Logistics Automation Market Size

| Study Period | 2018 - 2028 |

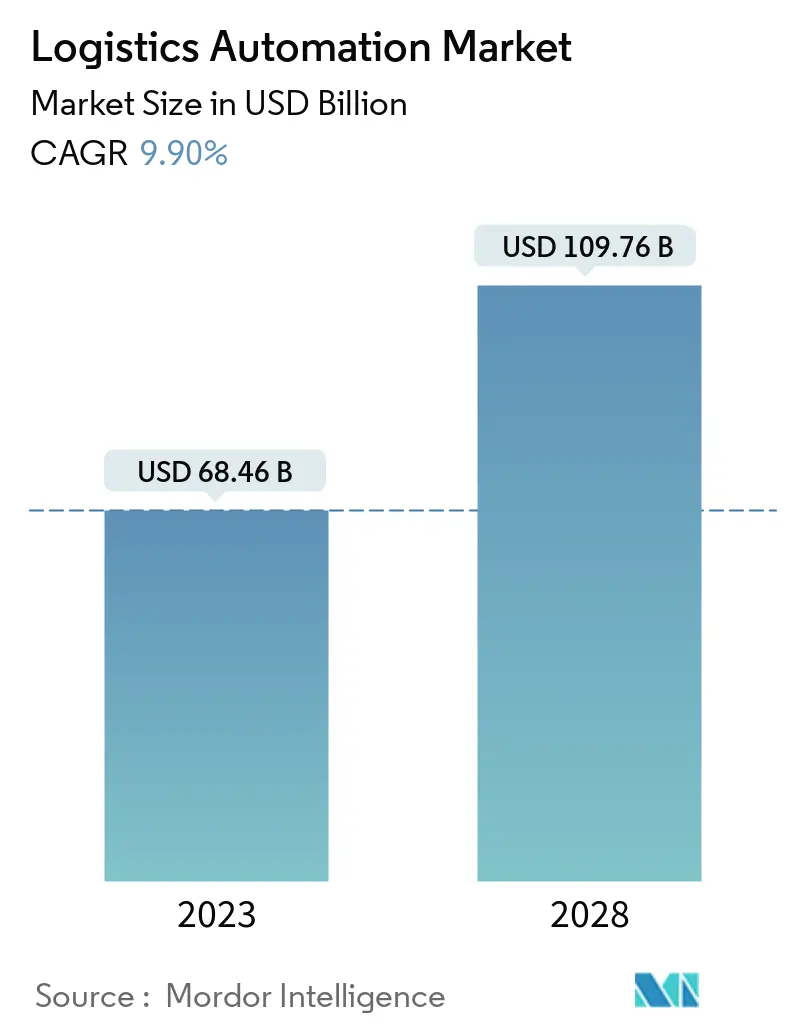

| Market Size (2023) | USD 68.46 Billion |

| Market Size (2028) | USD 109.76 Billion |

| CAGR (2023 - 2028) | 9.90 % |

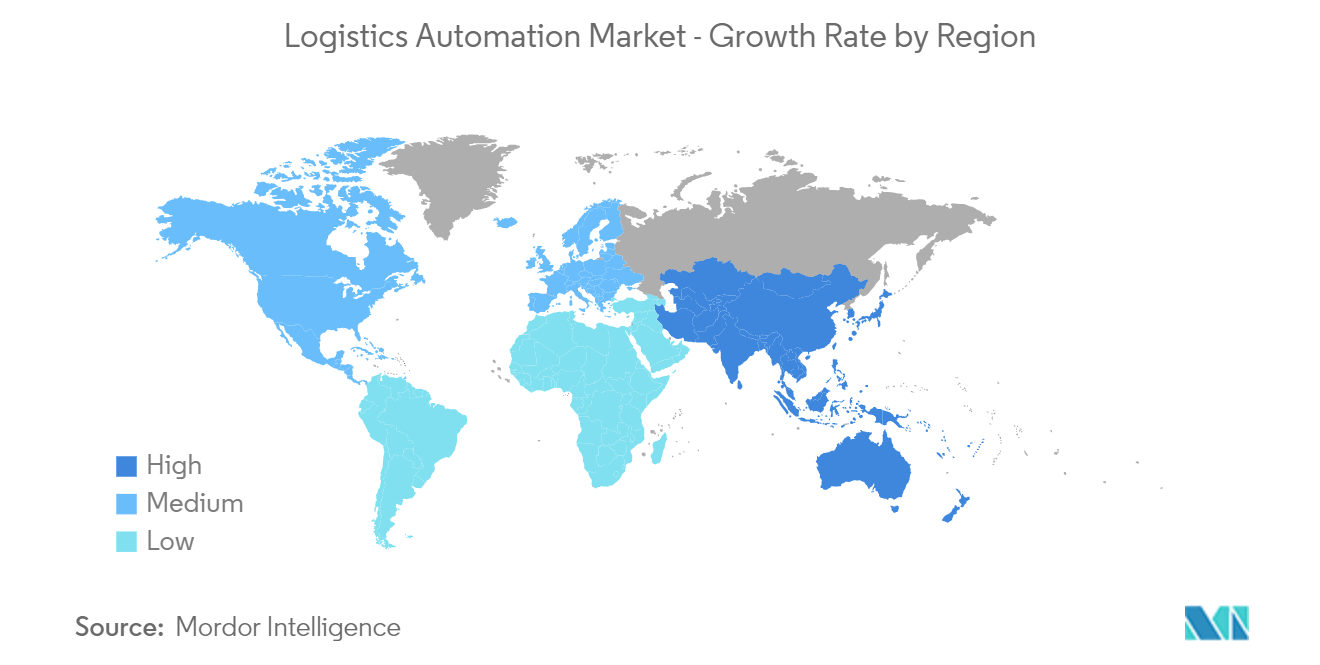

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Logistics Automation Market Analysis

The Logistics Automation Market size is estimated at USD 68.46 billion in 2023, and is expected to reach USD 109.76 billion by 2028, growing at a CAGR of 9.90% during the forecast period (2023-2028).

Automation in logistics is called the use of machinery, control systems, and software to enhance the efficiency of operations. It usually applies to the processes performed in a warehouse or distribution center, which requires minimal human intervention. Some of the benefits of automation logistics include improved customer service, scalability and speed, organizational control, and reduction of mistakes.

- The growth in the e-commerce industry and the need for efficient warehousing and inventory management worldwide are driving the market. For instance, The U.S. retail e-commerce sales for the second quarter of 2022 were USD 257.3 billion, up 2.7% from the first quarter of 2022, according to the Census Bureau of the Department of Commerce. Moreover, according to IBEF, the Indian e-commerce market is expected to flourish from USD 38.5 billion in 2017 to USD 200 billion by 2026.

- Automation for warehouses offers superior convenience regarding cost-cutting for the overall business and helps minimize minute errors in product deliveries. According to Dalsey, Hillblom, and Lynn, a prominent 3PL company and a significant end-user of warehouse automation solutions, about 80% of warehouses "still ma "usually operate with no supporting automation" despite "the advantages. Furthermore, warehouses that use sorters, conveyors, and pick and place solutions, among other equipment (not necessarily automated), account for 15% of the total warehouses. In contrast, only 5% of the current warehouses are automated.

- According to the Bank of America, by 2025, 45% of all manufacturing is likely to be performed by robotic technology. Following this trend, large firms, such as Raymond Limited (an Indian textile major) and Foxconn Technology (a China-based supplier for large technology manufacturers like Samsung), have replaced (or plan to replace) 10,000 and 60,000 workers, respectively, by incorporating automated technology into their factories. These factors have directly impacted the increasing adoption of warehouse robotics.

- With high upfront costs, the long duration to achieve an ROI has been limiting the mass adoption of automation solutions. Developing economies such as China and India have been representative of labor-intensive formats. With low costs , an investment of a million dollars for a single system with additional staff training has been restraining the same. The issues pertaining to cost and return on investment (ROI) also affect the investments from multiple small and medium-sized businesses (SMBs). These have been slow to adopt robotics, as per Nancey Green Leigh, who is a Georgia Tech professor at a National Science Foundation-funded project called "Workers, Firms, and Industries in Robotics.

- The COVID-19 pandemic led warehouse operators to consider accelerating their timelines to adopt automation and robotics. Those who have successfully deployed also depicted the creation of safer workplaces by reducing interactions among workers by simultaneously enhancing productivity to meet increasing demands for e-commerce.

Logistics Automation Market Trends

Mobile Robots (AGV and AMR) are Expected to Witness Significant Growth

- The primary usage of logistics robots is the use of mobile AGVs (automated guided vehicles) in warehouses and storage facilities to transport goods. These robots operate in predefined pathways by moving products for shipping and storage. AGVs play an essential role in decreasing the cost of logistics and streamlining the supply chain.

- AGVs are also used for replenishment and picking for inbound and outbound handling. For example, AGVs transport inventory from receiving to storage locations or long-term storage locations to forward-picking locations to replenish stock. Moving inventory from long-term storage to forward-picking locations ensures adequate inventory is accessible to pickers, making the order-picking process more efficient.

- The vendors in the studied market are constantly innovating and launching new AGVs and AMRs for the warehouse segment of operations, including logistics. For instance, in April 2021, JBT unveiled its warehouse freezer AGV, which may operate at various temperatures, from -10 oF to 110 oF, offering operations a lift capacity of 2,500 pounds. The automatic guided vehicle (AGV) features a triple-stage hydraulic mast with an integrated side shift and tilt. In addition, it provides a variety of lift heights, from 357 inches (or less) to the top of its forks to 422 inches.

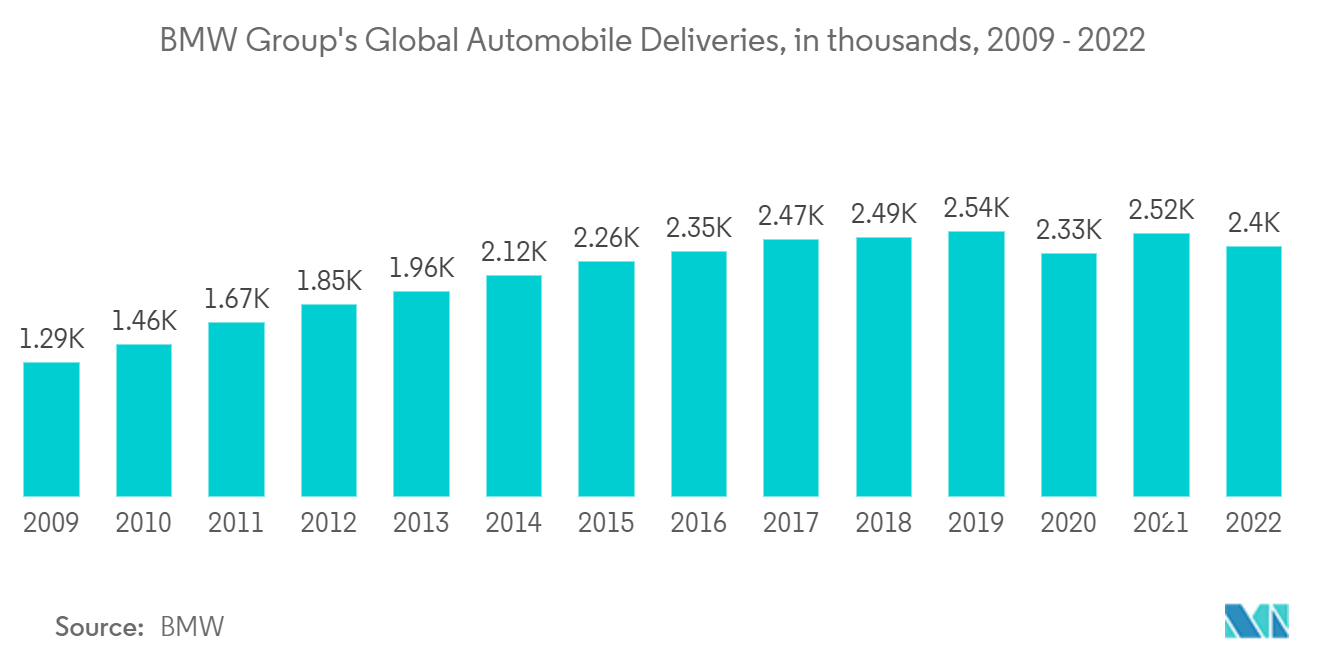

- Further, the automakers are increasing their production and shipment units, indicating the usage of AGVs and AMRs. For instance, according to BMW, in 2022, the Bayerische Motoren Werke AG (BMW) shipped over 2.5 million autos worldwide, including brands BMW, MINI, and Rolls-Royce vehicles, to customers worldwide, a year in which all industries faced headwinds from supply bottlenecks, China's pandemic lockdowns, and others.

- In March 2022, autonomous mobile robot (AMR) provider Locus Robotics extended its line of warehouse AMRs with the Locus Vector and Locus Max. Locus Vector is a compact AMR with omnidirectional mobility and robust payload capacity. The Locus Max AMR has a heavyweight load capacity and improved flexibility for industrial and material handling applications. The LocusBots can be added to existing and new workflows, enabling operations to scale and adapt to changing market demands.

Asia Pacific is Expected to Register the Largest Market

- The Asia-Pacific warehouse automation market is rapidly expanding due to the region's growing number of industries and their integration with automation to increase ROI. With the increasing adoption of robots, the expansion of e-commerce, and the construction of new warehouses, the Asia-Pacific warehouse automation market is expected to dominate.

- China, one of the biggest economies in the world, is a significant supplier of warehouse robots in the Asia-Pacific region, particularly in the automotive, manufacturing, and e-commerce sectors. The market is growing as a result of this. China achieved a robot density of 322 units per 10,000 workers in the manufacturing industry, according to the most recent statistical yearbook, "World Robotics," by IFR, and the nation was ranked 5th globally in 2021.

- In Japan, the "New Robot Strategy" aims to establish the country as the leading hub for robotic innovation. The Japanese government already contributed more than USD 930.5 million in 2022 (according to IFR). The manufacturing and service action plan includes initiatives like autonomous driving, advanced air mobility, and the creation of integrated technologies that are anticipated to form the basis of the next generation of robots and artificial intelligence. Additionally, according to IFR, a budget of USD 440 million was given to robotics-related projects in the "Moonshot Research and Development Program" for five years from 2020 to 2025.

- The robust e-commerce sector in India is also significantly boosting the market's growth. According to the India Brand Equity Foundation (IBEF), India's e-commerce market is expected to reach USD 111 billion by 2024 and USD 200 billion by 2026. After China and the United States, India had the third-largest online shopper base of 140 million in 2020. An increase in smartphone and internet usage is a major factor in the industry's growth. The Digital India program significantly increased the number of internet connections in 2021, reaching 830 million. Several government policies helped accelerate this growth. The Government of India allowed 100% FDI (foreign direct investment) in B2B e-commerce. Moreover, 100% FDI is permitted under the automatic route in the marketplace model of e-commerce.

- For instance, e-commerce giant Amazon, which invested USD 5 billion in the Indian market, is investing in automated warehouses across India. Amazon is among the first few companies in India that have experimented with and adopted robotics in their warehouses. Its Kiva robot engages in the picking and packing process at large warehouses. Further, in June 2022, Amazon announced its first autonomous mobile robot aimed at reducing warehouse workers' workload. The autonomous robot named Porteus moves through the Amazon facilities using advanced safety, perception, and navigation technology developed by Amazon. Furthermore, with the growing investment in the FMCG sector in India, the demand for the warehouse automation market is increasing.

Logistics Automation Industry Overview

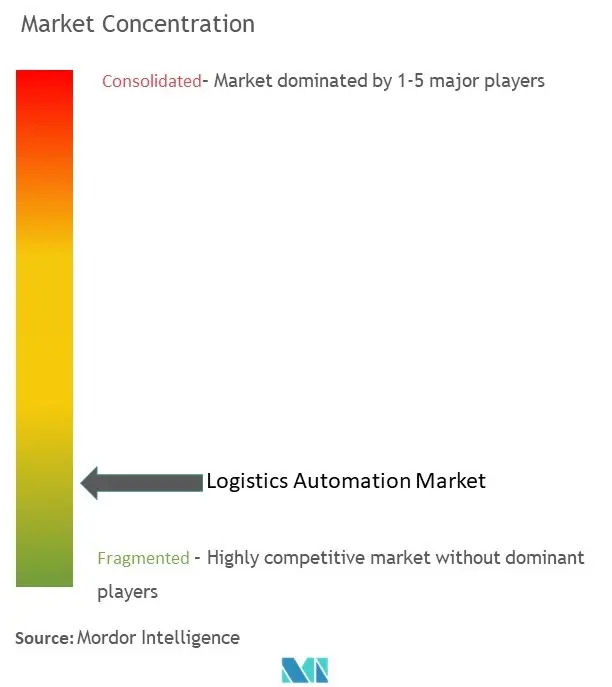

The logistics automation market comprises several global players vying for attention in a fairly contested market space. The market comprises long-standing established players, including Honeywell, Swisslog, Daifuku, and Schaefer. These players have made significant investments in products and manufacturing plants. Although the new market players require moderate investments, they can sustain themselves only through powerful competitive strategies.

Additionally, product innovations can also work in favor of new players, as they can target emerging and less explored application areas to expand their market presence further. As the market poses moderate barriers to entry for new players, several new entrants backed by VCs have been able to gain traction in the market, intensifying the market competition.

In March 2023, Dematic provided the most recent automation technologies for KION's new logistics facility. The KION Group is likely to utilize the facility to ship replacement components around Europe. The aim is to make customer deliveries more effective. Dematic plans to deploy a highly dynamic Dematic Multishuttle with 110,000 storage places and 150 shuttles for automatic storage and retrieval.

In March 2023, Swisslog's CarryPickmobile robotic goods-to-person storage and retrieval system was released. The new, updated CarryPickmobile robotic platform offers a much faster working speed. The mobile robots also employ a revolutionary lifting turntable that allows them to turn a rack or hold the rack stationary as it turns, enabling quicker and more adaptable storage and selection processes for goods-to-person solutions.

Logistics Automation Market Leaders

Dematic Group (Kion Group AG)

Daifuku Co. Limited

Swisslog Holding AG (KUKA AG)

Honeywell International Inc.

Jungheinrich AG

*Disclaimer: Major Players sorted in no particular order

Logistics Automation Market News

- April 2023 : TGW Logistics Group announced to offer of new and existing customer innovative visualization dashboards for optimizing the performance of the intralogistics system. With the help of this dashboard, data from many different software sources can be combined, analyzed, and processed graphically: from goods-in monitoring to the warehouse area to the sorters and scanners.

- March 2023 : KNAPP AG developed innovative robotics for automation and digitalization at the LogiMAT 2023 trade fair. Its robot solutions is expected to help lower costs in logistics processes while increasing shipping capacity. The company calls this new, future-proof approach zero-touch fulfillment.

Logistics Automation Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products and Services

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Exponential Growth of the E-commerce Industry and Customer Expectation

5.1.2 Increasing Manufacturing Complexity and Technology Availability

5.1.3 Improved Efficiency and Workforce Safety

5.2 Market Challenges

5.2.1 High Capital Investment

6. MARKET SEGMENTATION

6.1 Warehouse Automation Market

6.1.1 By Component

6.1.1.1 Hardware

6.1.1.1.1 Mobile Robots (AGV, AMR)

6.1.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

6.1.1.1.3 Automated Sorting Systems

6.1.1.1.4 De-palletizing/Palletizing Systems

6.1.1.1.5 Conveyor Systems

6.1.1.1.6 Automatic Identification and Data Collection (AIDC)

6.1.1.1.7 Order Picking

6.1.1.2 Software

6.1.1.3 Services

6.1.2 By End-user Industry

6.1.2.1 Food and Beverage

6.1.2.2 Post and Parcel

6.1.2.3 Groceries

6.1.2.4 General Merchandise

6.1.2.5 Apparel

6.1.2.6 Manufacturing

6.1.2.7 Other End-user Industries

6.1.3 By Geography

6.1.3.1 North America

6.1.3.2 Europe

6.1.3.3 Asia Pacific

6.1.3.4 Latin America

6.1.3.5 Middle East and Africa

6.2 Global Transportation Automation Market Scenario

6.3 Other Global Transportation Automation Market Scenarios

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Dematic Corp. (Kion Group AG)

7.1.2 Daifuku Co. Limited

7.1.3 Swisslog Holding AG (KUKA AG)

7.1.4 Honeywell International Inc.

7.1.5 Jungheinrich AG

7.1.6 Murata Machinery Ltd

7.1.7 Knapp AG

7.1.8 TGW Logistics Group GmbH

7.1.9 Kardex Group

7.1.10 Mecalux SA

7.1.11 Beumer Group GmbH & Co. KG

7.1.12 SSI Schaefer AG

7.1.13 Vanderlande Industries BV

7.1.14 WITRON Logistik

7.1.15 Oracle Corporation

7.1.16 One Network Enterprises Inc.

7.1.17 SAP SE

- *List Not Exhaustive

7.2 Vendor Market Share Analysis

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE GROWTH

Logistics Automation Industry Segmentation

Logistics automation is the use of technology like machinery and logistics software to enhance the efficiency of logistical processes from procurement to production, inventory management, distribution, customer service, and recovery.

The market study divides the market into warehouse automation, transportation automation, and other types. The market size was analyzed by estimating the individual markets for these types. Further, the warehouse automation market is studied on the basis of components, end-users, and geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa). Based on components, the warehouse automation market was classified into hardware, software, and services. The hardware segment comprises mobile robots (AGV, AMR), automated storage and retrieval systems (AS/RS), automated sorting systems, de-palletizing and palletizing systems, conveyor systems, automatic identification and data collection (AIDC), and order picking, while the software segment comprises warehouse management systems and warehouse execution systems.

The study also tracks the market analysis across several end-user industries like food and beverage, post and parcel, groceries, general merchandise, apparel, manufacturing, and others. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry across several regions like North America, Asia Pacific, Europe, the Middle East and Africa, and Latin America. This supports the market estimations and growth rates over the forecast period. The study further analyzes the overall impact of COVID-19 on the ecosystem. The market sizes and forecasts are provided in terms of value in USD billion for all the segments.

| Warehouse Automation Market | |||||||||||||

| |||||||||||||

| |||||||||||||

|

Logistics Automation Market Research FAQs

How big is the Logistics Automation Market?

The Logistics Automation Market size is expected to reach USD 68.46 billion in 2023 and grow at a CAGR of 9.90% to reach USD 109.76 billion by 2028.

What is the current Logistics Automation Market size?

In 2023, the Logistics Automation Market size is expected to reach USD 68.46 billion.

Who are the key players in Logistics Automation Market?

Dematic Group (Kion Group AG), Daifuku Co. Limited, Swisslog Holding AG (KUKA AG), Honeywell International Inc. and Jungheinrich AG are the major companies operating in the Logistics Automation Market.

Which is the fastest growing region in Logistics Automation Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Logistics Automation Market?

In 2023, the Asia Pacific accounts for the largest market share in the Logistics Automation Market.

Logistics Automation Industry Report

Statistics for the 2023 Logistics Automation market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Logistics Automation analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.