Philippines Freight & Logistics Market Size

| Study Period | 2019 - 2028 |

| Base Year For Estimation | 2022 |

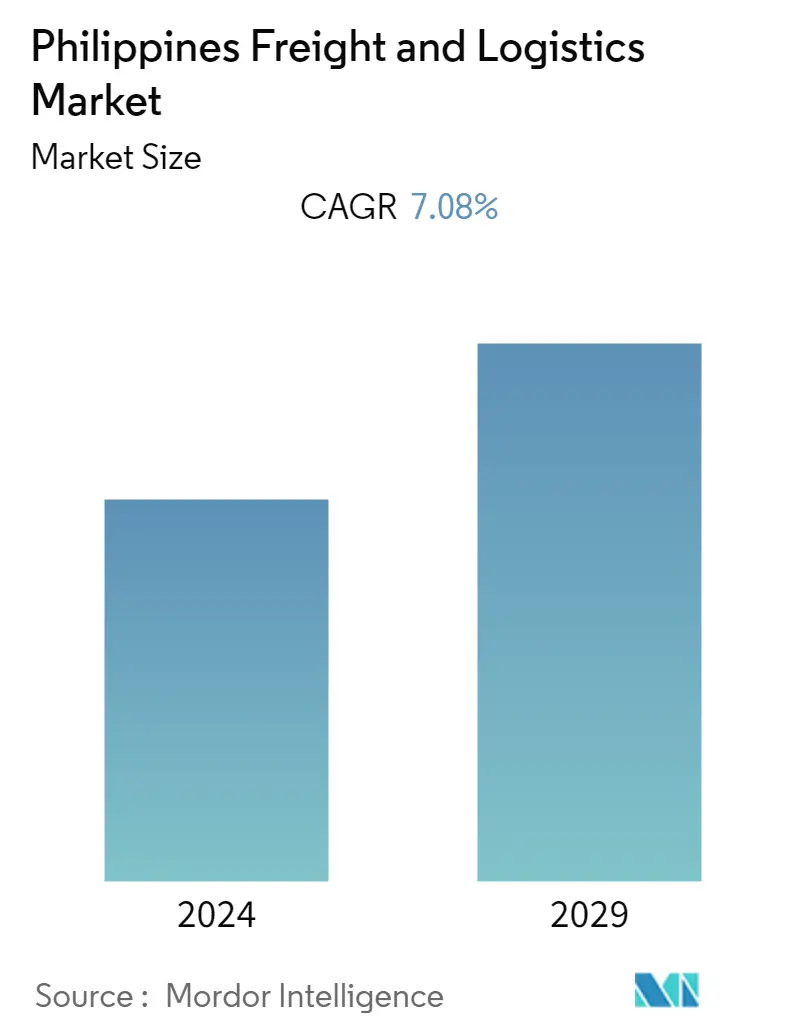

| Market Size (2023) | USD 18.03 Billion |

| Market Size (2028) | USD 25.38 Billion |

| CAGR (2023 - 2028) | 7.08 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Philippines Freight & Logistics Market Analysis

The Philippines Freight and Logistics Market size is estimated at USD 18.03 billion in 2023, and is expected to reach USD 25.38 billion by 2028, growing at a CAGR of 7.08% during the forecast period (2023-2028).

- The pandemic increased e-commerce in the nation as cautious consumers stayed home to avoid coming into contact with disease vectors. As more people purchase online and there are more online retailers in the country, this tendency will likely continue. According to the Philippines' Department of Trade and Industry (DTI), there were 1,700 online sellers in March 2020 and 93,318 in January 2021.

- The warehouse industry is still in high demand, driven by the thriving e-commerce business, and this bodes well for the industrial and logistics real estate sector's growth in 2022. According to a survey by Colliers Philippines, manufacturing, logistics, and e-commerce will continue to grow in 2022. According to Colliers, the industrial vacancy rate in the Cavite-Laguna-Batangas (CALABA) corridor decreased to 5.6% in the first half of 2021 from 5.7% in 2020.

- Colliers attributed the reduction to the increase in the demand for warehouse and storage space from fast-moving consumer goods (FMCG) companies as the country's online retail market continues to expand. The e-commerce sector is anticipated to contribute around PHP 1.2 trillion (USD 25 billion) by 2022, according to the DTI's e-commerce roadmap. According to Colliers Philippines, the increased need for cold storage facilities is anticipated to support demand for industrial assets over the next 12 to 36 months. By 2023, the Board of Investments (BOI) expects the country's cold chain sector to generate PHP 20 billion (USD 417 million) in income.

- The digital shift has been led by e-commerce firms like Lazada, Zalora, and Shopee, who work with tech-driven logistics firms like Ninja Van and Lalamove to transport items so that customers can track their orders in real-time. Switching to digital will increase order status transparency, reduce lead times, and speed up customs clearance processes by up to 80%, taking only 3-5 business days.

Philippines Freight & Logistics Market Trends

This section covers the major market trends shaping the Philippines Freight & Logistics Market according to our research experts:

Growth in e-commerce to drive logistics market in Philippines

- According to Lazada Group, the Philippine e-commerce market is expected to grow faster than its regional competitors. In the next five to ten years, Lazada expects e-commerce in the Philippines and the rest of Southeast Asia to grow "a lot higher" as these countries recover from the pandemic, despite the global economic slowdown and rising prices.

- The e-commerce market in the Philippines has been expanding in recent years. The pandemic boosted e-commerce in the country, as fearful consumers stayed home to avoid being exposed to disease vectors. With the increase in new online buyers and the proliferation of online retailers in the country, this tendency will continue. According to the Department of Trade and Industry, the number of online vendors in the Philippines increased from 1,700 in March 2020 to 93,318 in January 2021. (DTI).

- With 73 million monthly active users, the Philippines' e-commerce business saw revenues of USD 17 billion in 2021. Due to the COVID-19 pandemic, more Filipinos worked from home and shopped online. The leading e-commerce sites in the Philippines include Shopee, Lazada, Zalora, and BeautyMNL. These platforms sell goods from Asia-Pacific nations with free trade agreements with the Philippines. The most popular product categories are household care, electronics, fashion, and beauty products. The working population (ages 25 to 44) actively uses their desktop and mobile devices to access these platforms. Between 2020 and 2021, there was an increase in smartphone household penetration of 2%, reaching 74.1%.

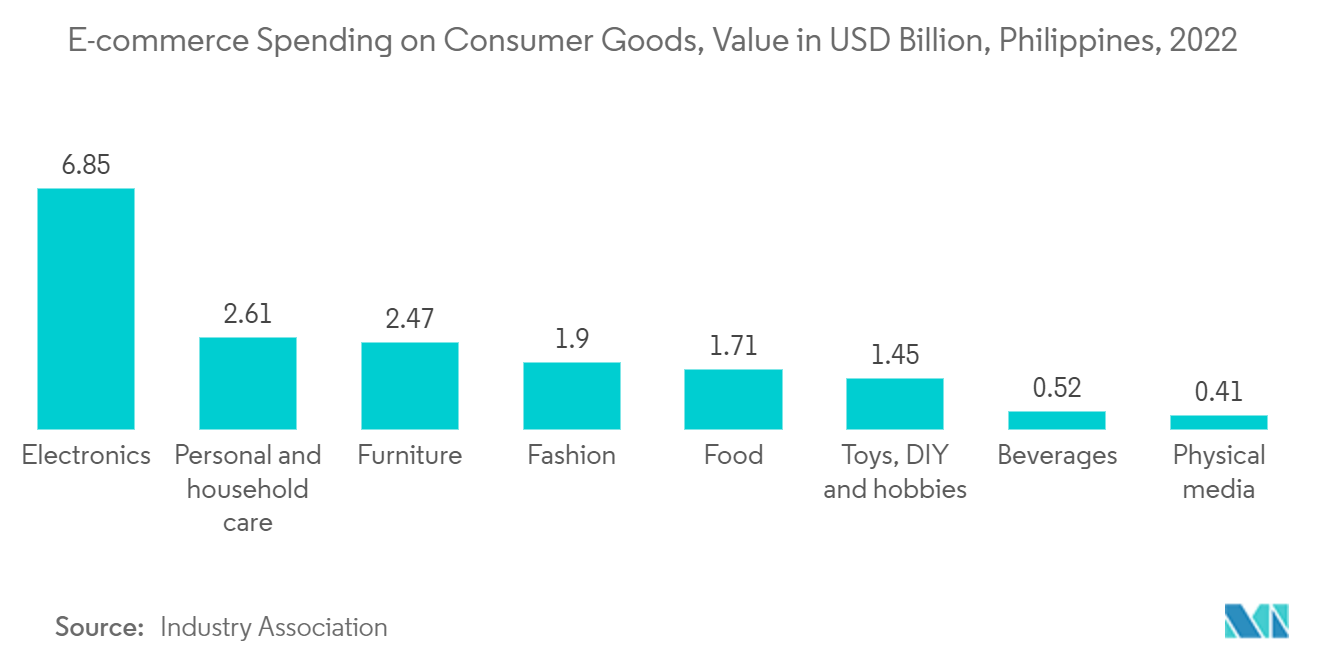

- In August 2021, Lazada Group announced the official rebranding of its logistics arm. The new Lazada Logistics division combines what was previously known as Lazada eLogistics (LeL), which managed third-party providers, and Lazada Express (LEx), the company's parcel-delivery service, and introduced multichannel logistics services that enable order fulfillment and delivery across all e-commerce platforms. While LEx was in charge of customer delivery, LeL managed fulfillment and logistics with third-party logistics (3PL) suppliers. In addition, in 2022, electronic goods witnessed significant sales from e-commerce platforms, and the sales amounted to more than USD 6 billion, followed by personal and household care, furniture, fashion, etc. thus, the growing e-commerce sales creating huge oppurtunity for logistics providers in the country.

Increased spending on infrastructure to propel the freight and logistics market in Philippines

In the customary areas of transportation, energy, and WASH, the Philippines has announced new projects for 2022. (water projects). The local firms continue to hold the majority of the market share, but some collaborations with international players are being formed in new or emerging industries (such as a planned public-private partnership for a data centre) when the local players lack the necessary technological expertise.

Government programs, such as the Philippines Cold Chain Project (PCCP), which is funded by the United States, are also helping to improve the Southeast nation's cold chain logistics infrastructure. The PCCP is a four-year project funded by the US Department of Agriculture (USDA). It is attempting to organize producer groups to increase agricultural productivity and meet international food safety standards by providing improved technologies, expanding cold chain-related markets, and strengthening intermediate organizations.

The Philippines' PHP 11 Bn (USD 214 Million) public-private partnership to rehabilitate Kennon Road has received expressions of interest from possible bidders, including China First Highway Engineering and JFE Engineering Corporation of Japan (PPP). Local building firms First Balfour and Riofil Corporation were among the others. The National Economic and Development Authority (NEDA) of the Philippines is where the DPWH will present the Kennon Road project for final approval. The 33km road has to be widened, 18 bridges need to be upgraded, and slope protection needs to be built.

The Philippines’ railway network is undergoing a rebirth after decades of neglect and underspending that has left it in a decrepit state. Among the government’s top priorities is the flagship North-South Commuter Railway in Manila, its largest-ever individual infrastructure investment. NSCR is envisaged as a 163 route-km suburban railway network connecting the regional growth centres of Clark and New Clark City in the north with central Manila and Calamba City in Laguna province to the south of the capital.

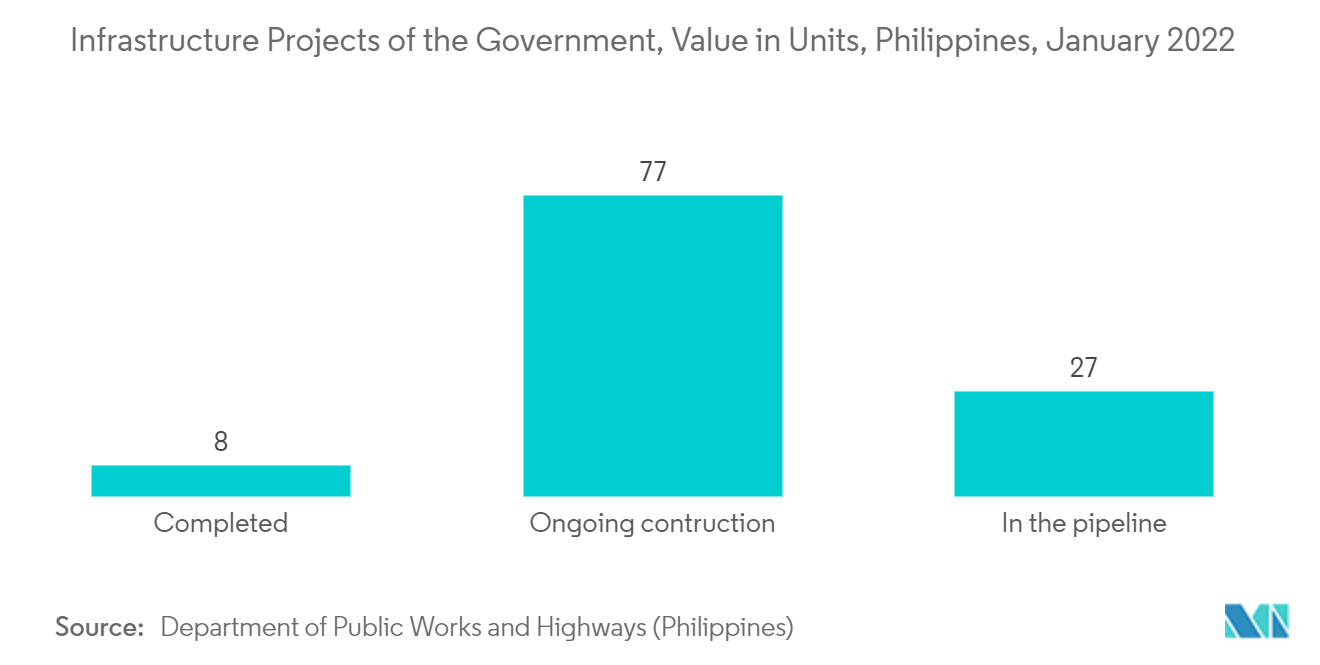

However, in January 2022, according to Department of Public Works and Highways, 15 out of 119 flagship infrastructure projects of the Philippine government had been completed, which includes the improvement of remaining sections along Pasig River. Meanwhile, 77 projects remain at the construction stage while 27 are in the pipeline. thus, the increasing logistics and infrastructure projects across the country expected to fuel the freight and logistics operations.

Philippines Freight & Logistics Industry Overview

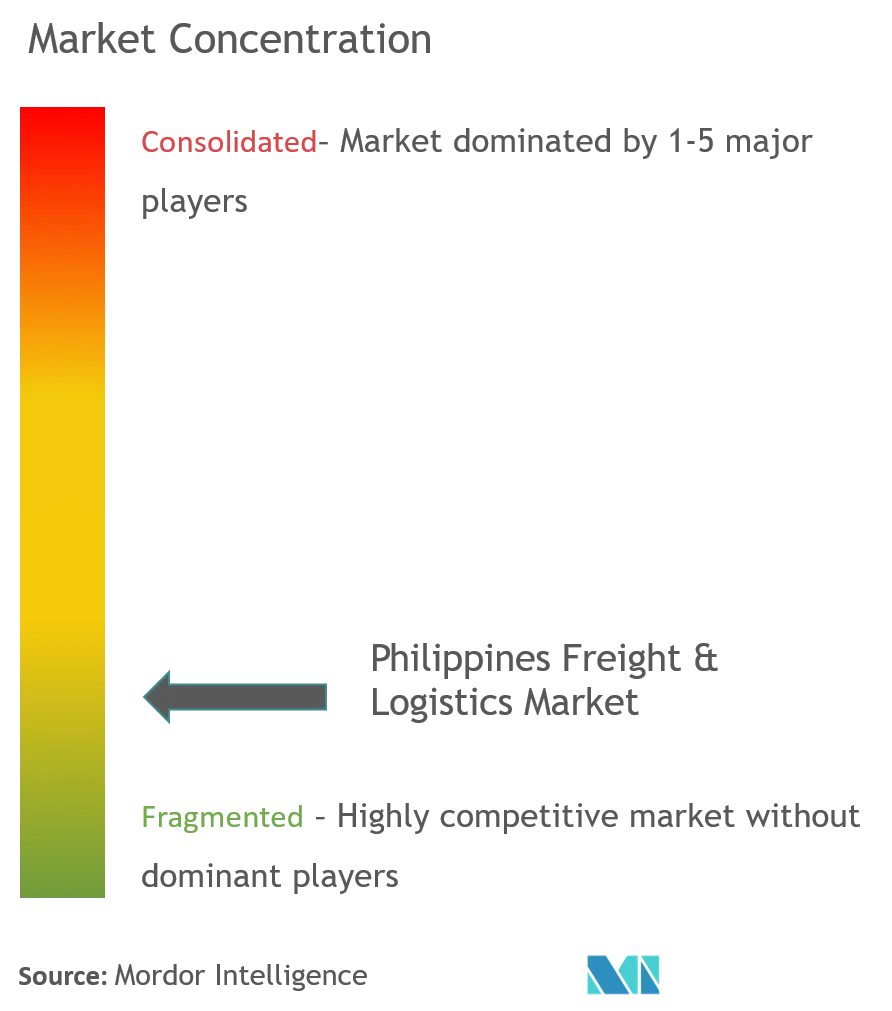

The competition in the Philippines freight and logistics market is fragmented, with the presence of many local and international logistics service providers. Some of the existing major players in the market include – FedEx, UPS, DHL, Kuehne + Nagel, PHL Post, Nippon Express, 2GO Express, etc.

The international players are making strategic investments to establish a regional logistics network, such as opening new distribution centers, smart warehouses, etc. The growth of e-commerce is an essential factor spurring the development of courier services. Increasing consumption and Internet penetration are boosting e-commerce activity in the Philippines.

Philippines Freight & Logistics Market Leaders

DHL

UPS

FedEx

PHL Post

Nippon Yusen NYK (Yusen Logistics)

*Disclaimer: Major Players sorted in no particular order

Philippines Freight & Logistics Market News

- November 2022: The Ayala Group is looking to expand its logistics business further as it focuses on becoming a major player in the lucrative and less-regulated industry. Through its logistics arm AC Logistics Holdings Corp., the diversified conglomerate is keen on acquiring at least one other company to expand its business. In August last year, AC Logistics reached financial close for the acquisition of 60 percent shares in Air 21 Holdings Inc. (AHI) for PHP 6.06 billion (USD 0.19 billion)

- June 2022: To improve its capabilities for the Southeast Asian market, CEVA Logistics established a new 14,000-square-metre facility there. The warehouse will provide a full range of services to the electronics and food and beverage industries. The facility comprises 13 loading bays, floor staging, ambient and temperature-controlled dangerous goods storage, and an optimum shelf arrangement that can hold up to 16,000 pallet placements.

Philippines Freight & Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS AND MARKET DYNAMICS

4.1 Current Market Scenario

4.2 Government Regulations and Initiatives

4.3 Market Dynamics

4.3.1 Drivers

4.3.2 Restraints

4.3.3 Opportunities

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitutes

4.4.5 Intensity of Competitive Rivalry

4.5 Industry Value Chain/Supply Chain Analysis

4.6 Technological Trends

4.7 Insights on the E-commerce Industry

4.8 Insights on Logistics Infrastructure Development in Philippines

4.9 Brief on Courier, Express, and Parcel (CEP) market in Philippines (Market Size and Forecast)

4.10 Insights on 3PL market in Philippines

5. MARKET SEGMENTATION

5.1 By Function

5.1.1 Freight Transport

5.1.1.1 Road

5.1.1.2 Sea & Inland Water

5.1.1.3 Air

5.1.1.4 Rail

5.1.2 Freight Forwarding

5.1.3 Warehousing

5.1.4 Value-added Services and Others

5.2 By End User

5.2.1 Manufacturing and Automotive

5.2.2 Oil and Gas, Mining, and Quarrying

5.2.3 Agriculture, Fishing, and Forestry

5.2.4 Construction

5.2.5 Distributive Trade

5.2.6 Healthcare and Pharmaceuticals

5.2.7 Other End Users

6. COMPETITIVE LANDSCAPE

6.1 Overview (Market Concentration and Major Players)

6.2 Company Profiles

6.2.1 Deutsche Post DHL Group

6.2.2 FedEx Corporation

6.2.3 United Parcel Service (UPS)

6.2.4 Nippon Yusen NYK (Yusen Logistics)

6.2.5 PHL Post

6.2.6 Nippon Express

6.2.7 LBC Express

6.2.8 2GO Express

6.2.9 JRS Express

6.2.10 DB Schenker

6.2.11 Kuehne + Nagel International AG

6.2.12 CJ Logistics*

- *List Not Exhaustive

6.3 Other Companies

7. FUTURE OF THE MARKET

8. APPENDIX

8.1 Macroeconomic Indicators

8.2 Insights on Capital Flows

8.3 External Trade Statistics

8.4 Economic Statistics - Transport and Storage Sector Contribution to Economy

Philippines Freight & Logistics Industry Segmentation

Freight refers to any type of goods, items, or commodities that are transported in bulk via air transport, surface transport, or sea/ocean transport. Logistics refers to managing how resources are acquired, stored, and transported to their final destination. A complete background analysis of the Philippines freight and logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Philippines freight and logistics market is segmented by function (freight transport, freight forwarding, warehousing, and value-added services and other services) and end-user (manufacturing and automotive, oil and gas, mining, and quarrying, agriculture, fishing, and forestry, construction, distributive trade, healthcare and pharmaceutical, and other end users). The report offers market size and forecasts for the Philippines freight and logistics market in value (USD billion) for all the above segments.

| By Function | ||||||

| ||||||

| Freight Forwarding | ||||||

| Warehousing | ||||||

| Value-added Services and Others |

| By End User | |

| Manufacturing and Automotive | |

| Oil and Gas, Mining, and Quarrying | |

| Agriculture, Fishing, and Forestry | |

| Construction | |

| Distributive Trade | |

| Healthcare and Pharmaceuticals | |

| Other End Users |

Philippines Freight & Logistics Market Research FAQs

How big is the Philippines Freight and Logistics Market?

The Philippines Freight and Logistics Market size is expected to reach USD 18.03 billion in 2023 and grow at a CAGR of 7.08% to reach USD 25.38 billion by 2028.

What is the current Philippines Freight and Logistics Market size?

In 2023, the Philippines Freight and Logistics Market size is expected to reach USD 18.03 billion.

Who are the key players in Philippines Freight and Logistics Market?

DHL, UPS, FedEx, PHL Post and Nippon Yusen NYK (Yusen Logistics) are the major companies operating in the Philippines Freight and Logistics Market.

Logistics in the Philippines Industry Report

Statistics for the 2023 Logistics in the Philippines market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Logistics in the Philippines analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.