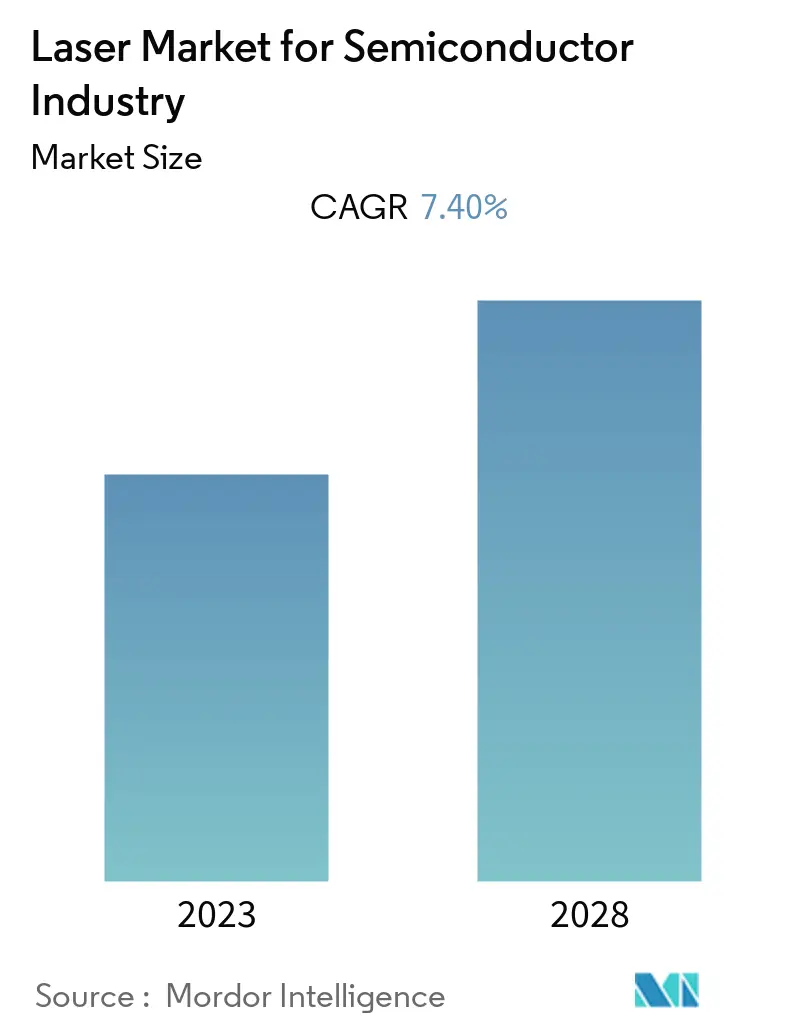

Semiconductor Industry Laser Market Size

| Study Period | 2017-2027 |

| Base Year For Estimation | 2021 |

| CAGR | 7.40 % |

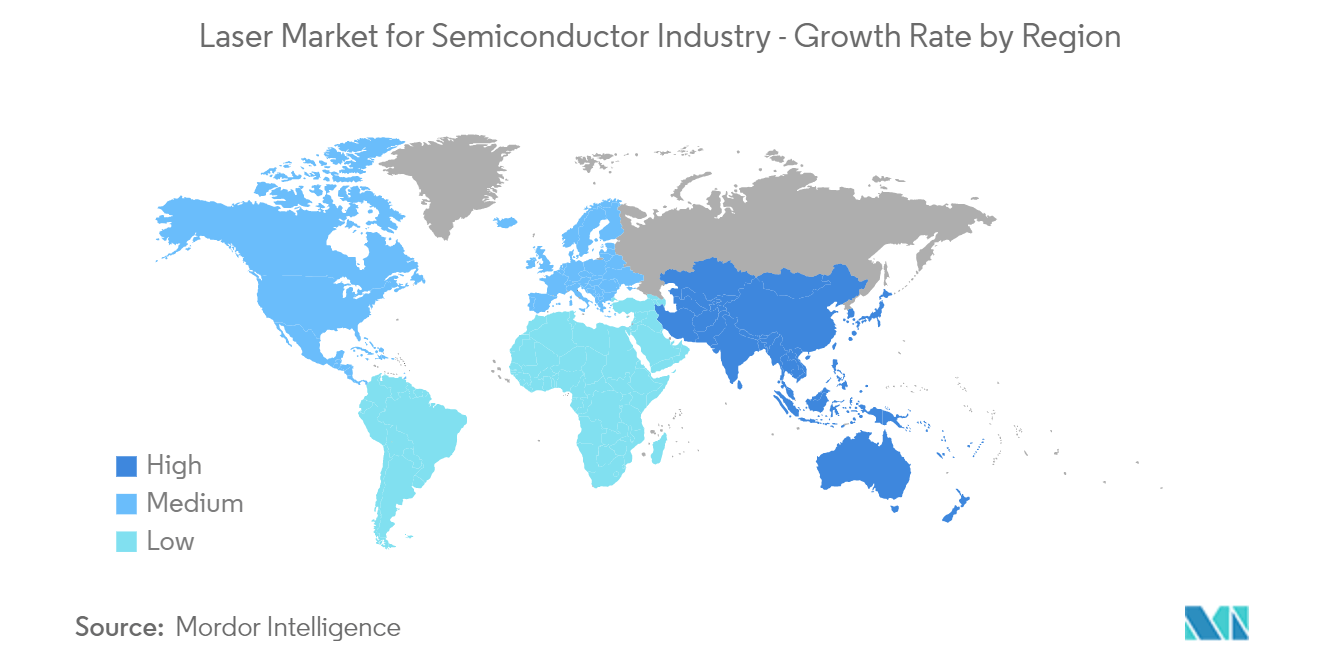

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Semiconductor Industry Laser Market Analysis

The Laser Market for Semiconductor Industry is anticipated to register a CAGR of 7.4% during the forecast period. Lasers are gaining significant traction in the semiconductor industry as they offer flexible, advanced machining to meet stringent requirements of the industry, providing semiconductor manufacturers with a highly accurate method of cutting complex shapes from various materials. Lasers allow materials to be sliced into infinite shapes and patterns with high precision. A laser system custom designed for semiconductor application can cut a wide range of materials accurately and quickly.

- The semiconductor market is witnessing several innovations owing to robust R&D activities. For instance, in November 2022, researchers from the LP3 Laboratory in France developed a direct laser writing technique to achieve local material processing within the 3D space of semiconductor chips. They claim that the dominating manufacturing technology, lithography, has substantial limitations in thoroughly addressing the challenges posed by the semiconductor manufacturing sector. For this reason, they suppose that fabricating structures under the wafer surfaces would be highly desirable to exploit the full space inside the materials. In the International Journal of Extreme Manufacturing, the researchers demonstrated such capability vis the newly developed direct laser writing technique, which facilitates fabricating embedded structures inside various semiconductor materials. Further, in June 2022, engineers at the University of California, Berkeley (Department of Electrical Engineering and Computer Sciences (EECS)) created a new type of semiconductor laser that accomplishes an elusive goal in the field of optics: the ability to maintain a single mode of emitted light while maintaining the ability to scale up in size and power. It is claimed to be a significant achievement as it means size does not have to come at the expense of coherence, enabling lasers to be more powerful and to cover longer distances for many applications.

- The studied market is witnessing an upsurge in demand owing to numerous initiatives by governments of various nations. For instance, the United States government aims to become independent in the semiconductor supply chain ecosystem. In these efforts, in December 2021, senators in the United States introduced Investing in Domestic Semiconductor Manufacturing Act in the senate. This proposed legislation would expand eligibility for CHIPS for America, a government subsidy program for the semiconductor industry, to fund financial assistance beyond entities involved in semiconductor fabrication, testing, assembly, or R&D to organizations involved with materials used to manufacture semiconductors and semiconductor manufacturing equipment. By incentivizing the companies that produce essential materials and equipment, this legislation can create more opportunities for manufacturers across the country and strengthen the supply chain that supports domestic semiconductor manufacturing

- Additionally, in September 2022, the Biden administration announced that it would invest USD 50 billion in building up the domestic semiconductor industry to counter dependency on China, as the US produces zero and consumes 25% of the world's leading-edge chips vital for its national security. President Joe Biden signed a USD 280 billion CHIPS bill in August 2022 to boost domestic high-tech manufacturing, part of his administration's push to increase US competitiveness over China. Such robust investments in the semiconductor sector in the region would offer lucrative opportunities for the growth of the studied market.

- The outbreak of COVID-19 globally has significantly disrupted the supply chain and production of the studied market in the initial phase of 2020. For circuit and chipmakers, the impact was more severe. Due to labor shortages, many packages and testing plants in the Asia-Pacific region reduced or even suspended operations. This also created a bottleneck for end-product companies that depend on semiconductors. However, many of these effects are likely to be short-term. Precautions by governments across the globe to support automotive and semiconductor sectors could help revive industry growth.

- On the Flipside, the initial calibration of lasers is a very complex task and requires a high level of expertise to achieve the high-precision tuning required for the application. Also, the huge number of parameters has to be considered while tuning the laser, and a small offset may lead to errors or be catastrophic in various applications. The manufacturing process of the lasers is very complex, due to which the manufacturing cost has also increased significantly. Another important aspect of the laser's performance when switching between wavelengths is the wavelength stability of the device. As the laser tunes into its desired wavelength, there is a settling drift before the channel finally stabilizes. Such factors might hinder the growth of the studied market.

Semiconductor Industry Laser Market Trends

This section covers the major market trends shaping the Semiconductor Industry Laser Market according to our research experts:

The Inspection & Metrology Segment is Expected to Hold a Major Market Share

- Smartphones and other applications across consumer electronics, automotive applications, etc., drive the demand for high-performance, low-cost semiconductor materials. These industries have been inspired by technology transitions, such as wireless technologies (5G), Artificial Intelligence, etc. Also, the trend of increasing Internet of Things (IoT) devices is expected to force the semiconductor industry to invest in this equipment to attain intelligent products.

- Moreover, the rising digitization and increasing trends of remote work and remote operations have sparked the need for advanced semiconductor devices that enable various new capabilities. As the demands for semiconductor devices intensify consistently, advanced packaging techniques provide the form factor and processing power required for today's digitized world. According to Semiconductor Industry Association, during August 2022, global semiconductor industry sales were USD 47.4 billion, a slight increase of 0.1% over the August 2021 total of USD 47.3 billion. Such an increase in the demand for semiconductors is anticipated to offer lucrative opportunities for the inspection and metrology equipment market growth.

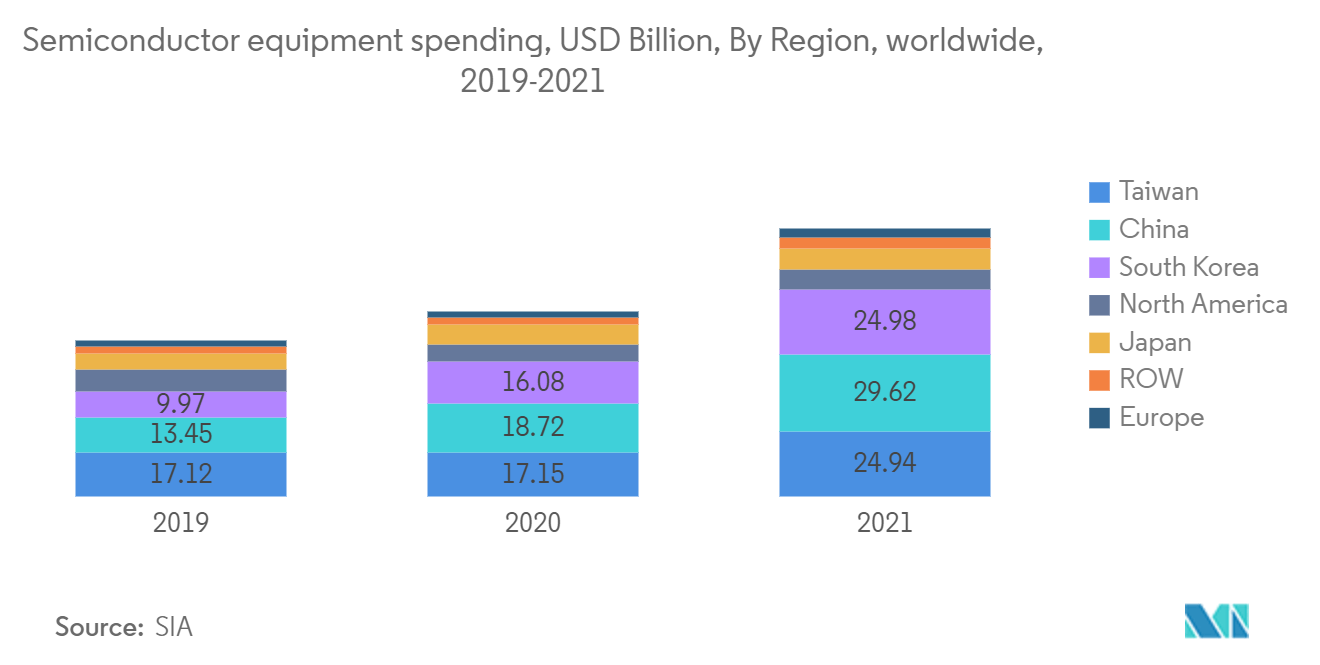

- Capacity expansions in the semiconductor industry are also aiding the growth of the studied market. For instance, according to SEMI Equipment Market Data Subscription (EMDS), the semiconductor industry's foot in 2021 was firmly on the accelerator. Capacity increases aided the expansion of both the front-end and back-end semiconductor equipment industries to meet growth drivers.

- Billings for semiconductor equipment in the United States increased by 44% yearly to USD 102 billion, surpassing the previous high established in 2020. Advanced logic and foundry capacity expansions, DRAM investment recovery, and robust NAND Flash spending drove equipment market growth. Equipment spending was high across the board in 2021, marking the first time the top three areas — China, Korea, and Taiwan – collectively spent more than USD 20 billion on capital equipment annually.

- Several companies are innovating new products to cater to the rise in demand for semiconductors and satisfy the complex requirements of consumers. For instance, in December 2021, Park Systems, a company that manufactures atomic force microscopes, created a tool for inspecting masks used in the wafer fabrication process's extreme ultraviolet (EUV) step. The equipment may check the cover for flaws and improvements without endangering it. The EUV laser can create even more precise circuit patterns on the wafer since its wavelength is fourteen times smaller than that of argon fluoride (ArF) lasers. As a result, the process's mask needs to be more precise and finely tuned. It can be expensive to have covers destroyed by dust when used in EUV processes.

The Asia Pacific Region is Expected to Witness a High Market Growth

- The Asia-Pacific is one of the prominent regions for the semiconductor industry's manufacturing and consumption. According to Semiconductor Equipment and Materials International, spending on semiconductor equipment in China reached USD 29.62 billion in 2021. Moreover, in South Korea, spending amounted to USD 24.98 billion in 2021, while in Taiwan, it stood at USD 24.94 billion. The expenditure has increased yearly, which will drive the studied market.

- The region also boasts several initiatives by governments to boost the semiconductor industry. For instance, China's State Council's ‘2014 "National Integrated Circuit Industry Development Guidelines" aims to become a global leader in all semiconductor industry segments by 2030. Additionally, the Made in China 2025 initiative maintains achieving knowledge about advanced semiconductor manufacturing as a vital component of China's future economy and society. It is highly focused on the strategy to build a strong manufacturing nation across the world. The initiative is expected to encourage local and foreign companies to invest in the Chinese market across various segments, including integrated circuits. The initiative also prompts the government bodies to boost research and development activities so that China can rely on its own companies for core technologies rather than overseas ones. This propels innovation in the semiconductor manufacturing industry, thereby driving the laser market.

- Further, in December 2021, the Ministry of Electronics and Information Technology (MeitY) approved a comprehensive PLI scheme for developing semiconductor and display manufacturing ecosystems. Incentives worth INR 76,000 crore (USD 9.81 billion) were announced and will be distributed over the next six years. Such initiatives in the region are expected to drive the studied market.

- Semiconductors remain the backbone material of electronics integrated with modern devices like cars, smartphones, robots, and many other intelligent devices. Driven by the continuous need for miniaturized and powerful chips, current semiconductor manufacturing technologies face increasing pressure. Japan's electronic products industry, one of the largest in the world, is one of the most significant factors driving demand for semiconductors packaging in the region. As per the Japan Electronics and Information Technology Industries Association (JEITA), in 2021, the production value of electronic devices in Japan grew by 10.6% compared to the previous year, reaching a value of about JPY 3.94 trillion (~USD 28.5 Billion) in 2021. The increase in demand for electronics and intelligent devices in the region will likely offer lucrative opportunities for the growth of the studied market.

- As the demand for semiconductors has increased significantly in the Asia Pacific region in recent years, and as prominent semiconductor customers in several countries are strengthening their supply chains, investment in the semiconductor industry is further accelerated. For instance, in July 2022, GigaphotonInc., a manufacturer of light sources used in semiconductor lithography, announced that it would increase its production capacity by 2.5 times by constructing a new building in Japan. The company invested around JPY 5 billion (USD 36.2 million) in the construction of the new facility expected to be completed by June 2023. Such investments would boost the semiconductor industry's expansion of the laser market.

Semiconductor Industry Laser Industry Overview

The Laser Market for Semiconductor Industry is a moderately competitive market with significant players like Lumentum Operations, Trumpf, SUSS MicroTec, Coherent, etc. The market players are striving to innovate advanced products and processes to cater to the evolving demands of their customers.

- April 2022 - MKS Instruments, Inc. launched its Spectra-Physics IceFyre GR50 laser, a compact, high-power green picosecond laser with efficient performance and low cost of ownership. The new laser delivers ultrashort pulses, >50 W green power, and versatility for process optimization with adjustable repetition rates, TimeShift ps programmable pulse flexibility, and pulse-on-demand triggering. The laser is rugged and compact, enabling easy integration into machine tools. The laser is intended for challenging micromachining materials like FR4, various metals, ceramics, and glass composites while operating in demanding, 24/7 manufacturing environments.

- February 2022 - Gigaphoton Inc., a prominent manufacturer of light sources utilized in semiconductor lithography, announced that its KrFexcimer laser ‘G300K’ for processing applications had been chosen for usage in a project led by the National Applied Research Laboratories in Taiwan and sold to National Cheng Kung University. Gigaphoton’s KrF laser ‘G300K’, developed under the concept of ‘optimizing processing’ for micro ablation, was adopted as it was considered the most suitable excimer laser for carrying out the research.

Semiconductor Industry Laser Market Leaders

Coherent, Inc.

Accretech

SUSS MicroTec

Lumentum Operations LLC

Hamamatsu Photonics K.K.

*Disclaimer: Major Players sorted in no particular order

Semiconductor Industry Laser Market News

- August 2022 - Coherent Inc. unveiled its commercial solid-state 460nm blue laser. Sharing a twin product platform as Coherent's prior sapphire products, the sapphire 460-10 is the company's third in a series of products incorporating its OPSL (optically pumped semiconductor laser) technology. In conventional Vertical Cavity Surface, Emitting Lasers emission is driven by electrical current. OPSL technology utilizes optical (photon) energy to go laser emission. Optical pumping allows higher power than that achieved with electrical pumping.

- November 2022 - 3D-Micromac AG, a prominent laser micromachining and roll-to-roll laser systems company for the semiconductor, photovoltaic, glass, and display markets, announced that a significant optical solutions provider purchased multiple microMIRA Laser Lift-Off (LLO) systems from 3D-Micromac for usage in the production of microLED devices. The customer would install the new microMIRA systems in the pilot- and production lines at its advanced LED chip factory in Asia.

Semiconductor Industry Laser Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Impact of COVID-19 on the Market

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Technology Snapshot

5. MARKET DYNAMICS

5.1 Market Drivers

5.2 Market Restraints

6. MARKET SEGMENTATION

6.1 By Laser Type

6.1.1 Nanosecond

6.1.2 Picosecond

6.1.3 CO2

6.1.4 Others (Femtosecond and Excimer)

6.2 By Process Step

6.2.1 Removal Process

6.2.2 Bonding Process

6.2.3 Inspection & Metrology

6.2.4 Reforming Process

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia Pacific

6.3.4 Rest of the World

7. COMPETITIVE LANDSCAPE

7.1 Laser Equipment Suppliers Analysis

7.1.1 Accretech

7.1.2 Disco Corporation

7.1.3 Coherent, Inc.

7.1.4 IPG Photonics Corporation

7.1.5 Veeco Instruments Inc.

7.1.6 EVG Group

7.1.7 SUSS MicroTec

7.1.8 Orbotech/SPTS

7.1.9 HGTech

7.1.10 QMC

7.1.11 Screen Semiconductor Solutions Co., Ltd.

7.1.12 Nikon

7.2 Laser Source Suppliers Analysis

7.2.1 Micromac

7.2.2 Lumentum Operations LLC

7.2.3 Trumpf

7.2.4 HANS Laser

7.2.5 Amplitude Laser

7.2.6 IPG

7.2.7 Hamamatsu

7.2.8 Ushio

7.2.9 Jenoptik

7.2.10 EO Technics

7.2.11 HGTech

7.2.12 Edgewave

7.2.13 MKS

8. VENDOR RANKING ANALYSIS OF LASER EQUIPMENT SUPPLIERS

9. FUTURE OUTLOOK OF THE MARKET

Semiconductor Industry Laser Industry Segmentation

A laser is a device or source that stimulates atoms or molecules to emit light at particular wavelengths and amplifies that light, typically producing a very narrow beam of radiation.

The Laser Market for Semiconductor Industry is Segmented by Laser Type (Nanosecond, Picosecond, CO2) and By Process Steps (Removal Process, Bonding Process, Inspection & Metrology, Reforming Process) and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

The studies track the revenue accrued by laser equipment manufacturing various semiconductor components across different geographical locations. Revenues from Service, maintenance, installation, etc., are not considered in the study. The study also analyzes the scope of laser technologies across different manufacturing process steps.

| By Laser Type | |

| Nanosecond | |

| Picosecond | |

| CO2 | |

| Others (Femtosecond and Excimer) |

| By Process Step | |

| Removal Process | |

| Bonding Process | |

| Inspection & Metrology | |

| Reforming Process |

| By Geography | |

| North America | |

| Europe | |

| Asia Pacific | |

| Rest of the World |

Semiconductor Industry Laser Market Research FAQs

What is the current Laser Market for Semiconductor Industry size?

The Laser Market for Semiconductor Industry is projected to register a CAGR of 7.4% during the forecast period (2023-2027).

Who are the key players in Laser Market for Semiconductor Industry?

Coherent, Inc., Accretech, SUSS MicroTec, Lumentum Operations LLC and Hamamatsu Photonics K.K. are the major companies operating in the Laser Market for Semiconductor Industry.

Which is the fastest growing region in Laser Market for Semiconductor Industry?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2027).

Which region has the biggest share in Laser Market for Semiconductor Industry?

In 2023, the North America accounts for the largest market share in the Laser Market for Semiconductor Industry.

Laser for Semiconductor Industry Industry Report

Statistics for the 2023 Laser for Semiconductor Industry market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Laser for Semiconductor Industry analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.