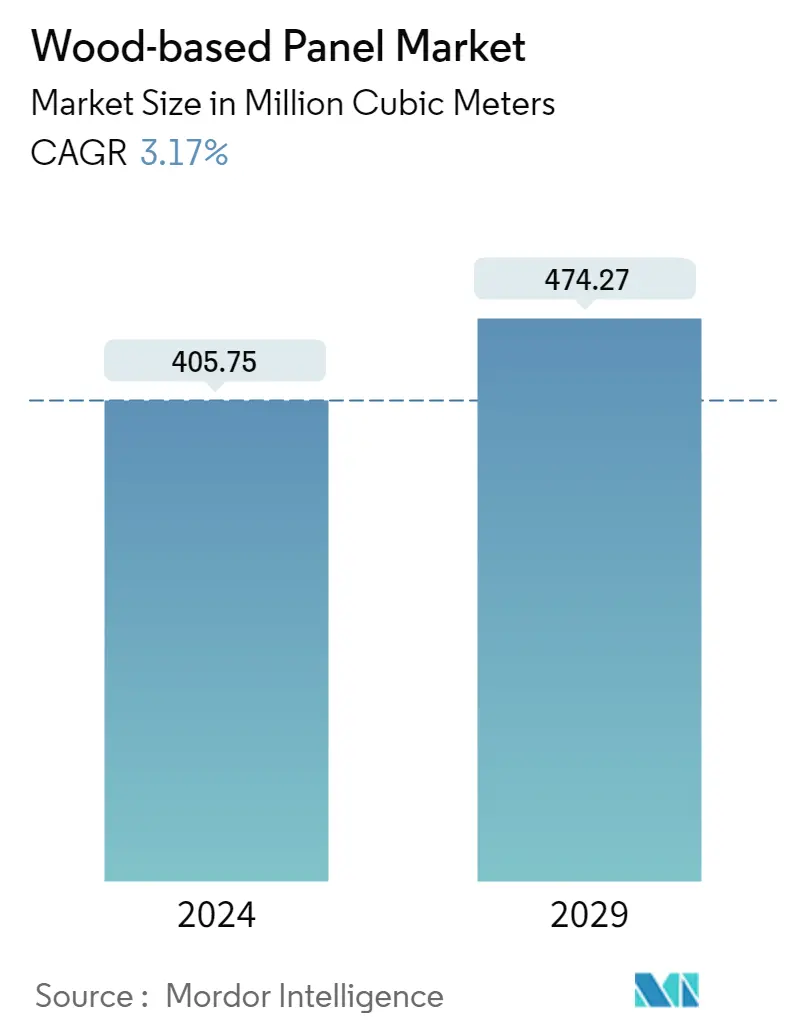

Wood Based Panel Market Size

| Study Period | 2018 - 2028 |

| Market Volume (2023) | 393.28 Million cubic meters |

| Market Volume (2028) | 459.70 Million cubic meters |

| CAGR (2023 - 2028) | 3.17 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Wood Based Panel Market Analysis

The Global Wood Based Panel Market size is expected to grow from 393.28 million cubic meters in 2023 to 459.70 million cubic meters by 2028, at a CAGR of 3.17% during the forecast period (2023-2028).

The market was negatively impacted by COVID-19 in 2020. Several countries imposed anti-dumping duty on the import of a certain variety of fiberboard used in furniture in order to aid domestic producers. All the construction work and other activities were put on hold to curb the spreading of the virus, thereby negatively affecting the market. However, the market is projected to grow steadily, owing to increased building and construction activities in 2021.

- Over the short term, bullish growth trends in residential and commercial construction, coupled with increasing demand from the furniture industry, are major factors driving the growth of the market studied.

- However, formaldehyde emission from wood-based panels is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the increasing application of OSB in structural insulated panels (SIPS) is likely to create lucrative growth opportunities for the global market soon.

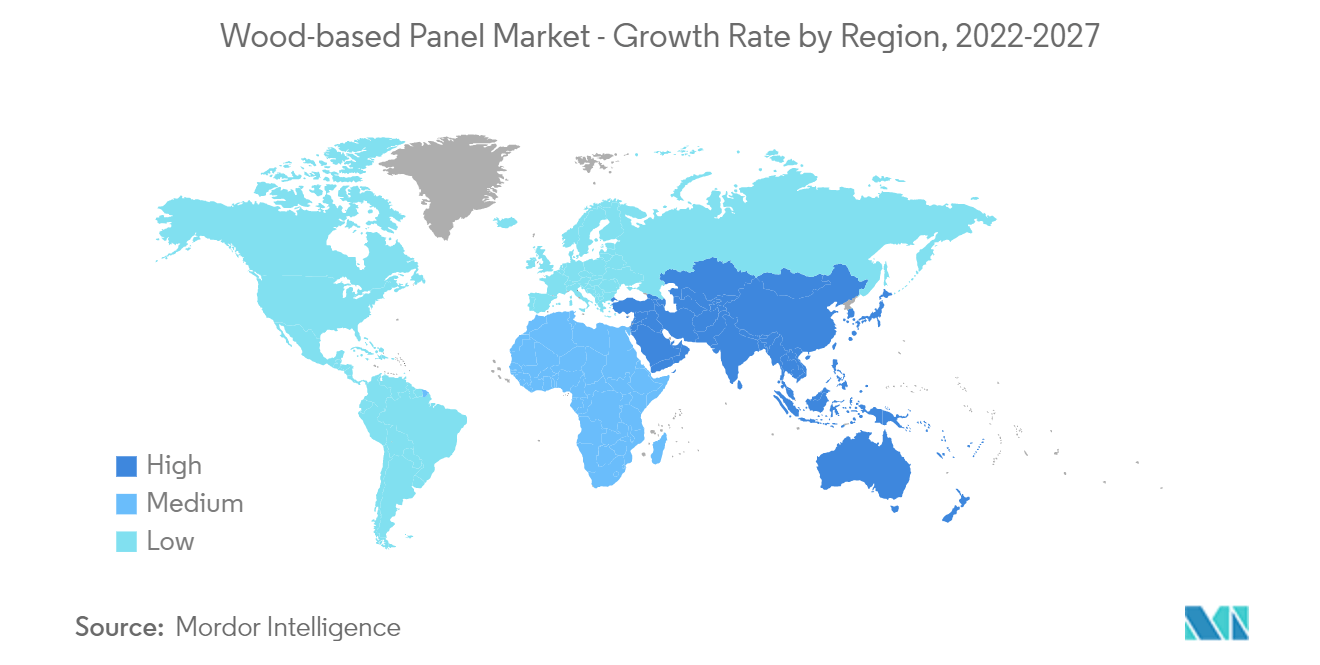

- Asia-Pacific is estimated to witness healthy growth over the assessment period in the wood-based panel market due to the wide usage of wood-based panels in end-use application segments, such as furniture, construction, and packaging, due to their desirable properties.

Wood Based Panel Market Trends

This section covers the major market trends shaping the Wood-based Panel Market according to our research experts:

Increasing Demand from the Furniture Industry

- Due to their several benefits, wood-based panels are extensively used in residential furniture. There are various alternatives to wooden furniture, but the demand for it is still at its peak. Wooden panels are long-lasting, economically friendly, easy-to-clean, and highly versatile.

- The global furniture market comprises 65% of domestic home furniture, followed by commercials (including offices, hotels, and others). Asia-Pacific is the world's largest home furniture producer, among which China, India, Japan, and others are the leading producers.

- China is the leading producer of the home furniture segment globally. As a result of urbanization, new brands have emerged in the Chinese furniture industry. Their most dedicated customers are younger people, who are more likely to adopt new trends and have tremendous purchasing power. Moreover, the growing technological advancement in the country has bought up a new generation in the furniture industry. In 2020, IKEA partnered with the Chinese e-commerce giant Alibaba to open up virtual stores on Alibaba's website. This is an extremely smart market move because the virtual store allows the Swedish furniture company to reach more consumers and experiment with a new manner of promoting their products.

- The Indian furniture industry's largest segment is the home furniture. Bedroom furniture has the highest share of the Indian home furniture market, followed by living room furniture. However, wardrobes and kitchens are the most expensive purchases, with customers spending around USD 7,000-10,000 on kitchen furniture.

- The European home furniture industry is heavily dependent on products imported from Asian countries, and recent supply chain interruptions complicate their sourcing strategies. As a result, retailers have increased their share of imports from neighboring countries compared to Asian countries to reduce transportation costs and delivery times.

- In October 2022, MoKo Home + Living raised USD 6.5 billion Series B debt-equity funding round, co-led by US-based investment fund Talanton and Swiss investor AlphaMundi Group. The aim is to increase home furniture production and maintain good quality. This initiative has driven the growth of the home furniture segment in the country.

- The ongoing working pattern, such as working from home, has increased the demand for compact, durable, and easy-to-handle home furniture. The shift from office workspaces to house settings has increased the demand for more functional and flexible home furniture. Several manufacturers have started offering efficient furniture using wood panels. Whether it is an ergonomic chair, office desk, and study table, working from home is putting the focus back on home décor, resulting in an increase in the furniture segment.

- All the above factors are expected to drive the market for wood-based panels in the coming years.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the global market share. With growing construction activities and the increasing demand for furniture in countries such as China, India, and Japan, the demand for wood-based panels is increasing in the region.

- According to the China Timber and Wood Products Distribution Association, China was the largest wood-based panel producer, with annual production accounting for around 315 million cubic meters last year. Out of the total, plywood production accounted for the largest share of the country's total wood-based panel production, with a production value of 201 million cubic meters. Furthermore, last year, fiberboard and particleboard production accounted for 63 million cubic meters and 33 million cubic meters, respectively.

- China's wood-based paneling production is concentrated in the Shandong, Jiangsu, and Guangxi provinces, which account for about 60% of the total production. According to the China Timber and Wood Products Distribution Association, around 44% of China's wood-based panels were used for furniture manufacturing, decoration, or renovation last year.

- China is amid a construction mega-boom. According to the National Bureau of Statistics of China, the construction works output value in the country increased from CNY 23.27 trillion (USD 3.16 trillion) in 2020 to CNY 25.92 trillion (USD 4.02 trillion) in 2021. Furthermore, China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for wood-based panels.

- Furthermore, according to the Department of Commerce (India), the export value of plywood and its products from India accounted for USD 1,152.04 million in FY 2021, compared to USD 1,086.88 million in FY 2020.

- Moreover, information technology (IT) continues to drive the demand for office spaces, with a 49.2% share of total leasing last year. Banking, financial services, and insurance (BFSI) accounted for a 15.2% share of the overall office space market, witnessing a growth rate of about 3% compared to 2020.

- The Make in India initiative by the government attracted several multinational companies to invest in the country, which is likely to increase the demand for new office buildings in the estimated time, supporting the demand for various wood-based panels, such as particle boards for furniture production.

- India's huge construction sector is expected to become the world's third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project and Housing For All by 2022, are expected to bring the needed impetus to the slowing construction industry.

- The aforementioned factors are contributing to the increasing demand for wood-based panel consumption in the region during the forecast period.

Wood Based Panel Industry Overview

The wood-based panel market is highly fragmented in nature. The major players include Kronoplus Limited, West Frazer, ARAUCO, EGGER Group, and Kastamonu Entegre.

Wood Based Panel Market Leaders

Kronoplus Limited

West Frazer

ARAUCO

EGGER Group

Kastamonu Entegre

*Disclaimer: Major Players sorted in no particular order

Wood Based Panel Market News

- In September 2022, LP Building Solutions completed a million-dollar conversion and expansion project to produce LP SmartSide Trim and Siding products at its New Limerick, Maine facility.

- In June 2022, Kronoplus invested EUR 400 million (USD 473.26 million) to build a new manufacturing facility for wood-based panels with a planned production of 720,000 m³/year covering 25 hectares in Tortosa.

Wood Based Panel Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Bullish Growth Trends in Residential and Commercial Construction

4.1.2 Increasing Demand from the Furniture Industry

4.2 Restraints

4.2.1 Formaldehyde Emission from Wood-based Panels

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

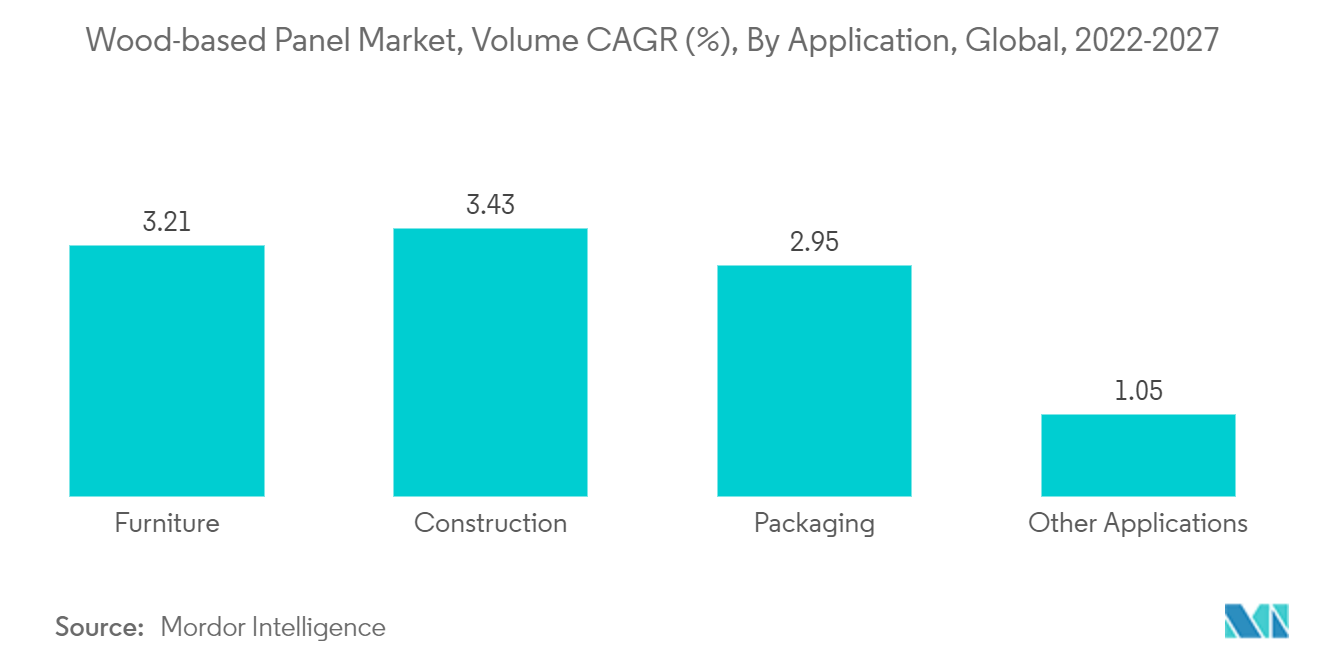

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Medium-Density Fiberboard (MDF)/High-Density Fiberboard (HDF)

5.1.2 Oriented Strand Board (OSB)

5.1.3 Particleboard

5.1.4 Hardboard

5.1.5 Plywood

5.1.6 Other Product Types

5.2 Application

5.2.1 Furniture

5.2.1.1 Residential

5.2.1.2 Commercial

5.2.2 Construction

5.2.2.1 Floor and Roof

5.2.2.2 Wall

5.2.2.3 Door

5.2.2.4 Other Constructions

5.2.3 Packaging

5.2.4 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East & Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East & Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 ARAUCO

6.4.2 CenturyPly

6.4.3 Dongwha Group

6.4.4 Dexco SA

6.4.5 Egger Group

6.4.6 Georgia-Pacific

6.4.7 Green panel Industries Ltd

6.4.8 Kastamonu Entegre

6.4.9 Kronoplus Limited

6.4.10 Langboard Inc.

6.4.11 Louisiana-Pacific Corporation

6.4.12 Pfleiderer

6.4.13 Roseburg Forest Products

6.4.14 Swiss Krono Group

6.4.15 West Fraser

6.4.16 Weyerhaeuser Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Application of OSB in Structural Insulated Panels (SIPS)

Wood Based Panel Industry Segmentation

Wood-based panels are a general term for a variety of different board products having an impressive range of engineering properties. Some of the major types of wood-based panels include plywood, fibreboard, and particleboard. The wood-based panel market is segmented by product type, application, and geography. By product type, the market is segmented into medium-density fiberboard (MDF)/high-density fiberboard (HDF), oriented strand board (OSB), particleboard, hardboard, plywood, and other product types. By application, the market is segmented into furniture, construction, packaging, and other applications. The report also covers the market size and forecasts for the wood-based panel market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (million cubic meters).

| Product Type | |

| Medium-Density Fiberboard (MDF)/High-Density Fiberboard (HDF) | |

| Oriented Strand Board (OSB) | |

| Particleboard | |

| Hardboard | |

| Plywood | |

| Other Product Types |

| Application | ||||||

| ||||||

| ||||||

| Packaging | ||||||

| Other Applications |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Wood Based Panel Market Research FAQs

How big is the Wood-based Panel Market?

The Wood-based Panel Market size is expected to reach 393.28 million cubic meters in 2023 and grow at a CAGR of 3.17% to reach 459.70 million cubic meters by 2028.

What is the current Wood-based Panel Market size?

In 2023, the Wood-based Panel Market size is expected to reach 393.28 million cubic meters.

Who are the key players in Wood-based Panel Market?

Kronoplus Limited, West Frazer, ARAUCO, EGGER Group and Kastamonu Entegre are the major companies operating in the Wood-based Panel Market.

Which is the fastest growing region in Wood-based Panel Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Wood-based Panel Market?

In 2023, the Asia Pacific accounts for the largest market share in the Wood-based Panel Market.

Wood Based Panel Industry Report

Statistics for the 2023 Wood Based Panel market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Wood Based Panel analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.