India Data Center Market Size

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2018 - 2028 |

|

|

Base Year For Estimation | 2022 |

|

|

Market Size (2023) | USD 6.12 Billion |

|

|

Market Size (2028) | USD 10.89 Billion |

|

|

CAGR (2023 - 2028) | 12.22 % |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

India Data Center Market Analysis

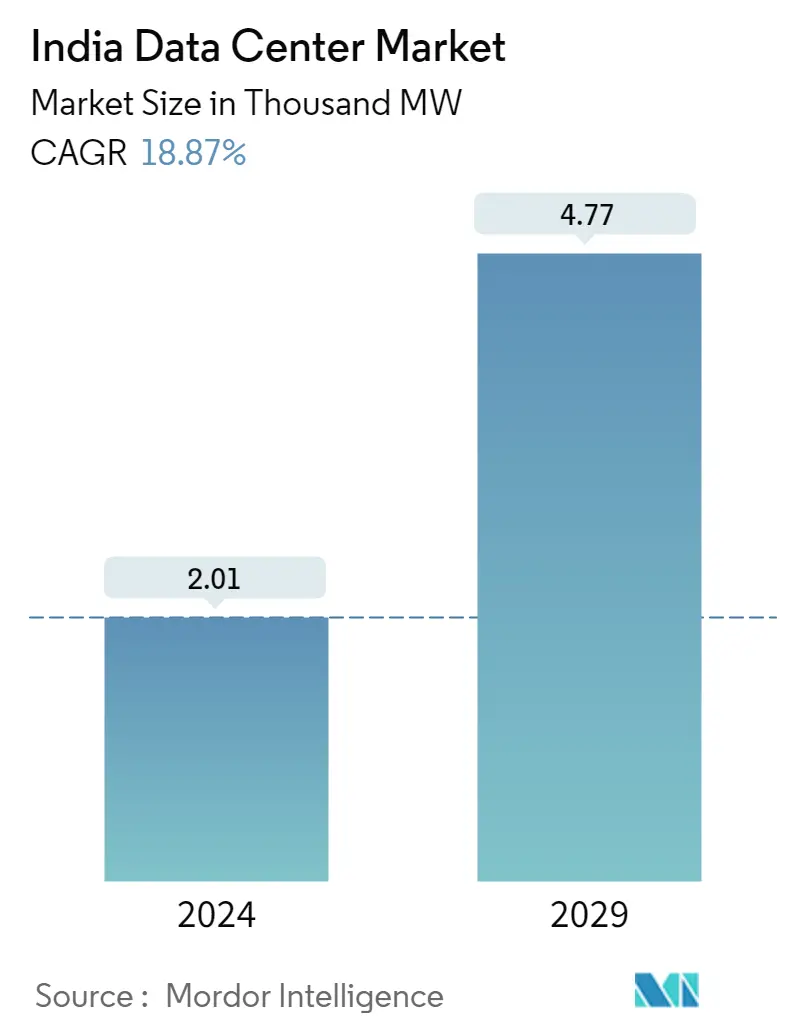

The India Data Center Market size is expected to grow from USD 6.12 billion in 2023 to USD 10.89 billion by 2028, at a CAGR of 12.22% during the forecast period (2023-2028).

The rapid adoption of cloud-based business operations has encouraged businesses to acquire data management capacities to handle huge volumes of data that are being generated. Increased proliferation of online shopping due to the availability of user-friendly interfaces, high-speed internet, and smart devices such as smartphones, tablets, laptops, etc., is expected to drive the market in the future.

- India is among the APAC region's major players in the data center sector. Data centers are critical for national security, internet infrastructure, and economic output. In India, data center infrastructure is growing exponentially, with a growing preference for the Cloud and increased data consumption and generation by over half a billion digital users.

- For companies that undertake the cloud migration process, the Cloud can have a huge impact. This includes reducing the total cost of ownership (TCO), quicker delivery, and better prospects for innovation. Agility and flexibility, two essential qualities to satisfy changing consumer and industry demands, come with access to the Cloud. The migration of businesses to the Cloud has increased recently as they shift into more flexible digital workplaces to deal with the increase in online demand and remote working. Although the Cloud is the foundation of digital transformation, cloud services are built on data centers. Due to this, the cloud migration of businesses is driving the growth of the data centers market in India.

- India is becoming the global destination for setting up data centers. But it could also reinforce its position as a global hub for green data centers. Demand for new data centers is enormous in India, driven by the hyperscale facilities key internet players, such as Amazon Web Services (AWS), Microsoft, Google Cloud, and Alibaba Cloud, demand to power their clouds.

- Datacenter establishment in India is cost-intensive, a barrier to entering the industry for many data center companies. Prevalent norms for commercial buildings applied to data centers lead to wastage of space and increased cost. Besides, factors such as high real estate costs, expenses on improving wide area network connectivity, and increased equipment costs have also augmented the heavy CapEx in the sector.

- The COVID-19 pandemic led to a new wave of digital transformation in various sectors across the country. Businesses rapidly turn to third-party colocation facilities for data center operations, further complemented by an increased shift toward a hybrid IT approach that leverages the combined capabilities of hosted data centers and multi-cloud setups.

India Data Center Market Trends

Government Support in the Form of Tax Incentives for Development of Data Centers is Expected to Drive the Market Growth

- The Government of India and various state governments are revising their data center policies to support the infrastructural growth of data centers in India through tax subsidies. Under a national policy framework for data centers, the IT ministry intends to provide up to INR 15,000 crore (USD 1.83 Million) as incentives. The government plans to invest up to Rs 3 lakh crore (USD 36.5 Million) in the data center ecosystem, over the next five years, as per the policy.

- The Government of Maharashtra announced the GST refund for a maximum period of 10 years for the companies that participate in developing integrated facilities. Similarly, the Andhra Pradesh government announced providing 50% reimbursement of SGST on purchasing raw materials and equipment for three years from the approval date of the project.

- Tamil Nadu government announced a data center policy that allows the data centers to avail of an Electricity TAX waiver. For five years following the start of commercial operation, there is a 100% electricity tax subsidy on power obtained from the Tamil Nadu Generation and Distribution Corporation Ltd. or generated and consumed using captive sources.

- The Odisha government announced a data center policy that offers a 100% reimbursement of net SGST. Net SGST paid in will be fully reimbursed to eligible units, relying on its exports of goods and services for funding limited to 100% of fixed capital investment for a maximum of seven years.

- In June 2022, the Haryana cabinet approved a data center policy to make Haryana a popular location for constructing these facilities and assist the state in becoming a hub for global data centers. The Haryana government would categorize the data center sector as an energy-intensive and infrastructure industry. The government would deem data centers essential by the Haryana Essential Services Maintenance Act of 1974. This policy includes various tax incentives, such as reimbursement of SGST and a land tax rebate.

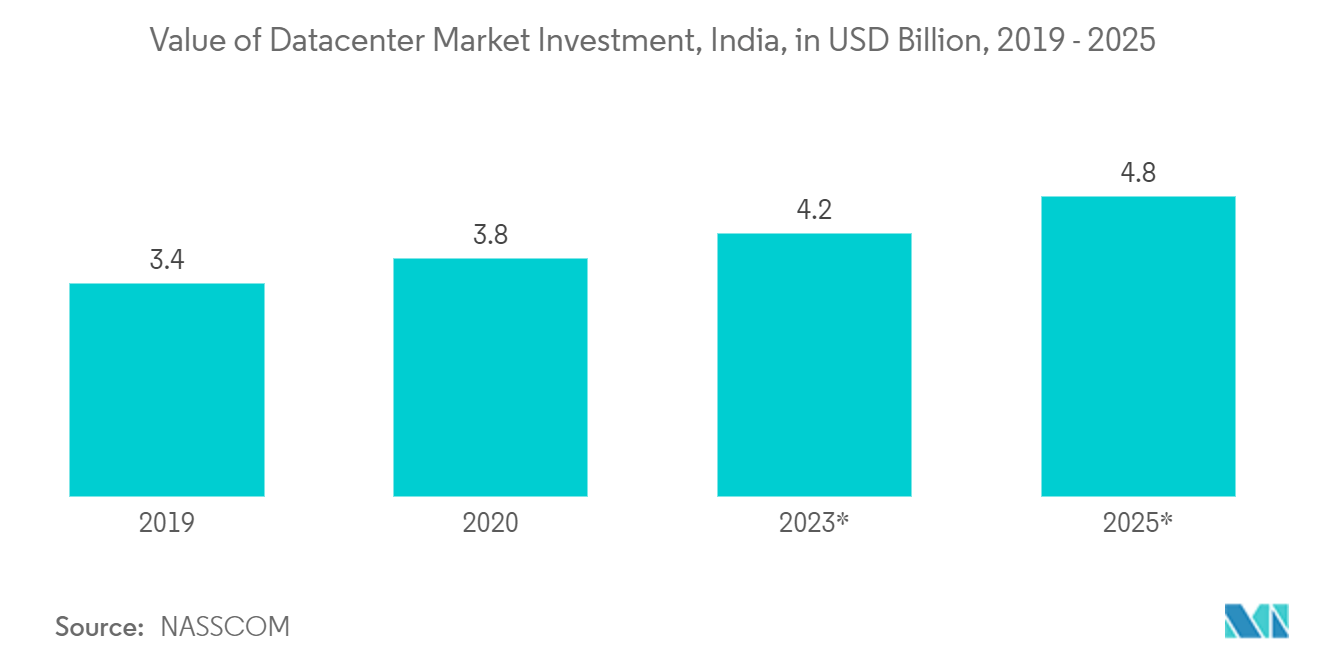

- As per NASSCOM, the Indian data center market would witness cumulative investments of USD 25 billion during 2019-2025. India’s data center market investment is expected to reach USD 4.8 billion in 2025. Investment increase is expected from private equity players, real estate developers, and end occupiers.

Servers IT Infrastructure Type Segment is Expected to Holds Significant Market Share

- In India's data center market, various IT infrastructures are deployed to support server operations. Rack servers are the most common type of servers used in data centers. These servers are mounted in standard racks, which provide easy installation and maintenance.

- Virtualized servers use virtualization technology to run multiple virtual machines on a single physical server. This approach helps maximize resource utilization and improve efficiency in data centers.

- Storage servers are specialized servers dedicated to storing and managing data. They provide high-capacity storage solutions for data-intensive applications and backup purposes.

- Mainframe systems are high-performance servers designed for heavy workloads and large-scale data processing. They are commonly used in enterprise-level data centers.

- With the growth of data-intensive technologies, cloud computing, and digital services, organizations are generating and processing larger volumes of data. Data centers need to scale their server infrastructure to accommodate these increasing workloads. This may involve adding more servers to existing data centers or constructing new data centers altogether.

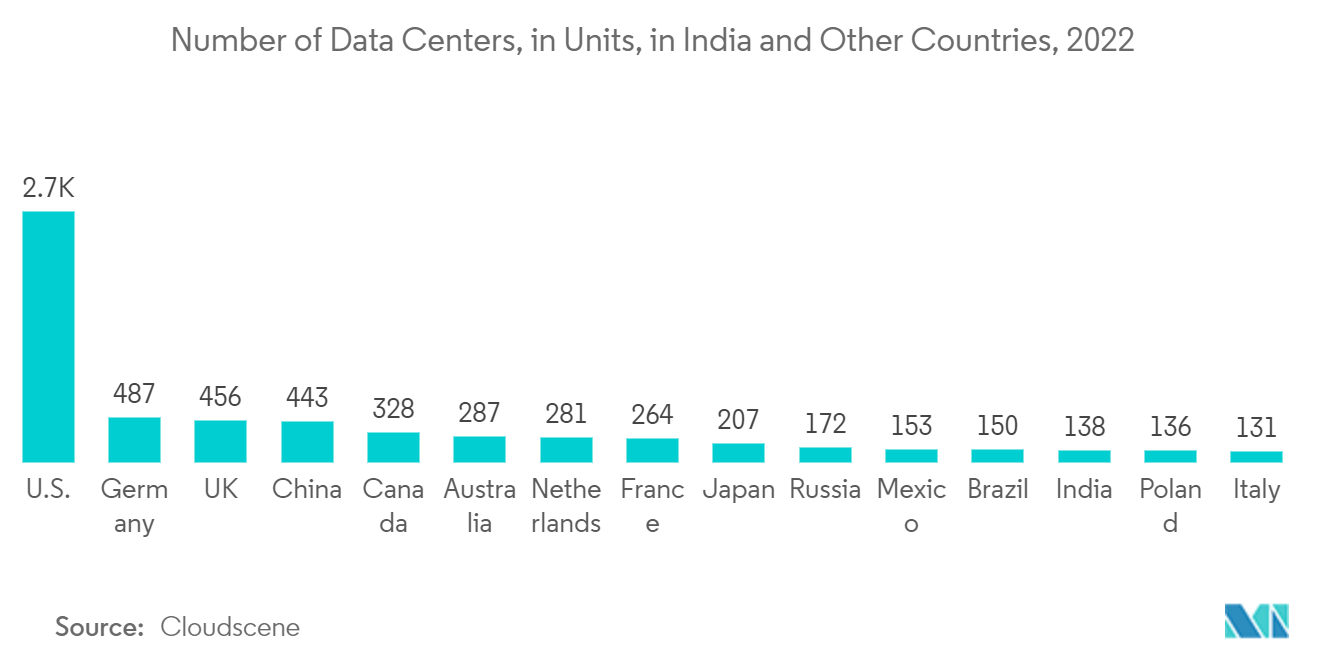

- The increasing number of data centers directly relates to the demand for server IT infrastructure. As the number of data centers grows, there is a corresponding need for more server infrastructure to support the expanding computing requirements. According to Cloudscene, as of January 2022, 138 data centers were in India.

India Data Center Industry Overview

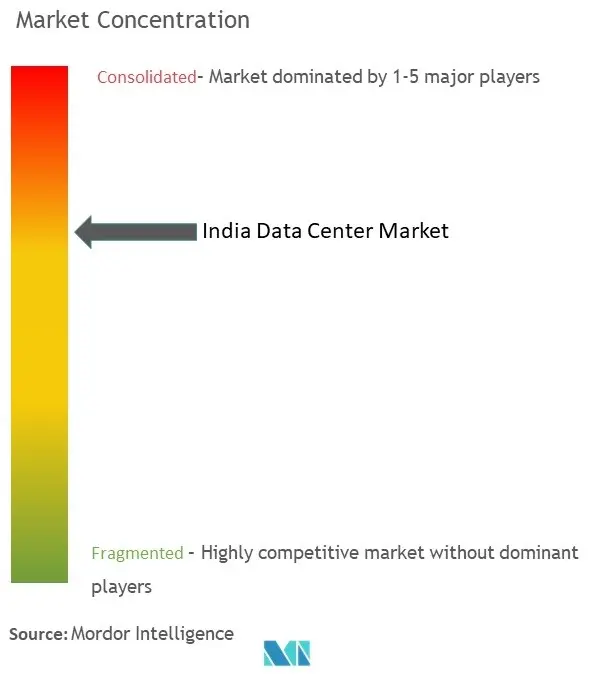

The Indian Data Center Market is highly concentrated due to higher initial investments and low availability of resources. The major players, with a prominent share of the market, are focusing on expanding their customer base across foreign countries. These companies are leveraging strategic collaborative initiatives to increase their market share and increase their profitability. However, with technological advancements and product innovations, mid-size to smaller companies are increasing their market presence by securing new contracts and by tapping new markets.

In May 2022, a strategic partnership between Cyxtera, a collocation service provider, and SifyTechnologies Limited was signed, and it would enable it to start providing colocation solutions in India. Customers in five more markets in India can now use colocation services from Cyxtera.

In May 2022, Cisco Duo launched the data center in Mumbai. The data center would enable all functionality from Duo's zero-trust platform, including multi-factor authentication (MFA), single sign-on (SSO), VPN-less remote access, device trust, password-less (in public preview), and adaptive risk-based policies.

India Data Center Market Leaders

Nikom Infrastructure Private Limited

Trimax IT Infrastructure & Services Limited

Arshiya Limited

Sify Technologies

Sterling & Wilson (Shapoorji Pallonji Group)

*Disclaimer: Major Players sorted in no particular order

India Data Center Market News

- May 2022: NTT India announced the launch of its new hyperscale data center campus, NAV1A, in Navi Mumbai. The latest development takes NTT’s data center footprint in the country to 12 facilities, with more than 2.5 million sq. ft and 220MW of facility power. This launch is near a new data center going live in its Chandivali campus, India’s first operational hyperscale data center campus.

- Jun 2022: Equinix Inc., a US-based digital infrastructure company, announced an initial investment of over USD 86 million to build its third International Business Exchange (IBX) data center in Mumbai, to be named MB3. This initial investment includes an acquisition of a parcel of land, which provides a total space of nearly four acres, allowing Equinix to continue growing its ecosystem on Platform Equinix across India, supporting the country’s growing digital economy.

India Data Center Market Report - Table of Contents

0. INTRODUCTION

0_0. Study Assumptions and Market Definition

0_1. Scope of the Study

1. RESEARCH METHODOLOGY

2. EXECUTIVE SUMMARY

3. MARKET INSIGHTS

3_0. Market Overview

3_1. Industry Attractiveness - Porter's Five Forces Analysis

3_1_0. Bargaining Power of Suppliers

3_1_1. Bargaining Power of Buyers

3_1_2. Threat Of New Entrants

3_1_3. Threat of Substitute Products

3_1_4. Intensity of Competitive Rivalry

3_2. Value Chain Analysis

3_3. Assessment of Impact of COVID-19 on the Market

4. MARKET DYNAMICS

4_0. Market Drivers

4_0_0. Increased Migration to Cloud-based Business Operations

4_0_1. Rise of Green Data Centers

4_0_2. Government Support in the Form of Tax Incentives for Development of Data Centers

4_1. Market Restraints

4_1_0. Higher Initial Investments and Low Availability of Resources

5. MARKET SEGMENTATION

5_0. By Type

5_0_0. Captive

5_0_1. Outsourced (Colocation and Hosting)

5_1. By IT Infrastructure Type

5_1_0. Servers

5_1_1. Storage

5_1_2. Enterprise Networking

5_1_3. Other IT Infrastructure Types

5_2. Key Regions (Based on Current Data Center Activity)

6. ANALYSIS OF MAJOR DATA CENTER CONSTRUCTION COMPONENTS

7. COMPETITIVE LANDSCAPE

7_0. Company Profiles*

7_0_0. Nikom Infrastructure Private Limited

7_0_1. Trimax IT Infrastructure & Services Limited

7_0_2. Arshiya Limited

7_0_3. Sify Technologies

7_0_4. Sterling & Wilson (Shapoorji Pallonji Group)

7_0_5. Hewlett Packard Enterprise (HPE)

7_0_6. Atos

7_0_7. Arista

7_0_8. Huawei

7_0_9. Cisco India

7_0_10. Delta Group

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

List of Tables & Figures

- Figure 1:

- INDIA DATA CENTER MARKET, IT LOAD CAPACITY, VOLUME IN MW, 2017 - 2029

- Figure 2:

- INDIA DATA CENTER MARKET, RAISED FLOOR SPACE, VOLUME IN SQ. FT.(000'), 2017 - 2029

- Figure 3:

- INDIA DATA CENTER MARKET, COLOCATION REVENUE, VALUE IN USD MILLION, 2017 - 2029

- Figure 4:

- INDIA DATA CENTER MARKET, INSTALLED RACKS, VALUE IN UNIT, 2017 - 2029

- Figure 5:

- INDIA DATA CENTER MARKET, RACK SPACE UTILIZATION, VALUE IN (%), 2017 - 2029

- Figure 6:

- INDIA DATA CENTER MARKET, SMARTPHONE USERS, VOLUME IN MILLION, 2017 - 2029

- Figure 7:

- INDIA DATA CENTER MARKET, DATA TRAFFIC PER SMARTPHONE, VOLUME IN GB, 2017 - 2029

- Figure 8:

- INDIA DATA CENTER MARKET, MOBILE DATA SPEED, VOLUME IN MBPS, 2017 - 2029

- Figure 9:

- INDIA DATA CENTER MARKET, BROADBAND SPEED, VOLUME IN MBPS, 2017 - 2029

- Figure 10:

- INDIA DATA CENTER MARKET, FIBER CONNECTIVITY NETWORK, VOLUME IN KILOMETER, 2017 - 2029

- Figure 11:

- INDIA DATA CENTER MARKET, VOLUME, MW, 2017 - 2029

- Figure 12:

- INDIA DATA CENTER MARKET, BY HOTSPOT, VOLUME IN MW, 2017 - 2029

- Figure 13:

- INDIA DATA CENTER MARKET, SHARE(%), BY HOTSPOT, 2017 - 2023 - 2029

- Figure 14:

- INDIA DATA CENTER MARKET, BANGALORE, VOLUME IN MW, 2017 - 2029

- Figure 15:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, BANGALORE, VOLUME SHARE (%), 2022 - 2029

- Figure 16:

- INDIA DATA CENTER MARKET, CHENNAI, VOLUME IN MW, 2017 - 2029

- Figure 17:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, CHENNAI, VOLUME SHARE (%), 2022 - 2029

- Figure 18:

- INDIA DATA CENTER MARKET, HYDERABAD, VOLUME IN MW, 2017 - 2029

- Figure 19:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, HYDERABAD, VOLUME SHARE (%), 2022 - 2029

- Figure 20:

- INDIA DATA CENTER MARKET, MUMBAI, VOLUME IN MW, 2017 - 2029

- Figure 21:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, MUMBAI, VOLUME SHARE (%), 2022 - 2029

- Figure 22:

- INDIA DATA CENTER MARKET, NCR, VOLUME IN MW, 2017 - 2029

- Figure 23:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, NCR, VOLUME SHARE (%), 2022 - 2029

- Figure 24:

- INDIA DATA CENTER MARKET, PUNE, VOLUME IN MW, 2017 - 2029

- Figure 25:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, PUNE, VOLUME SHARE (%), 2022 - 2029

- Figure 26:

- INDIA DATA CENTER MARKET, REST OF INDIA, VOLUME IN MW, 2017 - 2029

- Figure 27:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, REST OF INDIA, VOLUME SHARE (%), 2022 - 2029

- Figure 28:

- INDIA DATA CENTER MARKET, BY DATA CENTER SIZE, VOLUME IN MW, 2017 - 2029

- Figure 29:

- INDIA DATA CENTER MARKET, SHARE(%), BY DATA CENTER SIZE, 2017 - 2023 - 2029

- Figure 30:

- INDIA DATA CENTER MARKET, LARGE, VOLUME IN MW, 2017 - 2029

- Figure 31:

- INDIA DATA CENTER MARKET, MASSIVE, VOLUME IN MW, 2017 - 2029

- Figure 32:

- INDIA DATA CENTER MARKET, MEDIUM, VOLUME IN MW, 2017 - 2029

- Figure 33:

- INDIA DATA CENTER MARKET, MEGA, VOLUME IN MW, 2017 - 2029

- Figure 34:

- INDIA DATA CENTER MARKET, SMALL, VOLUME IN MW, 2017 - 2029

- Figure 35:

- INDIA DATA CENTER MARKET, BY TIER TYPE, VOLUME IN MW, 2017 - 2029

- Figure 36:

- INDIA DATA CENTER MARKET, SHARE(%), BY TIER TYPE, 2017 - 2023 - 2029

- Figure 37:

- INDIA DATA CENTER MARKET, TIER 1 AND 2, VOLUME IN MW, 2017 - 2029

- Figure 38:

- INDIA DATA CENTER MARKET, TIER 3, VOLUME IN MW, 2017 - 2029

- Figure 39:

- INDIA DATA CENTER MARKET, TIER 4, VOLUME IN MW, 2017 - 2029

- Figure 40:

- INDIA DATA CENTER MARKET, BY ABSORPTION, VOLUME IN MW, 2017 - 2029

- Figure 41:

- INDIA DATA CENTER MARKET, SHARE(%), BY ABSORPTION, 2017 - 2023 - 2029

- Figure 42:

- INDIA DATA CENTER MARKET, NON-UTILIZED, VOLUME IN MW, 2017 - 2029

- Figure 43:

- INDIA DATA CENTER MARKET, BY COLOCATION TYPE, VOLUME IN MW, 2017 - 2029

- Figure 44:

- INDIA DATA CENTER MARKET, SHARE(%), BY COLOCATION TYPE, 2017 - 2023 - 2029

- Figure 45:

- INDIA DATA CENTER MARKET, HYPERSCALE, VOLUME IN MW, 2017 - 2029

- Figure 46:

- INDIA DATA CENTER MARKET, RETAIL, VOLUME IN MW, 2017 - 2029

- Figure 47:

- INDIA DATA CENTER MARKET, WHOLESALE, VOLUME IN MW, 2017 - 2029

- Figure 48:

- INDIA DATA CENTER MARKET, BY END USER, VOLUME IN MW, 2017 - 2029

- Figure 49:

- INDIA DATA CENTER MARKET, SHARE(%), BY END USER, 2017 - 2023 - 2029

- Figure 50:

- INDIA DATA CENTER MARKET, BFSI, VOLUME IN MW, 2017 - 2029

- Figure 51:

- INDIA DATA CENTER MARKET, CLOUD, VOLUME IN MW, 2017 - 2029

- Figure 52:

- INDIA DATA CENTER MARKET, E-COMMERCE, VOLUME IN MW, 2017 - 2029

- Figure 53:

- INDIA DATA CENTER MARKET, GOVERNMENT, VOLUME IN MW, 2017 - 2029

- Figure 54:

- INDIA DATA CENTER MARKET, MANUFACTURING, VOLUME IN MW, 2017 - 2029

- Figure 55:

- INDIA DATA CENTER MARKET, MEDIA & ENTERTAINMENT, VOLUME IN MW, 2017 - 2029

- Figure 56:

- INDIA DATA CENTER MARKET, TELECOM, VOLUME IN MW, 2017 - 2029

- Figure 57:

- INDIA DATA CENTER MARKET, OTHER END USER, VOLUME IN MW, 2017 - 2029

- Figure 58:

- INDIA DATA CENTER MARKET, BY MAJOR PLAYER IT LOAD CAPACITY, 2022

India Data Center Industry Segmentation

A data center is a facility or dedicated space that houses computer systems and associated components to store, process, and disseminate data and applications. Since IT operations are crucial for business activities and continuity, they also include infrastructure for power backups, data communications connections, environmental controls, and various security devices. The study tracks the current market footprint and planned expansions within the data center industry in India.

The India Data Center Market is segmented by Type (Captive and Outsourced (Colocation and Hosting)) and IT Infrastructure Type (Servers, Storage, and Enterprise Networking). The market sizes and forecasts are provided in terms of value in USD billion for all the above segments.

| By Type | |

| Captive | |

| Outsourced (Colocation and Hosting) |

| By IT Infrastructure Type | |

| Servers | |

| Storage | |

| Enterprise Networking | |

| Other IT Infrastructure Types |

Market Definition

- IT LOAD CAPACITY - The IT load capacity or installed capacity, refers to the amount of energy consumed by servers and network equipments placed in a rack installed. It is measured in megawatt (MW).

- ABSORPTION RATE - It denotes the extend to which the data center capacity has been leased out. For instance, a 100 MW DC has leased out 75 MW, then absorption rate would be 75%. It is also referred as utilization rate and leased-out capacity.

- RAISED FLOOR SPACE - It is an elevated space build over the floor. This gap between the original floor and the elevated floor is used to accommodate wiring, cooling, and other data center equipment. This arrangement assist in having proper wiring and cooling infrastructure. It is measured in square feet (ft^2).

- DATA CENTER SIZE - Data Center Size is segmented based on the raised floor space allocated to the data center facilities. Mega DC - # of Racks must be more than 9000 or RFS (raised floor space) must be more than 225001 Sq. ft; Massive DC - # of Racks must be in between 9000 and 3001 or RFS must be in between 225000 Sq. ft and 75001 Sq. ft; Large DC - # of Racks must be in between 3000 and 801 or RFS must be in between 75000 Sq. ft and 20001 Sq. ft; Medium DC # of Racks must be in between 800 and 201 or RFS must be in between 20000 Sq. ft and 5001 Sq. ft; Small DC - # of Racks must be less than 200 or RFS must be less than 5000 Sq. ft.

- TIER TYPE - According to Uptime Institute the data centers are classified into four tiers based on the proficiencies of redundant equipment of the data center infrastructure. In this segment the data center are segmented as Tier 1,Tier 2, Tier 3 and Tier 4.

- COLOCATION TYPE - The segment is segregated into 3 categories namely Retail, Wholesale and Hyperscale Colocation service. The categorization is done based on the amount of IT load leased out to potential customers. Retail colocation service has leased capacity less than 250 kW; Wholesale colocation services has leased capacity between 251 kW and 4 MW and Hyperscale colocation services has leased capacity more than 4 MW.

- END CONSUMERS - The Data Center Market operates on a B2B basis. BFSI, Government, Cloud Operators, Media and Entertainment, E-Commerce, Telecom and Manufacturing are the major end-consumers in the market studied. The scope only includes colocation service operators catering to the increasing digitalization of the end-user industries.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms