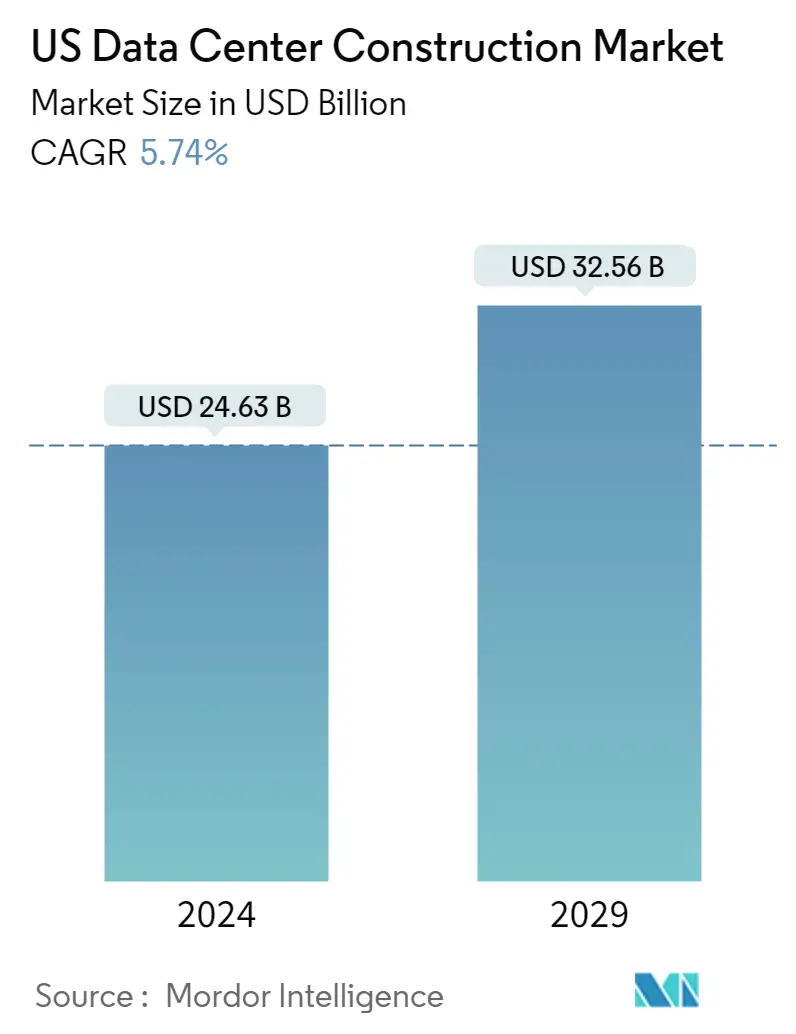

US Data Center Construction Market Size

| Study Period | 2018 - 2028 |

| Base Year For Estimation | 2022 |

| Market Size (2023) | USD 23.29 Billion |

| Market Size (2028) | USD 30.79 Billion |

| CAGR (2023 - 2028) | 5.74 % |

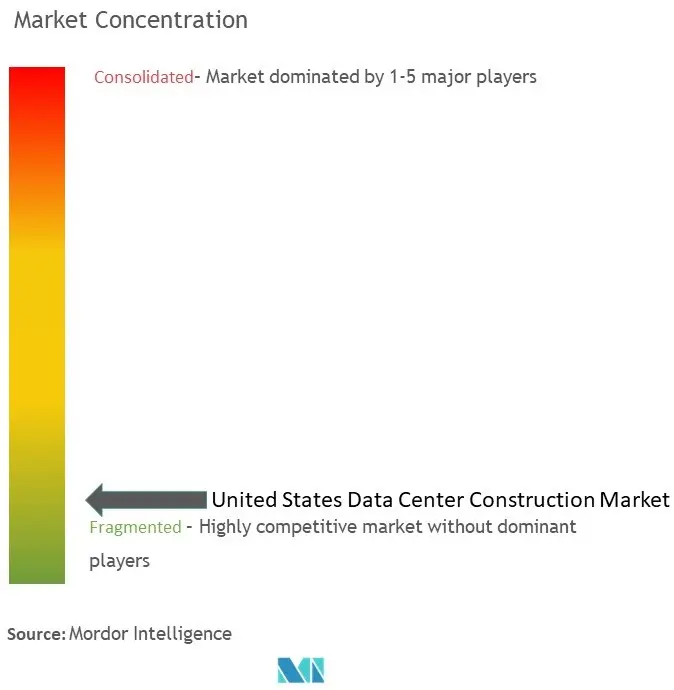

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

US Data Center Construction Market Analysis

The United States Data Center Construction Market size is expected to grow from USD 23.29 billion in 2023 to USD 30.79 billion by 2028, at a CAGR of 5.74% during the forecast period (2023-2028).

- Data center construction is a very complex task requiring extensive planning of electrical, location, and mechanical requirements. Moreover, the data centers carry out mission tasks. Any imperfection in power management to building design could be catastrophic and result in increased company costs.

- The United States data center construction market is a rapidly growing industry driven by the increasing demand for data storage and processing capabilities. The growth of cloud computing, the Internet of Things (IoT), artificial intelligence (AI), and other emerging technologies have led to an exponential increase in data generation, storage, and processing needs, which, in turn, has resulted in a surge in the construction of data centers in the United States.

- The growing adoption of cloud applications, artificial intelligence (AI), and big data is driving the demand for data center construction. As more businesses and organizations shift their operations to the cloud, they require larger and more advanced data centers to support their needs.

- The rising adoption of hyperscale data centers is a significant driver of the data center construction market. Hyperscale data centers are large-scale facilities designed to support the massive amounts of data processing and storage required by modern businesses and organizations.

- The increase in real estate costs is one of the key factors restraining the growth of the data center market. As the demand for data centers continues to rise, the cost of acquiring and developing land for data center construction has also increased significantly.

- The COVID-19 pandemic led to a disruption in the supply chain for the construction of data centers. The lockdowns delayed the completion of projects and caused a decline in demand from severely hit industries, such as hospitality, entertainment, and construction activities. The surge on the internet and cloud adoption increased significantly during the spread of COVID-19 with a shift to the remote working environment and a focus on digitization by government authorities. Such factors are propelling the demand for increasing data center capacities in most regions across the globe.

US Data Center Construction Market Trends

Growing Cloud Applications, AI, and Big Data Drives the the Market Growth

- Cloud applications have become increasingly popular in recent years, as they allow businesses to access software and services over the internet rather than installing and maintaining them on their own hardware. This has led to a surge in demand for cloud-based data storage and processing capabilities, which large data centers typically provide.

- For instance, in December 2022, a new Oracle Cloud Infrastructure (OCI) region officially began operations in Chicago. The new area, Oracle's fourth in the United States and 41st overall, is a public cloud region. The business also runs in two general US Government regions, three Department of Defense-specific US Government regions, several US National Security regions, a TikTok plant in Texas, and regions in Ashburn, Virginia, Phoenix, Arizona, and San Jose, California.

- Artificial intelligence (AI) and big data also require significant amounts of data storage and processing power. AI algorithms require vast amounts of data to be processed quickly, and big data analytics require massive amounts of storage and processing power to handle large datasets. This has increased demand for data centers with advanced computing capabilities, such as graphics processing units (GPUs) and artificial intelligence accelerators.

- For instance, the National Science Foundation started its program for AI Research Institutes in 2020. Since then, 18 colleges in 40 states have received USD 360 million through this scheme. An ecosystem-based strategy can produce AI innovations and introduce AI business owners to the market. In the fiscal year 2022, US federal agencies proposed USD 1.7 billion for non-defense AI research and development. By 2026, non-defense-related AI research and development should get 32 billion USD yearly, according to the National Security Commission for AI. This is expected to increase the demand for Data Centers in the region.

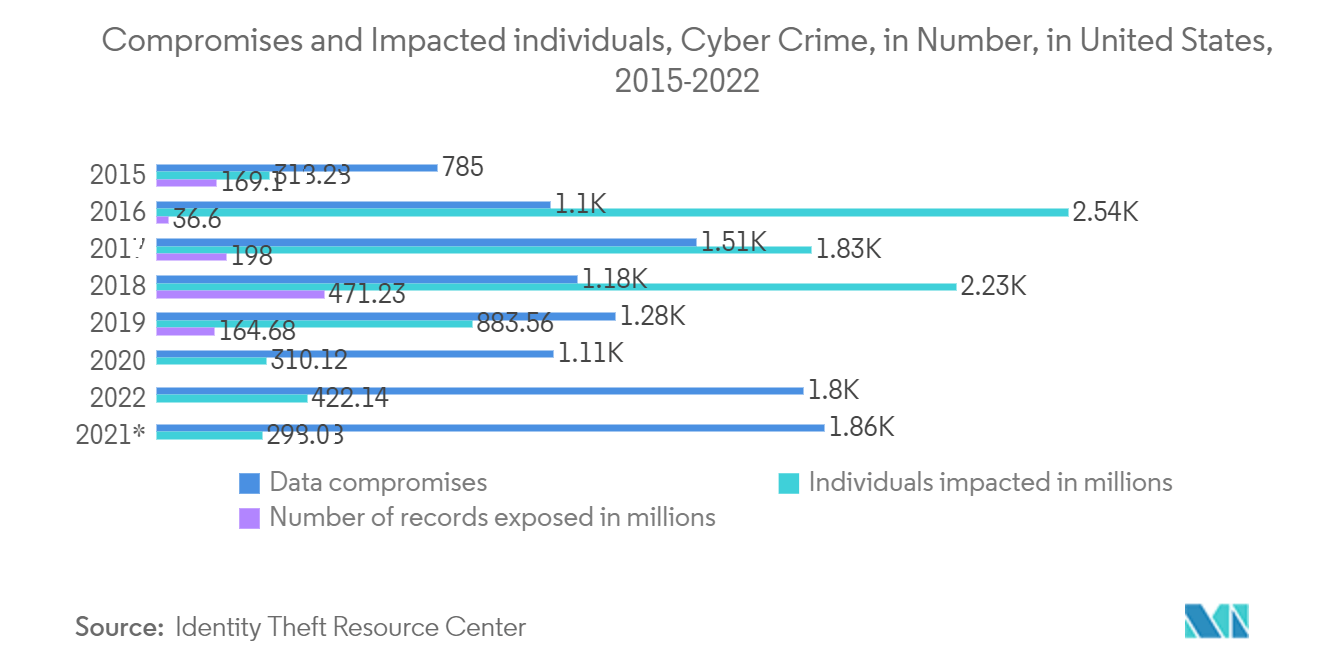

- Furthermore, the increasing need for data privacy and security is also driving the demand for data centers. According to Identity Theft Resource Center, The number of data compromises in the United States in 2022 was 1802. However, approximately 422 million people were affected by data intrusions in the same year, including data breaches, leakage, and exposure. While they are three distinct incidents, they have one feature. An unauthorized threat actor can access sensitive data due to all three instances. With the rise in cyber threats and data breaches, businesses and organizations seeking secure and reliable data storage and processing solutions, which advanced data centers can only provide.

- In summary, the growth of cloud applications, AI, and big data is driving the demand for advanced data centers. As businesses and organizations increasingly rely on these technologies to support their operations, the demand for data center construction is expected to grow. This presents a significant opportunity for businesses and investors looking to enter the data center market.

Healthcare End User Vertical Holds Significant Market Share

- Data center construction is expected to witness substantial demand during the forecast period due to the growth in digital data owing to technological advances and government incentives to implement Electronic Health Records (EHR), the proliferation of IoT, and smart devices in the country's healthcare sector. In addition, the increased enforcement of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) security is further forcing healthcare organizations to upgrade data security and disaster recovery protocols or face high penalties.

- Moreover, with the introduction of the Electronic Medical Records (EMR) Mandate in the United States, healthcare organizations nationwide have adopted cloud-based healthcare solutions to store and protect patient records. Most hospitals and healthcare organizations use cloud storage for patients' healthcare data. Electronic health records are stored in the cloud and updated electronically by physicians, nurses, and other healthcare providers. Such factors augment the demand for data center construction, owning to the growth in digital data in the healthcare sector.

- The digitization of consumer healthcare records in the form of electronic medical records (EMR) has significantly contributed to massive data generation. The latest innovations in medical equipment and the modernization of legacy operating systems, such as the management of personnel and the improvement in the patient response systems, generate a multitude of data, further necessitating the need for secured data center construction initiatives in the country.

- Furthermore, the healthcare sector in the United States is rapidly using deep learning, machine learning, precision medicine, and artificial intelligence (AI), thus generating significant sensitive patient and employee data. Such developments are further analyzed to drive the demand for data center construction in the country during the forecast period.

- Technologies like IoT have many healthcare applications, from remote monitoring to medical device integration. It also has the potential to keep patients healthy and safe and improve how physicians deliver care. However, sensors, wearables, remote monitors, and other medical devices produce a massive amount of data.

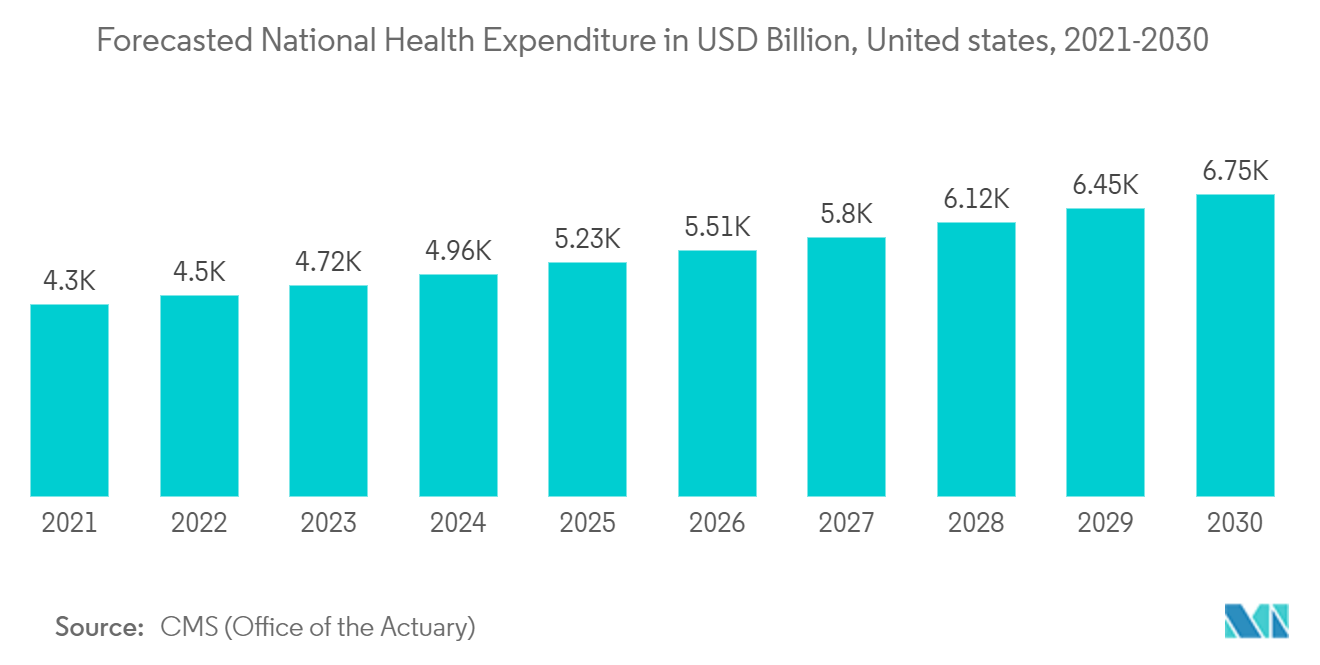

- Moreover, the government of the country continuously recognizes the role of digital health and technological innovation in healthcare as an integral part of successful healthcare infrastructure. The government is making significant strides to make the healthcare sector technologically advanced and continuously increasing its healthcare expenditure to support the healthcare sector. For instance, according to the data from CMS (Office of the Actuary), the forecasted U.S. national health expenditure was expected to reach USD 6751.4 billion in 2030 from USD 4297.1 billion in 2021.

US Data Center Construction Industry Overview

The United States data center construction market is highly fragmented with the precence of major players like IBM Corporation, Schneider Electric SE, DPR Construction Inc., Fortis Construction Inc., and Hensel Phelps Construction Co. Inc. Players in the market are adopting strategies such as partnerships, mergers, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In January 2023, Metro Edge finalized agreements with Clune Construction and other construction companies to design and build the data center facility. The project is expected to have full entitlements within the next few months and break ground shortly after.

In July 2022, IBM announced the acquisition of Databand.ai, one of the leading providers of data observability software that enables businesses to correct data problems such as errors, pipeline failures, and poor quality before they have an adverse effect on their bottom line. This enhances IBM's software portfolio spanning data, artificial intelligence (AI), and automation to cover the complete spectrum of observability and aids organizations in ensuring that reliable data is placed in the hands of the appropriate individuals at the appropriate time.

US Data Center Construction Market Leaders

IBM Corporation

Schneider Electric SE

DPR Construction Inc.

Fortis Construction Inc.

Hensel Phelps Construction Co. Inc.

*Disclaimer: Major Players sorted in no particular order

US Data Center Construction Market News

- October 2022: Red Hat associate teams and product roadmaps for storage were added by IBM to the IBM Storage business segment, enabling uniform application and data storage across on-premises infrastructure and the cloud. With this change, IBM will use Red Hat OpenShift Data Foundation (ODF) storage technology as the basis for IBM Spectrum Fusion. This enhances IBM's capabilities in the developing Kubernetes platform market by combining the container storage technologies from Red Hat and IBM for data services. Moreover, IBM plans to develop new Cephsolutions that give a unified, software-defined storage platform that spans the architectural gap between data centers and cloud providers.

- September 2022: Data center operators and industrial companies increasingly use unmanaged switches to connect edge devices for Industrial Internet of Things (IIoT) applications. These switches allow Ethernet devices to stream data reliably for aggregation and analysis. Antaira, an industrial networking and communication product manufacturer, released the LNP-0800G and LNP-0800G-24 unmanaged switch models with power over ethernet (PoE). These fanless switches, housed in rigid, IP30-rated DIN-rail metal cases, provide long-term reliability in harsh industrial settings, including extreme applications where temperatures range from -10°C to 65°C (LNP-0800G) or -40°C to 75°C (LNP-0800G) (LNP-0800G-24).

US Data Center Construction Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Market Dynamics

4.2.1 Market Drivers

4.2.1.1 Growing Cloud Applications, AI, and Big Data

4.2.1.2 Rising Adoption of Hyperscale Data Centers

4.2.2 Market Restraints

4.2.2.1 Increase in Real Estate Costs

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Threat of New Entrants

4.3.3 Bargaining Power of Buyers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Key US Data Center Construction Statistics

4.4.1 Number of Data Centers in the United States, 2021 and 2022

4.4.2 Data Center Under Construction in the United States, in MW, 2020 - 2022

4.4.3 Average Capex and Opex for the United States Data Center Construction

4.4.4 Data Center Power Capacity Absorption, in MW, Selected Cities, United States, 2021 and 2022

4.5 Assessment of Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

5.1 By Infrastructure

5.1.1 Electrical Infrastructure

5.1.1.1 UPS Systems

5.1.1.2 Other Electrical Infrastructure

5.1.2 Mechanical Infrastructure

5.1.2.1 Cooling Systems

5.1.2.2 Racks

5.1.2.3 Other Mechanical Infrastructure

5.1.3 General Construction

5.2 By Tier Type

5.2.1 Tier-I and -II

5.2.2 Tier-III

5.2.3 Tier-IV

5.3 By End User

5.3.1 Banking, Financial Services, and Insurance

5.3.2 IT and Telecommunications

5.3.3 Government and Defense

5.3.4 Healthcare

5.3.5 Other End Users

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles*

6.1.1 IBM Corporation

6.1.2 Schneider Electric SE

6.1.3 DPR Construction Inc.

6.1.4 Fortis Construction Inc.

6.1.5 Hensel Phelps Construction Co. Inc.

6.1.6 HITT Contracting Inc.

6.1.7 AECOM

6.1.8 Clune Construction Company LP

6.1.9 Nabholz Construction Corporation

6.1.10 Turner Construction Co. (HOCHTIEF)

7. INVESTMENT ANALYSIS

8. FUTURE OF THE MARKET

US Data Center Construction Industry Segmentation

The US data center construction market study tracks and analyses the revenue generated by the initial cost of infrastructure such as electrical infrastructure, mechanical infrastructure, and general construction that are being used by various end users within country tiers. The study also analyses the overall impact of the COVID-19 pandemic on the ecosystem. The study includes qualitative coverage of the most adopted strategies and analysis of the key base indicators in emerging markets.

The study is segmented by infrastructure (electrical infrastructure (UPS systems, and other electrical infrastructure), mechanical infrastructure (cooling systems, racks, and other mechanical infrastructure), and general construction), tier type (tier-I and II, tier-III, and tier-IV), and end-user (banking, financial services, and insurance, IT and telecommunications, government and defense, healthcare, and other end users). The analysis is based on the market insights captured through secondary research and the primaries. The report tracks the key market parameters, the underlying growth influencers, and the major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

| By Infrastructure | |||||

| |||||

| |||||

| General Construction |

| By Tier Type | |

| Tier-I and -II | |

| Tier-III | |

| Tier-IV |

| By End User | |

| Banking, Financial Services, and Insurance | |

| IT and Telecommunications | |

| Government and Defense | |

| Healthcare | |

| Other End Users |

US Data Center Construction Market Research FAQs

How big is the US Data Center Construction Market?

The US Data Center Construction Market size is expected to reach USD 23.29 billion in 2023 and grow at a CAGR of 5.74% to reach USD 30.79 billion by 2028.

What is the current US Data Center Construction Market size?

In 2023, the US Data Center Construction Market size is expected to reach USD 23.29 billion.

Who are the key players in US Data Center Construction Market?

IBM Corporation, Schneider Electric SE, DPR Construction Inc., Fortis Construction Inc. and Hensel Phelps Construction Co. Inc. are the major companies operating in the US Data Center Construction Market.

US Data Center Construction Industry Report

Statistics for the 2023 US Data Center Construction market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. US Data Center Construction analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.