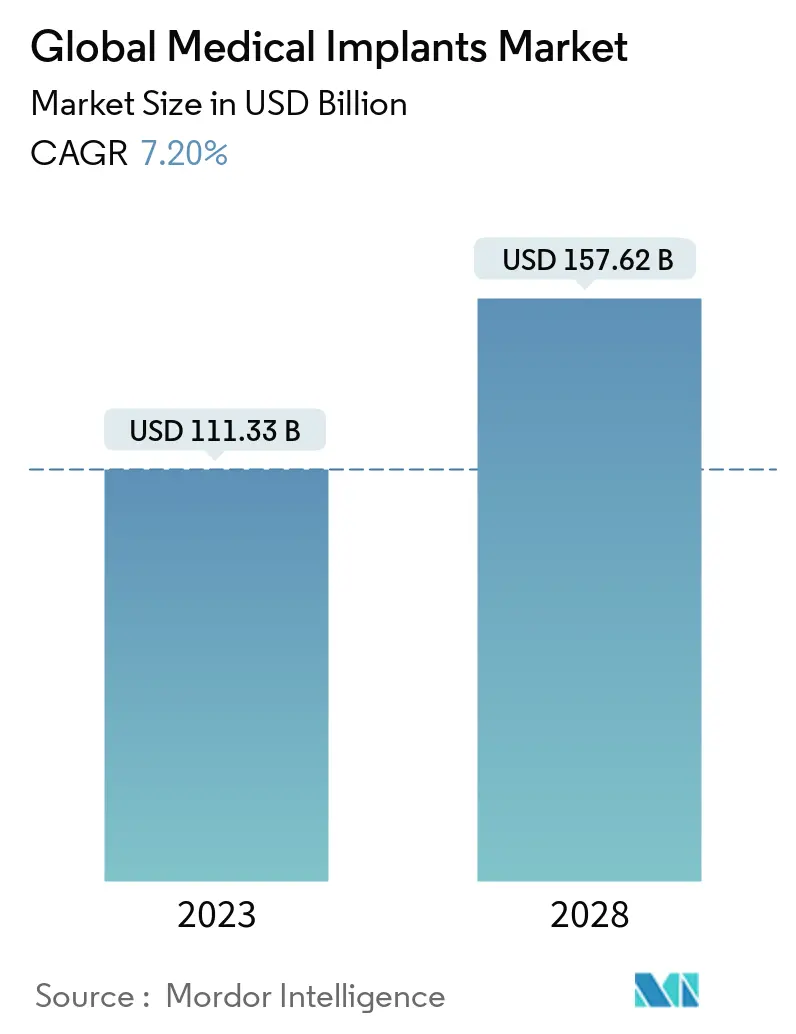

Medical Implants Market Size

| Study Period | 2018 - 2028 |

| Market Size (2023) | USD 111.33 Billion |

| Market Size (2028) | USD 157.62 Billion |

| CAGR (2023 - 2028) | 7.20 % |

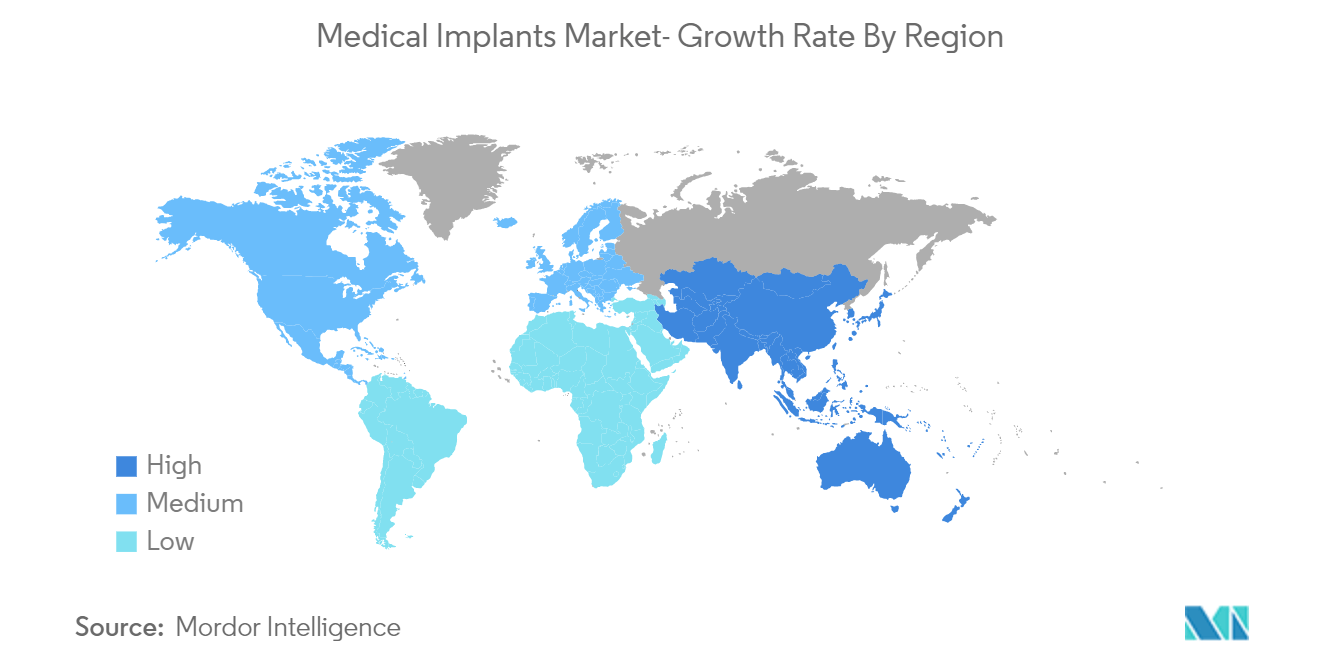

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Medical Implants Market Analysis

The Global Medical Implants Market size is expected to grow from USD 111.33 billion in 2023 to USD 157.62 billion by 2028, at a CAGR of 7.20% during the forecast period (2023-2028).

COVID-19 had significantly impacted the medical implants market's growth initially due to supply chain restrictions and the reduced number of hospital visits by patients. For instance, according to the study published in Patient Safety, titled "The Impact of COVID-19 on Medical Device Reporting and Investigation" in September 2021, constraints on person-to-person contact limited the sort of treatment patients may receive, and the pandemic made researching medical implants more challenging. Such studies suggest that COVID-19 has significantly impacted the growth of the market.

The major factors contributing to the growth of the medical implants market are the increasing geriatric population, the burden of chronic diseases, increasing demand for cosmetic dentistry, and technological advancements in medical implants.

The global population is aging rapidly, so with increasing age, the burden of orthopedic and cardiovascular diseases is increasing, which creates a need for medical implants and thus drives the growth of the market. For instance, in October 2021, according to the World Health Organization (WHO), the world's population aged 60 and above will reach a share of 22% of the total world population in 2050. Furthermore, according to the same source, by 2050, 80% of the world's elderly will live in low and middle-income countries. This increase in the number of older adults is found to augment the number of disorders, which subsequently helps boost the demand for medical implants across the globe.

Furthermore, the rise in aesthetic surgeries is also expected to drive the growth of the medical implants market over the forecast period. For instance, according to the report published by the International Society of Aesthetic Plastic Surgery in 2020, breast augmentation was among the top aesthetic surgical procedures in 2020, with 1,624,281 surgeries. Moreover, according to a March 2020 update by the World Health Organization (WHO), it is estimated that oral diseases affect nearly 3.5 billion people worldwide, and severe periodontal (gum) disease, which may result in tooth loss, is also very common, with almost 10% of the global population affected. Thus, the increasing incidence of aesthetic surgeries is driving the need for breast and dental implants, thereby driving the market growth. A few other factors are playing pivotal roles in accelerating the medical implants market include the hike in disposable income among people, technological advancements in the field of implants, the availability of better medical facilities, and a growing number of cases involving damaged limbs or organs caused by various accidents.

However, the high cost of medical implants and stringent regulatory policies are expected to restrain the market for the forecast period.

Medical Implants Market Trends

This section covers the major market trends shaping the Medical Implants Market according to our research experts:

Orthopedic Implants Segment is Expected to Hold a Significant Market Share in the Medical Implants Market

The orthopedic implants segment is expected to hold a significant market share in the medical implants market. Orthopedic implants are medical implant devices used to replace missing joints or bones or to support damaged bones. These devices are manufactured using titanium alloys and stainless steel for strength, while plastic coating acts as artificial cartilage. Internal fixation is a type of surgery in orthopedics involving implant implementation to repair the damaged bone. These implants also treat deformities, stabilize body posture, and restore normal skeletal function.

Furthermore, as the COVID-19 pandemic has burdened the healthcare system, there has been a decrease in the number of orthopedic surgeries performed, thereby restricting the demand for medical implants. However, demand is expected to increase post-pandemic over the coming years. Moreover, orthopedic implants have witnessed a shift from conventional surgical procedures to modern fixation and prosthetic devices. The demand for orthopedic implants has increased significantly because of the senior population's increased risk of osteoporosis, osteoarthritis, and other musculoskeletal disorders.

The article titled "Microstructural Analysis of Fractured Orthopedic Implants" published in April 2021 reported that stainless steel and titanium alloys are widely used as implant materials in orthopedic surgery due to their good biocompatibility, corrosion resistance, and durability. It also reported that these materials are suitable for the production of bio-components used in medicine due to their relatively high tolerance.

In addition, rising launches of orthopedic implants by key market players are also expected to drive the growth of this segment. For instance, in August 2021, the Orthopaedic Implant Company launched its wrist fracture plating technology, the DRPx System, which has received Food and Drug Administration approval to enable ambulatory surgical centers (ASCs) and hospitals to improve their financial sustainability. In October 2020, Medtronic in the United States launched the Adaptix Interbody System, a navigated titanium spine implant with Titan nanoLOCK surface technology.

Therefore, this segment is expected to grow over the forecast period due to the above factors.

North America is Expected to Hold a Significant Share in the Market and Expected to do Same Over the Forecast Period

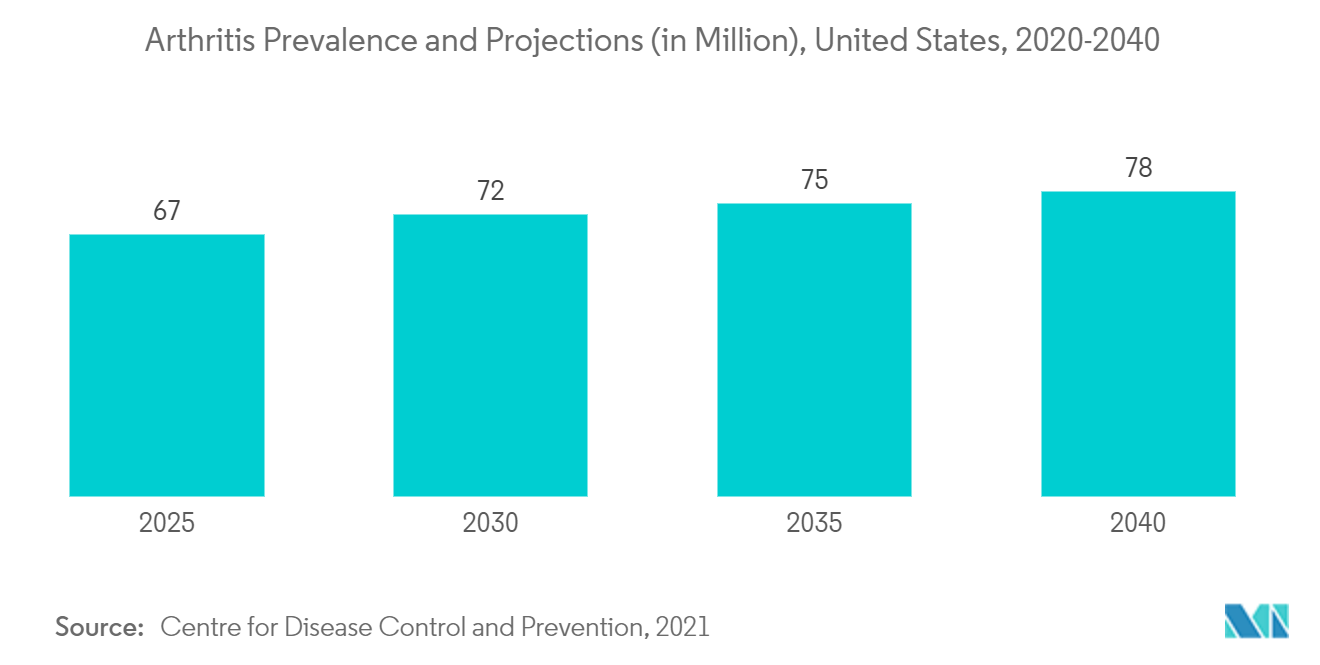

North America currently holds a major share in the global medical implants market and is expected to follow the same trend throughout the forecast period. This is due to several factors, such as the rising incidence of diseases like arthritis, the rising adoption of cosmetic dental procedures due to tooth loss in the country, well-established insurance policies, and the availability of advanced healthcare infrastructure.

For instance, according to the American Dental Association 2020, more than 5 million United States seniors aged 65 to 74 have complete tooth loss, with nearly 3 million edentulous. Tooth loss, on the other hand, is primarily a problem for the elderly. This is because 91 percent of adults aged 20 to 64 have dental caries, with 27 percent going untreated. Furthermore, tooth decay is a common cause of tooth loss in many cases. As a result, teeth gradually loosen and fall out. Thus, the senior dental loss is a common problem due to dental diseases, thereby driving the demand for dental implants in the geriatric population.

Furthermore, the introduction of new implants into the market is also driving growth in the region. For instance, in September 2020, Ditron Dental USA launched its commercial operations in the United States for its dental implant portfolio. Likewise, in June 2022, ZimVie Inc. announced that the Food and Drug Administration-cleared T3 PRO Tapered Implant and Encode Emergence Healing Abutment in the United States. The T3 PRO is the newest addition to ZimVie’s family of dental implants and builds on the proven solutions of the T3 Tapered Implant. Similarly, in February 2022, DeGen Medical, Inc., a spinal implant company specializing in augmented reality and patient-specific solutions, launched Impulse AM, a 3D-printed porous titanium implant for posterior interbody fusion. Therefore, the rise in the launch of medical implants in the United States will lead to increased adoption, thereby driving market growth in this region.

Hence, owing to the abovementioned factors, the North American market is expected to drive swiftly.

Medical Implants Industry Overview

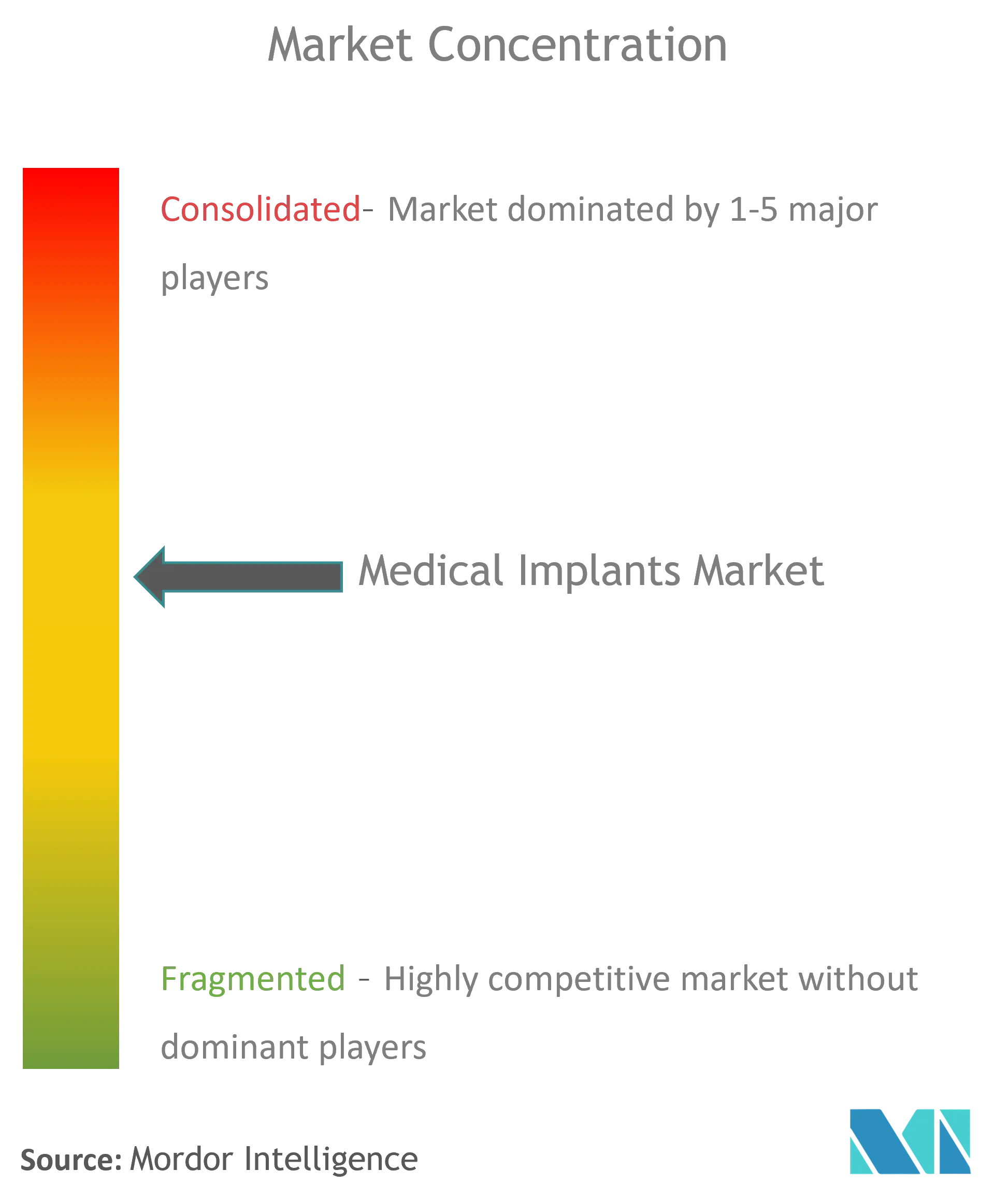

The medical implants market is fragmented and consists of several major players. In terms of market share, a few major players dominate the market. Some prominent players are vigorously making acquisitions of other companies to consolidate their market positions globally. These major global medical implants market companies include Abbott Laboratories, 3M Company, Strauman AG, Dentsply Sirona, Johnson & Johnson Limited, Stryker, and Boston Scientific Corporation, among others.

Medical Implants Market Leaders

Smith & Nephew PLC

Stryker Corporation

Zimmer Biomet

CONMED Corporation

Boston Scientific

*Disclaimer: Major Players sorted in no particular order

Medical Implants Market News

- In March 2022, SurGenTec, a privately held spine and orthopedic technology company based in Florida, the United States, received clearance from the United States Food and Drug Administration (FDA) for ION Screw, its proprietary stand-alone spine fixation implant.

- In February 2022, 4WEB Medical launched a new array of hyperlordotic lateral spine implants, the Hyperlordotic Lateral Spine Truss System (LSTS). The latest addition to the LTST portfolio includes 18, 24, and 30-degree lordotic angles in anterior longitudinal release procedures for spine correction.

Medical Implants Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Geriatric Population and Burden of Chronic Diseases

4.2.2 Increasing Demand for Cosmetic Dentistry

4.2.3 Technological Advancements in the Medical Implants

4.3 Market Restraints

4.3.1 Stringent Regulatory Reforms

4.3.2 Reimbursement Issues and High Cost of Medical Implants

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

5.1 By Product

5.1.1 Orthopedic Implants

5.1.1.1 Hip Orthopaedic Device

5.1.1.2 Joint Reconstruction

5.1.1.3 Knee Orthopedic Devices

5.1.1.4 Spine Orthopedic Devices

5.1.1.5 Other Products

5.1.2 Cardiovascular Implants

5.1.2.1 Pacing devices

5.1.2.2 Stents

5.1.2.3 Structural Cardiac Implants

5.1.3 Ophthalmic implants

5.1.3.1 Intraocular lens

5.1.3.2 Glaucoma Implants

5.1.4 Dental Implants

5.1.5 Facial Implants

5.1.6 Breast Implants

5.1.7 Other Implants

5.2 By Type of Material

5.2.1 Metallic Biomaterial

5.2.2 Polymers Biomaterial

5.2.3 Natural Biomaterial

5.2.4 Ceramic Biomaterial

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Abbott Laboratories

6.1.2 Biotronik SE & Co. KG

6.1.3 Boston Scientific Corporation

6.1.4 Cardinal Health, Inc.

6.1.5 Conmed Corporation

6.1.6 Globus Medical, Inc.

6.1.7 Integra Lifesciences Holdings Corporation

6.1.8 Johnson & Johnson

6.1.9 Smith & Nephew PLC

6.1.10 Stryker Corporation

6.1.11 Zimmer Biomet

6.1.12 Straumann AG

6.1.13 Dentsply Sirona

6.1.14 Osstem Implant Co. Ltd

6.1.15 Henry Schein Inc.

6.1.16 Abbvie Inc. (Allergan PLC)

6.1.17 Ivoclar Vivadent Inc.

6.1.18 GC Aesthetics

6.1.19 3M Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Medical Implants Industry Segmentation

As per the scope of the report, medical implants are devices or tissues placed inside or on the body's surface. Many implants are prosthetics intended to replace missing body parts. Other implants deliver medication, monitor body functions, or support organs and tissues. The Medical Implants Market is Segmented by Product (Orthopedic Implants (Hip Orthopedic Device, Joint Reconstruction, Knee Orthopedic Devices, Spine Orthopedic Devices, Other Products), Cardiovascular Implants (Pacing devices, Stents, Structural Cardiac Implants), Ophthalmic Implants ( Intraocular lens, Glaucoma Implants), Dental Implants, Facial implants, and Breast implants, and Other Products)), Type of Material (Metallic Biomaterial, Polymers Biomaterial, Natural Biomaterial, and Ceramic Biomaterial), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| By Product | |||||||

| |||||||

| |||||||

| |||||||

| Dental Implants | |||||||

| Facial Implants | |||||||

| Breast Implants | |||||||

| Other Implants |

| By Type of Material | |

| Metallic Biomaterial | |

| Polymers Biomaterial | |

| Natural Biomaterial | |

| Ceramic Biomaterial |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Medical Implants Market Research FAQs

How big is the Global Medical Implants Market?

The Global Medical Implants Market size is expected to reach USD 111.33 billion in 2023 and grow at a CAGR of 7.20% to reach USD 157.62 billion by 2028.

What is the current Global Medical Implants Market size?

In 2023, the Global Medical Implants Market size is expected to reach USD 111.33 billion.

Who are the key players in Global Medical Implants Market?

Smith & Nephew PLC, Stryker Corporation, Zimmer Biomet, CONMED Corporation and Boston Scientific are the major companies operating in the Global Medical Implants Market.

Which is the fastest growing region in Global Medical Implants Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Global Medical Implants Market?

In 2023, the North America accounts for the largest market share in the Global Medical Implants Market.

Medical Implants Industry Report

Statistics for the 2023 Medical Implants market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Medical Implants analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.