Modular Data Center Market Size

| Study Period | 2019-2027 |

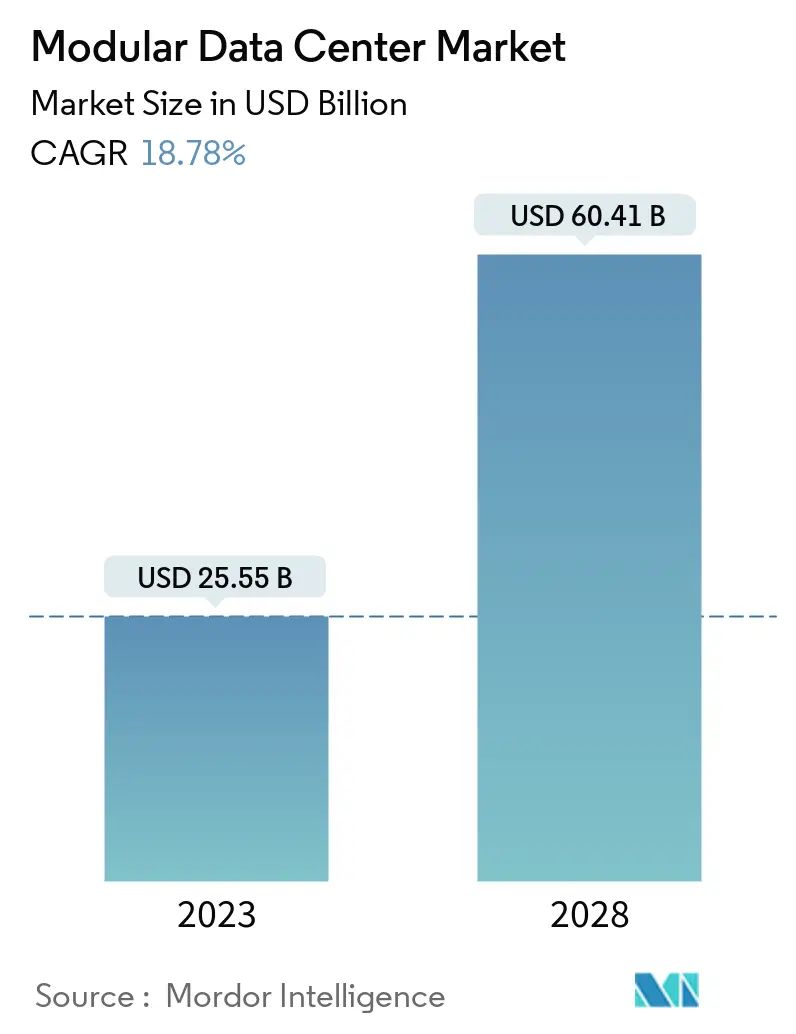

| Market Size (2023) | USD 25.55 Billion |

| Market Size (2028) | USD 60.41 Billion |

| CAGR (2023 - 2028) | 18.78 % |

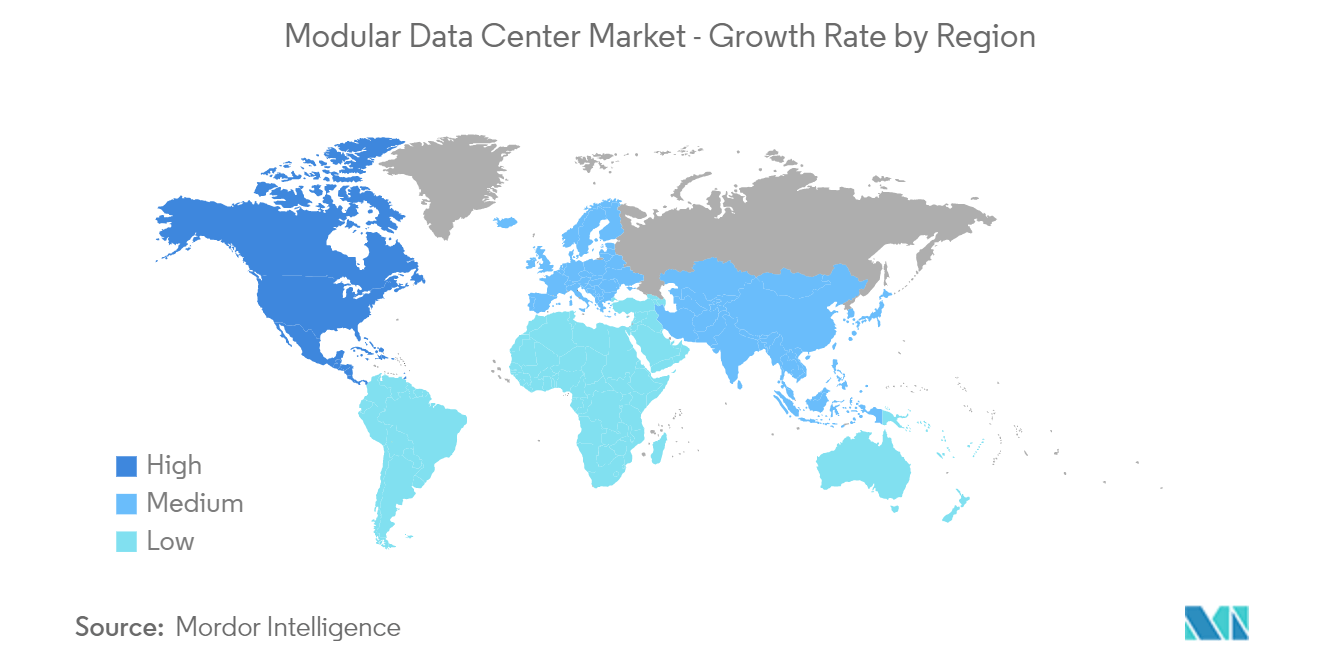

| Fastest Growing Market | Europe |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Modular Data Center Market Analysis

The Modular Data Center Market size is expected to grow from USD 25.55 billion in 2023 to USD 60.41 billion by 2028, at a CAGR of 18.78% during the forecast period (2023-2028).

- Modular data center solution units facilitate the physical build of IT infrastructure. The modular approach can be focused on the data center or a more granular level. As organizations adopt more cloud-based distributed technologies, modular architecture can support additional workloads to support business demands. These portable data centers offer a cost-effective way of securing computing power without adding extra floor space to meet the rising demand for cloud, mobile, and social analytics.

- Green data centers are in high demand, driving the market growth. Green data centers use energy-efficient management methods and technology, providing enterprises with little environmental impact and optimum efficiency. Because of the increase in energy consumption and environmental protection requirements set by governments worldwide, modular data centers are in high demand. One of the most significant advantages of modular data centers is that, compared to traditional data centers, they consume less power and are more energy-efficient, allowing them to meet companies' intrinsic requirements for lower energy usage.

- In January this year, For security and economic growth purposes, the Japanese government will invest about JPY 50 billion (USD 440 million) in subsea cable and data center decentralization. More than 60% of data centers are located in Tokyo, but most key international cables currently land in east Japan. In addition to constructing 12 data centers in remote locations over five years, the government wants to install a submarine cable around the entire nation in three years.

- The creation of vast amounts of data is driving firms to develop new solutions to store and keep it efficiently. The growing use of cloud-based tools and applications allows the government and key players to centralize, compute, improve operational efficiency, and reduce overall energy consumption. This will enable businesses to adapt to changing demands for vital IT power. As a result, the adoption of cloud-based solutions and services is likely to contribute to the growth of the global market over the forecast period.

- Further, According to Germany's digital group Bitkom, the COVID-19 pandemic and widespread digitization have accelerated the country's data center performance. According to a Bitkom study, the capacity of data processing centers in Germany expanded by 84% in IT performance between 2010 and 2020 and will continue to grow by another 30% by 2025.

- Prefabricated modules are huge and heavy, and while transportable, they can be difficult to position and relocate. Modules may be too heavy to place on a building's roof or cause logistical issues in congested city streets. The data center module is often transported to a place by truck. However, many countries and regions restrict truck transportation on public roads. Furthermore, the modular data center is often created and containerized. Still, room-based cooling and challenge-based cooling are challenging to implement, which used to be most useful when an organization wanted to scale up its existing data center with a modular data center.

Modular Data Center Market Trends

This section covers the major market trends shaping the Modular Data Center Market according to our research experts:

Telecom and IT Sector to Hold Significant Market Growth

- To optimize their networks and the digital services running on them, the telecom providers will need more computing and storage capacity to be deployed across carrier networks. Additionally, the increasing 4G penetration and the upcoming 5G wave further motivate telecom vendors to invest in the modular data center market for more network functionality and a much higher ability to manage networks around the edges due to increased data traffic.

- As carriers can be benefitted in terms of network service optimization, edge computing has become almost a common practice in the telecom industry. The telecom operators are estimated to deploy micro modular data centers and 5G cell towers to provide enterprises across industries with better network connectivity. For instance, according to the Ericsson Mobility report, in the North American region, 5G subscriptions are expected to account for 55% of mobile subscriptions by the end of 2024. As 5G has to ensure higher speeds and lower latency, telecom vendors would turn toward edge computing.

- Further, according to GSMA, 4G technology accounted for 58 % of the market last year, but by 2025, that figure is expected to fall to 55%. By then, the new 5G technology is expected to hold a 25% share of the mobile technology market. The arrival of 5G has now become a driver for developing data centers and the necessary infrastructure to enable 5G. To be successful, current data centers will need to be upgraded to support edge computing and 5G. The infrastructure must be adaptable and capable of recovering from any potential disaster.

- According to their size, the Chinese IT industry requires on-premise private data storage facilities and hyperscale data centers. Furthermore, due to the expansion of SaaS providers, cloud storage selection has advanced throughout the years, allowing them to extend their capacities and create demand for the data center industry. SaaS, along with platform as a service (PaaS) and infrastructure as a service (IaaS), is one of China's three major cloud computing categories. This fuels the demand for more data centers.

- Also, in April last year, Chinese cloud service provider Tencent Cloud launched an internet data center (IDC) in Jakarta, Indonesia, enabling faster data transfers and accelerating various industries' digital transformations. This helps reduce access delays to data and applications and helps businesses and organizations accelerate their digital transformation.

Europe accounts for the Significant Market Share

- Some significant factors driving modular data center demand in Europe are the increasing use of online and cloud-based technology, rising technological proliferation around the world, increasing load on existing data centers, the establishment of new SMEs, and rising demand for energy-efficient and sustainable data centers. Changing environmental laws and regulations worldwide will likely push modular data center companies to create more sustainable designs and solutions.

- The Modular data center market in the united kingdom region is expected to register significant growth due to increasing acceptance and adoption of IoT-based and cloud-based systems that require the implementation of data centers. The expansion of collaborations between governments and numerous other private organizations to lessen businesses' carbon footprints is another factor contributing to the growth of the data center construction industry in the united kingdom. Additionally, the capacity of data centers to store customer information, personnel management data, and electronic financial services like remote banking has increased demand for data centers, supporting the expansion of the modular data center market in the region.

- Further, data center contribution to the nation's economy is expected that the government will develop new policies towards new data center construction players to enter the United kingdom region. For instance, in accordance with the UK government's report on its digital strategy, data centers enable the internet economy, which is growing faster than any other G-20 economy and contributes about 16% of the national GDP, 10% of jobs, and 24% of all UK exports. While the annual GVA contribution of an existing data center is estimated to be between GBP 291 million and GBP 320 million, each new data center ranges from GBP 397 million to GBP 436 million.

- According to the Dutch Data Center Association, 80% of data centers in the Netherlands use green electricity. This means that at least 20% of Dutch data centers are still largely reliant on fossil fuels. The green energy used is often 'light green' electricity ('certified power') and does not come from sustainable electricity generation in the Netherlands. Only a small part of the power supply for data centers is 'dark green,' meaning that it is generated sustainably in the Netherlands. There is still a lot of work to be done, particularly considering the Climate Accord and the objectives of the Dutch Climate Act, namely the almost eradication of greenhouse gases and CO2- neutral electricity generation in this country by 2050.

- According to Cloudscene, there are 264 data centers in France, with most of these colocation facilities situated in and around Paris, Lille, and Lyon. There were 113 data centers in Paris and 20 data centers in Lille. France has several data center markets offering a sufficient supply of facilities to support the surge in growing IT infrastructural needs. However, the Paris metropolitan area, which includes the city of Paris and its surrounding suburbs, remains the country's top market for data centers.

Modular Data Center Industry Overview

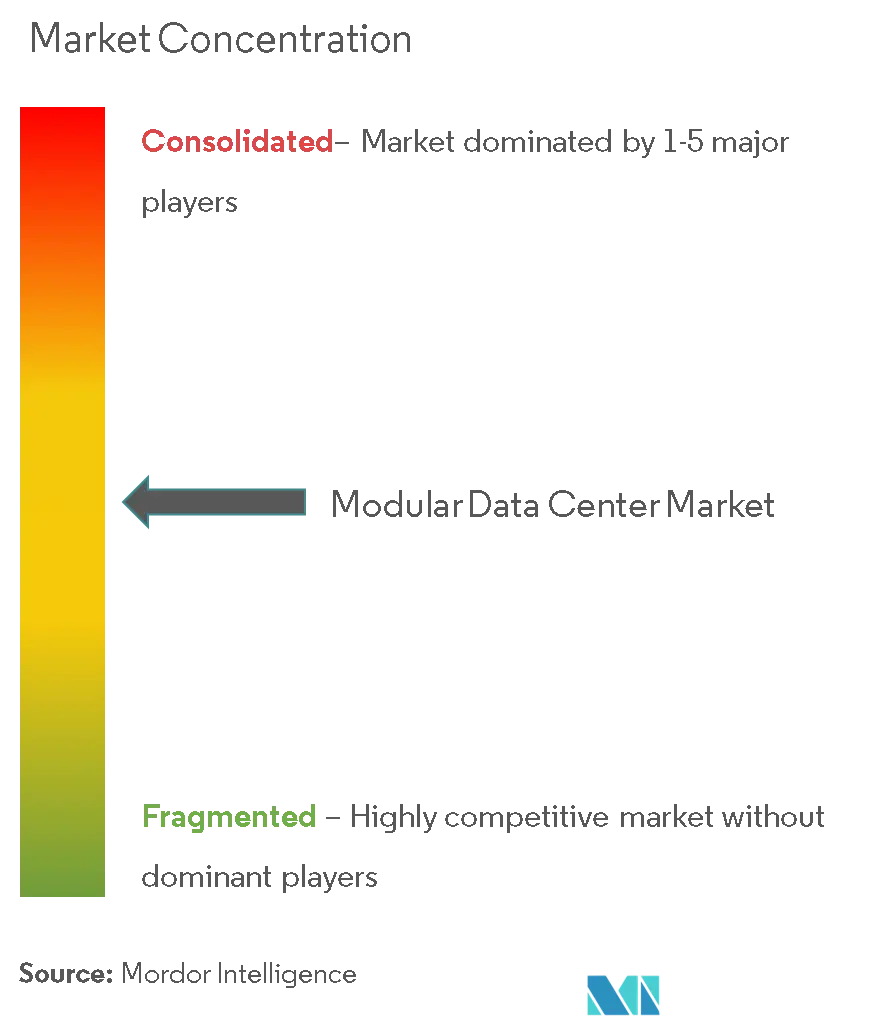

The modular data center market is fragmented, where competition tends to increase and consists of several major players. Few of the major players currently dominate the market, and these major players with a prominent share in the market are focusing on expanding their customer base across foreign countries. Further new players are also entering this market through strategic collaborative initiatives that cater to intense rivalry. Key players are IBM Corporation, Huawei Technologies Co. Ltd, etc. Recent developments in the market are -

In September 2022: In India, Vertiv introduced Vertiv prefabricated modular data centers and infrastructure options. The integrated solutions are flexible platforms suited for IT asset deployment and provide a straightforward way to install capacity in less time. They also offer simple scalability, letting the data center operator start with a solution that suits immediate needs and then scale up as needed. Vertiv's prefabricated modular data centers use the company's crucial power and thermal management capabilities and monitoring and control technology.

In June 2022, Schneider Electric, the global player in digital energy management and automation, announced the launch of its new Easy Modular All-in-One Data Center solution in Europe. Schneider Electric's Easy Modular 'All-in-One' Data Centers combine all power, cooling, and IT equipment into a single, pre-configured solution and provide exceptional value for enterprise and IT organizations looking to implement an edge computing strategy. They are available in four standardized form factors with additional configurable options.

Modular Data Center Market Leaders

IBM Corporation

Huawei Technologies Co. Ltd

Dell EMC (Dell Technologies)

Hewlett Packard Enterprise Development LP

Schneider Electric SE

*Disclaimer: Major Players sorted in no particular order

Modular Data Center Market News

- January 2022: Colocation specialist Colt Data Centre Services (DCS) purchased ten parcels of land for upcoming data centers, targeting key infrastructure hubs across Europe and Asia-Pacific. These include London, Frankfurt, Paris, and an unnamed city in Japan. The company said the locations had secured power capacity of more than 500 MVA, making them suitable for especially large data centers.

- March 2022: CloudHQ, a hyperscale data center developer and operator in the United States and Europe, through its subsidiary CloudHQ UK Limited, is in the process of developing an 81 MW, 831 k sqft (77.2 k sqm), hyperscale data center campus around Didcot, England, a town located 60 miles (97 km) west of Central London.

Modular Data Center Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables & Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Attractiveness Porter's Five Forces Analysis

4.2.1 Threat of New Entrants

4.2.2 Bargaining Power of Buyers/Consumers

4.2.3 Bargaining Power of Suppliers

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Assessment of Impact of COVID-19 on the Industry

4.5 Market Drivers

4.5.1 Mobility and Scalability of Modular Data Centers

4.5.2 Disaster Recovery Advantages

4.6 Market Challenges

5. MARKET SEGMENTATION

5.1 Solution and Services

5.1.1 Function Module Solution (Individual Function Module and All-in-One Function Module)

5.1.2 Services

5.2 Application

5.2.1 Disaster Backup

5.2.2 High Performance/ Edge Computing

5.2.3 Data Center Expansion

5.2.4 Starter Data Centers

5.3 End User

5.3.1 IT

5.3.2 Telecom

5.3.3 BFSI

5.3.4 Government

5.3.5 Other End Users (Healthcare, Retail, Defense, etc.)

5.4 Geography

5.4.1 North America

5.4.2 Europe

5.4.3 Asia-Pacific

5.4.4 Latin America

5.4.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 IBM Corporation

6.1.2 Huawei Technologies Co. Ltd.

6.1.3 Dell EMC

6.1.4 HPE Company

6.1.5 Baselayer Technology LLC

6.1.6 Vertiv Co.

6.1.7 Schneider Electric SE

6.1.8 Cannon Technologies Ltd

6.1.9 Rittal Gmbh & Co. KG

6.1.10 Instant Data Centers LLC

6.1.11 Colt Group SA

6.1.12 Bladeroom Group Ltd.

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

Modular Data Center Industry Segmentation

A modular data center is portable and exists at any location that requires data capacity. This type of data center system comprises modules and components with purpose engineering. Applications such as disaster backup, high-performance/ edge computing, data center expansion, and starter data centers are considered under the scope. '

The modular data center market is segmented by solution and services (function module solution, services), application (disaster backup, high performance/ edge computing, data center expansion, starter data centers), end user (IT, telecom, BFSI, government), and geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Solution and Services | |

| Function Module Solution (Individual Function Module and All-in-One Function Module) | |

| Services |

| Application | |

| Disaster Backup | |

| High Performance/ Edge Computing | |

| Data Center Expansion | |

| Starter Data Centers |

| End User | |

| IT | |

| Telecom | |

| BFSI | |

| Government | |

| Other End Users (Healthcare, Retail, Defense, etc.) |

| Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Modular Data Center Market Research FAQs

How big is the Modular Data Center Market?

The Modular Data Center Market size is expected to reach USD 25.55 billion in 2023 and grow at a CAGR of 18.78% to reach USD 60.41 billion by 2028.

What is the current Modular Data Center Market size?

In 2023, the Modular Data Center Market size is expected to reach USD 25.55 billion.

Who are the key players in Modular Data Center Market?

IBM Corporation, Huawei Technologies Co. Ltd, Dell EMC (Dell Technologies), Hewlett Packard Enterprise Development LP and Schneider Electric SE are the major companies operating in the Modular Data Center Market.

Which is the fastest growing region in Modular Data Center Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2023-2027).

Which region has the biggest share in Modular Data Center Market?

In 2023, the North America accounts for the largest market share in the Modular Data Center Market.

Modular Data Centers Industry Report

Statistics for the 2023 Modular Data Centers market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Modular Data Centers analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.