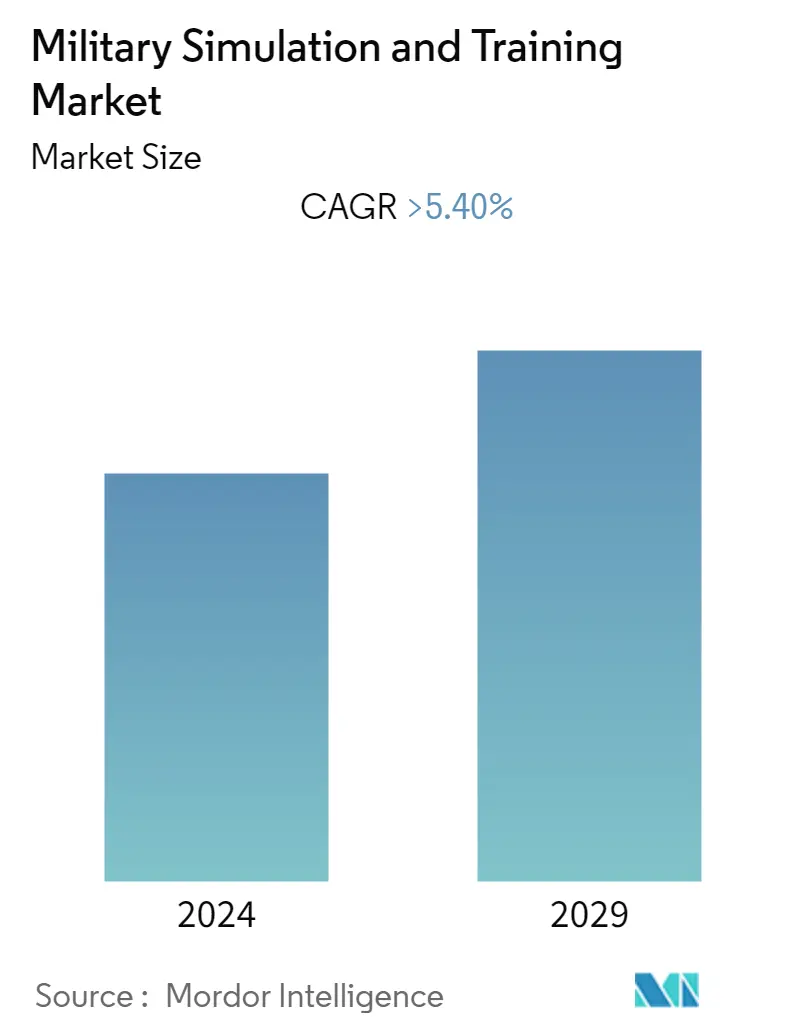

Military Simulation & Training Market Size

| Study Period | 2018 - 2028 |

| Base Year For Estimation | 2021 |

| CAGR | > 5.40 % |

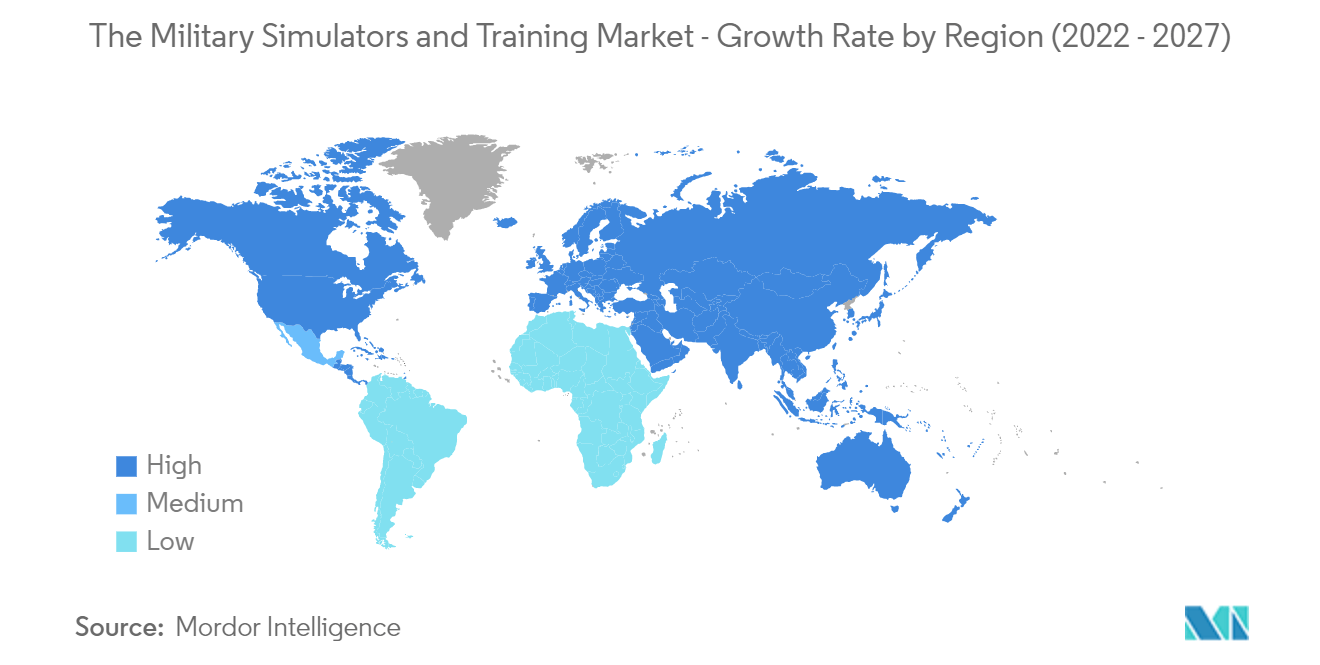

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Military Simulation & Training Market Analysis

The Military Simulators and Training Market is estimated to register a CAGR of more than 5.4% during the forecast period.

Despite the economic impacts of the COVID-19 pandemic, global military spending continued to increase in 2020 and 2021. Global military spending increased by 0.7% to reach USD 2,113 billion in 2021. The continued growth in global defense spending combined with the increased need for skilled forces to successfully navigate and operate various new combat vehicles is expected to propel the growth of the Military Simulators and Training Market during the forecast period.

The growth in demand for military vehicles across the land, sea, and aerial platforms is the primary driver of the market growth. Several countries are modernizing their military fleet by inducting newer generation vehicle platforms, generating a simultaneous demand for simulation-based training for the military personnel on these platforms, thereby propelling the market prospects of the affiliate military simulators.

The training of pilots and military personnel in real aircraft, land vehicles, and ships involves multiple risks and sometimes may lead to hazardous situations and fatalities. Simulators provide a realistic experience and safety training for beginners. This need for safe and efficient training is also driving the simulator market.

Military Simulation & Training Market Trends

This section covers the major market trends shaping the Military Simulation & Training Market according to our research experts:

The Air Segment is Expected to Experience the Highest Growth During the Forecast Period

The Air segment of the market held the largest market share in 2021. The segment is also expected to register the highest CAGR during the forecast period, majorly due to the complexity and risk involved in operating the aircraft compared to the other end users. For example, a single mistake by pilots on board a military aircraft while landing or take-off will cost the lives of people on board and result in the loss of sophisticated military property and compromise the mission. Such complexity has forced the military authorities to incorporate simulator-based training for pilots. Moreover, the increasing adoption of newer aircraft that incorporate complex technologies in the military may require pilots to familiarize themselves with the latest equipment and systems. In such situations, providing hands-on experience may be difficult due to high-cost involvement. In such cases, the simulators act as the preferred option. For instance, the operating cost of the USAF’s F-35A is estimated to be about USD 44,000 per flight hour. In this regard, the F-35 pilots are first trained on simulators instead of the actual aircraft, which helps in cost-cutting. Pilots are typically trained for about 30 hours on the F-35 full-mission simulators before getting airborne on their first sortie in the F-35. Lockheed Martin is also planning to connect full-mission simulators in the United States and the United Kingdom through a software upgrade, allowing the Air Force pilots in these countries to virtually train with one another across international borders. Furthermore, the USAF aims to deploy and connect more full-mission simulators in the years to come. Such initiatives also help the militaries increase interoperability without conducting joint military exercises on actual aircraft. With the interest of the defense departments of major countries in utilizing flight simulator training, the demand for simulators that cater to the needs of aircraft and military pilot training is skyrocketing. As a result, new purchases and product innovations to supply the most advanced military aircraft training activities have been taking place in the market. For instance, Lockheed Martin is planning to connect full-mission simulators- in the United States and the United Kingdom through a software upgrade, allowing the Air Force pilots in these countries to virtually train with one another across international borders. Furthermore, the USAF aims to deploy and connect more full-mission simulators in the years to come. Such initiatives also help the militaries in enhancing interoperability without conducting joint military exercises on actual aircraft, which is expected to drive the market growth during the forecast period.

North America Held the Largest Market Share

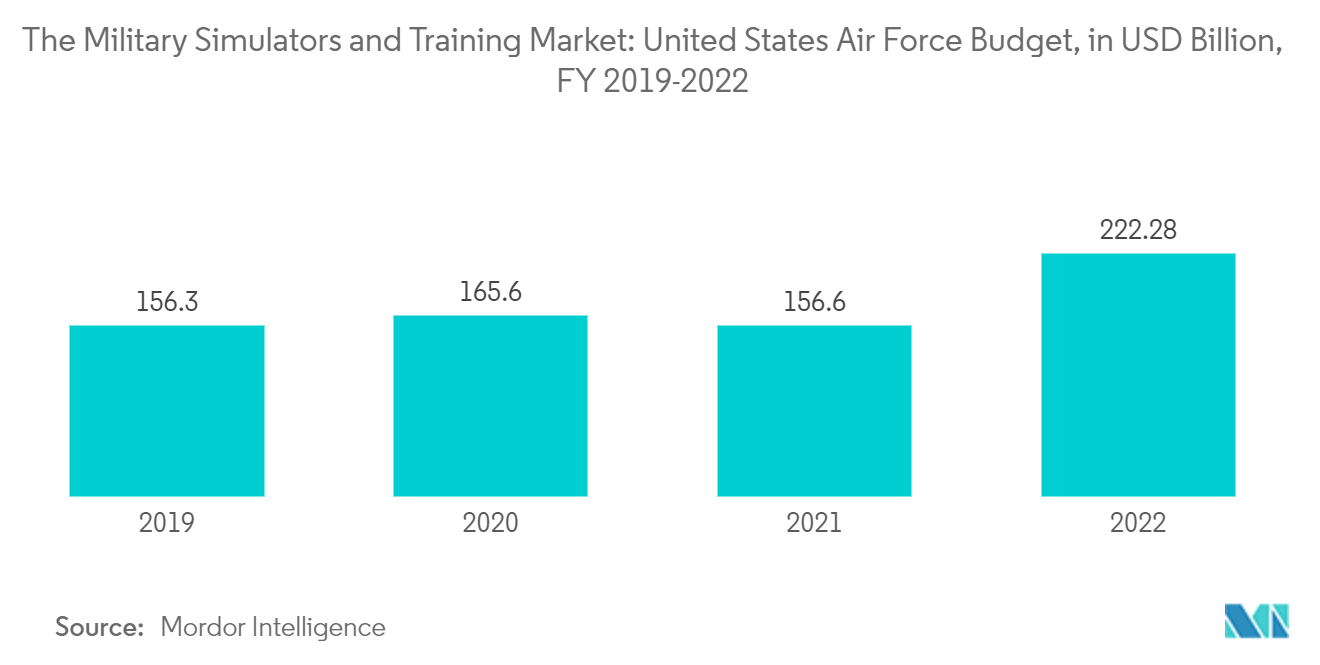

The United States had a total military expenditure of USD 801 Billion in 2021. The Armed Forces of the country are procuring several newer generation military vehicles across the land, air, and sea-based platforms, amidst the ongoing race for technological superiority. Simultaneously, the country is investing in the development and procurement of related simulator solutions, which is expected to drive market growth in the region. Although the US Air Force has been procuring simulators on a large scale for several years, the US Navy is investing heavily in simulation to improve its navigation training, and it budgeted for new integrated bridge simulators to fill the capacity gaps. The efforts to increase ship simulator capacity are further supported by constructing new buildings in San Diego and Norfolk to house multiple simulation facilities. The Royal Canadian Air Force plans to combine two training programs under a single, multibillion-dollar project, the Future Aircrew Training program, or FAcT, where the number of pilots trained annually will increase.

Furthermore, the government of Canada, with plans to implement fire training simulators for military uses, has offered to stand offered to VirTra, Inc. in December 2021. As per the offer, the company is expected to supply advanced military training simulators to the country’s land, marine, and air force divisions of the military. Such developments are expected to drive the growth of the market in the North American region during the forecast period.

Military Simulation & Training Industry Overview

Some of the prominent players in the military simulator market in 2021 were Collins Aerospace (Raytheon Technologies Company), CAE Inc., Rheinmetall AG, FlightSafety International (Berkshire Hathaway Inc.), and Thales Group. Simulator manufacturers are required to build a brand and reach out to geographical extremes to get customers. Manufacturers may have the first-mover advantage if they can attract customers for the simulators for new vehicle platforms, as simulators tend to be reconfigured or upgraded to support newer variants, providing the players to enjoy continuous revenue inflow. Mergers and acquisitions are expected to help the players by increasing their addressable market. For instance, in 2020, CAE announced that it acquired TRU Simulation + Training Canada Inc. Furthermore, in 2021, the company also announced the acquisition of L3Harris Technologies' Military Training business for USD 1.05 billion. Such acquisitions are expected to help the companies expand their market presence and their revenue share in the market during the forecast period. In the coming future, growing demand from end-users is expected to create some intense competitive rivalry where the companies offering the best products for a limited budget, along with other affiliate services, will reap the most benefits.

Military Simulation & Training Market Leaders

Rheinmetall AG

FlightSafety International

Collins Aerospace

CAE Inc.

Thales Group

*Disclaimer: Major Players sorted in no particular order

.webp)

Military Simulation & Training Market News

In April 2021, the United States Army awarded Science Applications International Corp. two major contracts worth a total of more than USD 4 billion for modeling and simulation systems engineering and hardware-in-the-loop development of simulation capabilities for the Aviation & Missile Center.

In January 2021, Top Aces Corp announced that it received the first batch of its F-16 aircraft that are to be used for military air training for the pilots who operate the F-16s

Military Simulation & Training Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porters Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By Platform

5.1.1 Army

5.1.1.1 Armored Tanks

5.1.1.2 Howitzers

5.1.1.3 Other

5.1.2 Naval

5.1.2.1 Naval Vessels

5.1.2.2 Submarines

5.1.2.3 Others

5.1.3 Air

5.1.3.1 Fixed-wing Aircraft

5.1.3.2 Rotary-wing Aircraft

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 United Kingdom

5.2.2.3 France

5.2.2.4 Russia

5.2.2.5 Spain

5.2.2.6 Rest of Europe

5.2.3 Asia Pacific

5.2.3.1 India

5.2.3.2 China

5.2.3.3 Japan

5.2.3.4 South Korea

5.2.3.5 Rest of Asia Pacific

5.2.4 Latin America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.5 Middle East & Africa

5.2.5.1 United Arab Emirates

5.2.5.2 Saudi Arabia

5.2.5.3 South Africa

5.2.5.4 Rest of Middle East & Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share**

6.2 Company Profiles*

6.2.1 CAE Inc.,

6.2.2 FlightSafety International

6.2.3 Lockheed Martin Corporation

6.2.4 Thales Group

6.2.5 TRU Simulation + Training Inc.

6.2.6 BAE Systems PLC

6.2.7 The Boeing Company

6.2.8 Rheinmetall AG

6.2.9 Raytheon Technologies Corporation

6.2.10 Frasca Flight Simulation

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Military Simulation & Training Industry Segmentation

The Military Simulators and Training Market is segmented By Platform (Army (Armored Tanks, Howitzers, and Others), Navy (Naval Vessels, Submarines, and Others), and Air (Fixed-wing Aircraft and Rotor-wing Aircraft) and By Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers market size and forecast for all the above segments in terms of value (USD Million).

| By Platform | |||||

| |||||

| |||||

|

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Military Simulation & Training Market Research FAQs

What is the current Military Simulation and Training Market size?

The Military Simulation and Training Market is projected to register a CAGR of greater than 5.4% during the forecast period (2023-2028).

Who are the key players in Military Simulation and Training Market?

Rheinmetall AG, FlightSafety International, Collins Aerospace, CAE Inc. and Thales Group are the major companies operating in the Military Simulation and Training Market.

Which is the fastest growing region in Military Simulation and Training Market?

North America is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Military Simulation and Training Market?

In 2023, the North America accounts for the largest market share in the Military Simulation and Training Market.

Military Simulation and Training Industry Report

Statistics for the 2023 Military Simulation and Training market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Military Simulation and Training analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.