Belgium (USD 38.5M or -29.4%) in December 2022 can be attributed mainly to these declines.

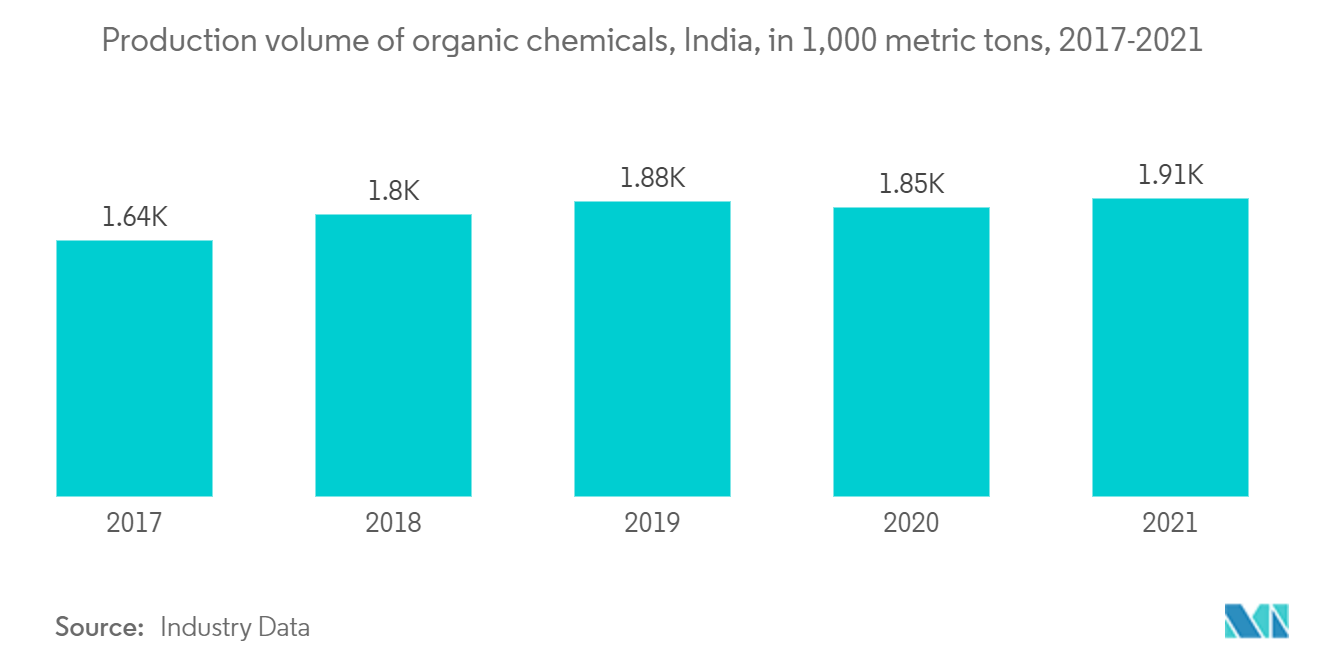

The chemicals sector has also been attracting high growth rates in developing countries. For instance, the SMEs in the Indian chemical manufacturing sector are expected to witness revenue growth of around 20% owing to an improvement in domestic demand and higher realization due to the high prices of chemicals. A revival in domestic demand post-pandemic and robust exports are driving the chemical industry's production in India.

Hazardous Goods Logistics Industry Overview

The Hazardous Goods Logistics Market is fragmented by nature, with a mix of global and local players. Some of the strong players include DHL, DSV, Ceva Logistics, Bollore Logistics, and DGD Transport. Contracts, collaborations, joint ventures, and partnerships are among many other strategies that have been implemented by these players to stay ahead of the competition and meet the expanding needs of their clients. Furthermore, they are engaging in research and development operations to strengthen their portfolios and gain market share. The capabilities of local players in terms of technology, items handled, service offered, and inventory management are all improving. With the tightening of hazardous goods logistics regulations, an increasing number of freight forwarding businesses have emerged that can provide competent hazardous goods logistics full-chain services independently.

Hazardous Goods Logistics Market Leaders

DHL

DSV

Ceva Logistics

Bollore Logistics

DGD Transport

*Disclaimer: Major Players sorted in no particular order

Hazardous Goods Logistics Market News

- October 2022: Chemet will incorporate cutting-edge Nexxiot technology into recently produced railway tank carriages. One of the top producers of stationary and portable pressure tanks and vessels for liquefied gasses in Europe, Chemet, has chosen Nexxiot to digitize its line of railroad tank cars. The first European company to commit to fully digitizing its rail tank car offerings is Chemet, which has offices in both France and Poland.

- March 2022: Drone Delivery Canada Corp. reported that the intra-site drone delivery route for DSV Air & Sea Inc. Canada ("DSV") has successfully received clearance and has been put into operation for the transfer of dangerous items. The DroneSpotsTM at DSV's Milton, Ontario, warehouse may transport dangerous goods ("DG") and consumer goods via this route.

Hazardous Goods Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS AND DYNAMICS

4.1 Current Market Scenario

4.2 Industry Value Chain Analysis

4.3 Government Regulations and Initiatives

4.4 Brief on Dangerous Goods Classes

4.5 Review and Commentary on Goods Transport Regulations and Standards (Hazardous Materials Transportation Act (HMTA), International Air Transport Association Dangerous Goods Regulations (IATA DGR), etc.)

4.6 Focus on Key Stakeholders in Supply Chain (Freight Forwarders, Ground Handling Agents, Carriers, Advisors and Consultants, etc.)

4.7 Key Information - Documentation, Special Permissions, and Safety Checklists

4.8 Spotlight - Equipment and Accessories Associated with Transport of Dangerous Goods (Air, Sea, and Road)

4.9 Potential Risk Involved in Shipment of Hazardous Materials

4.10 Insights on Packaging

4.11 Technology Snapshot (Digitalization and Process Optimization and Management Software, e-Dangerous Goods Declaration (eDGD), etc.)*

4.12 Impact of COVID-19 on the Market

4.13 Market Dynamics

4.13.1 Market Drivers

4.13.2 Market Restraints/Challenges

4.13.3 Market Opportunities

4.14 Industry Attractiveness - Porter's Five Forces Analysis

4.14.1 Bargaining Power of Buyers/Consumers

4.14.2 Bargaining Power of Suppliers

4.14.3 Threat of New Entrants

4.14.4 Threat of Substitute Products

4.14.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By Service

5.1.1 Transportation

5.1.2 Warehousing and Distribution

5.1.3 Value-added Services

5.2 By Destination

5.2.1 Domestic

5.2.2 International

5.3 By Geography

5.3.1 Asia-Pacific

5.3.2 North America

5.3.3 Europe

5.3.4 Latin America

5.3.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Overview (Market Concentration and Major Players)

6.2 Company Profiles

6.2.1 Deutsche Post DHL Group

6.2.2 DSV

6.2.3 Ceva Logistics

6.2.4 Bollore Logistics

6.2.5 DGD Transport

6.2.6 Toll Group

6.2.7 YRC Worldwide Inc.

6.2.8 DB Schenker

6.2.9 Hellmann Worldwide Logistics

6.2.10 Agility Logistics

6.2.11 Kuehne + Nagel

6.2.12 XPO Logistics

6.2.13 United Parcel Service

6.2.14 GEODIS

6.2.15 Rhenus Logistics*

- *List Not Exhaustive

7. FUTURE OF THE MARKET

8. APPENDIX

8.1 GDP Distribution, by Activity - Key Countries

8.2 Insights on Capital Flows - Key Countries

8.3 Global Dangerous Goods Flow Statistics

8.4 External Trade Statistics - Exports and Imports, by Product and by Country of Destination/Origin

Hazardous Goods Logistics Industry Segmentation

Corrosive, flammable, explosive, spontaneously combustible, poisonous, oxidizing, or water-reactive compounds are classified as hazardous goods. Logistics refers to the overall process of managing how resources are acquired, stored, and transported to their final destination.

A complete background analysis of the hazardous goods logistics market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is included in the report. The Hazardous Goods Logistics Market is segmented by Service (Transportation, Warehousing and Distribution, Value-added Services), Destination (Domestic, International), and Geography (Asia-Pacific, North America, Europe, Latin America, Middle East, and Africa). The report offers market size and forecasts for the Hazardous Goods Logistics market in value (USD billion) for all the above segments.

| By Service | |

| Transportation | |

| Warehousing and Distribution | |

| Value-added Services |

| By Destination | |

| Domestic | |

| International |

| By Geography | |

| Asia-Pacific | |

| North America | |

| Europe | |

| Latin America | |

| Middle East and Africa |

Hazardous Goods Logistics Market Research FAQs

How big is the Hazardous Goods Logistics Market?

The Hazardous Goods Logistics Market size is expected to reach USD 244.20 billion in 2023 and grow at a CAGR of 6.08% to reach USD 328.03 billion by 2028.

What is the current Hazardous Goods Logistics Market size?

In 2023, the Hazardous Goods Logistics Market size is expected to reach USD 244.20 billion.

Who are the key players in Hazardous Goods Logistics Market?

DHL, DSV, Ceva Logistics, Bollore Logistics and DGD Transport are the major companies operating in the Hazardous Goods Logistics Market.

Which is the fastest growing region in Hazardous Goods Logistics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (20221-2028).

Which region has the biggest share in Hazardous Goods Logistics Market?

In 20221, the North America accounts for the largest market share in Hazardous Goods Logistics Market.

Hazardous Goods Logistics Industry Report

Statistics for the 2023 Hazardous Goods Logistics market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Hazardous Goods Logistics analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.