Market Size of Europe HVAC Industry

| Study Period | 2018 - 2028 |

| Base Year For Estimation | 2021 |

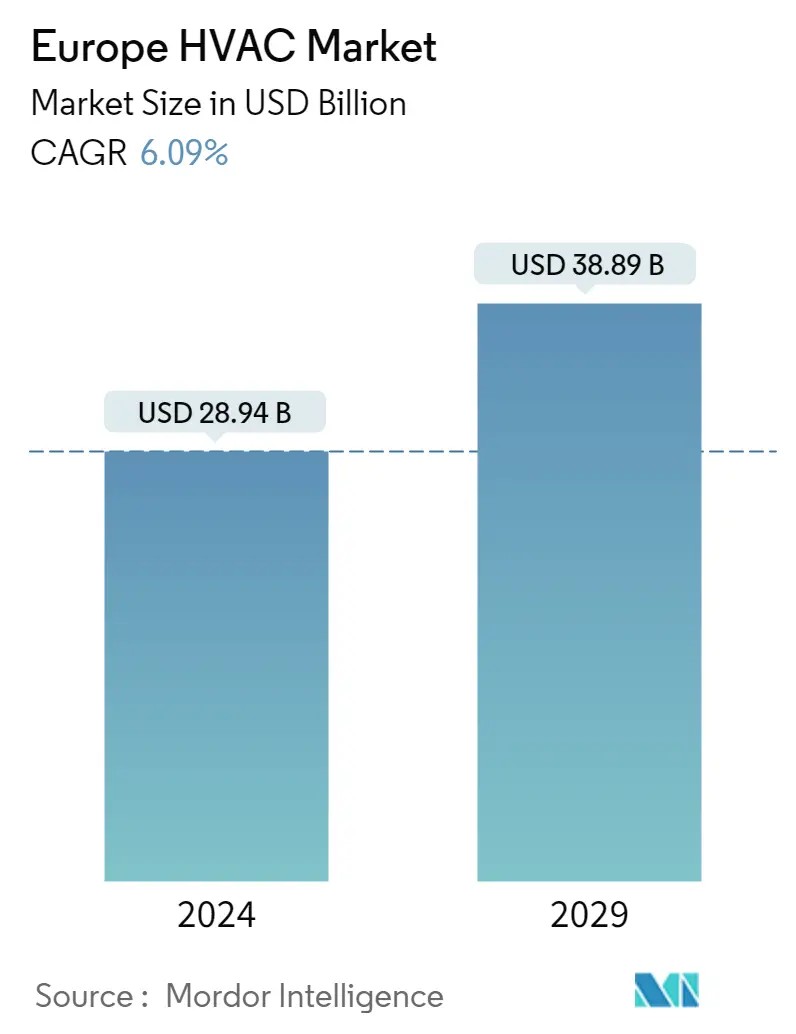

| Market Size (2023) | USD 27.28 Billion |

| Market Size (2028) | USD 36.66 Billion |

| CAGR (2023 - 2028) | 6.09 % |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Europe HVAC Market Analysis

The Europe HVAC Equipment Market size is expected to grow from USD 27.28 billion in 2023 to USD 36.66 billion by 2028, at a CAGR of 6.09% during the forecast period (2023-2028).

- Heating, ventilation, and air conditioning is a mechanical system that provides thermal comfort and indoor air quality while also controlling internal temperatures and regulating internal humidity. Central air conditioners, heat pumps, chillers, and packaged systems are the most common types of systems.

- Heating, ventilation, and air conditioning (HVAC) systems are becoming increasingly popular throughout the EU region owing to their numerous benefits, notably power-saving techniques. The increase in demand for smart systems, as well as the integration of the Internet of Things (IoT), industrial automation systems, smart manufacturing, and Industry 4.0, is driving the growth of the European HVAC equipment market.

- Furthermore, continued urbanization and population growth are essential in increasing the popularity of indoor and outdoor temperature control systems in various parts of Europe. For example, the EU Commission estimates that by January 2022, the EU's population will be 446.8 million people, 172 000 fewer than the previous year, with urban areas housing 85% of the population.

- The replacement of existing equipment with better-performing equipment and supportive government regulations, such as energy-saving incentives through tax credit programs, are driving the United Kingdom HVAC equipment market over the forecast period. For example, the UK government has already set a target of installing 600,000 heat pumps per year by 2028 to reduce the country's reliance on fossil fuels and aid in the fight against global warming.

- Moreover, one of the major factors driving the market in the region is several government initiatives to promote low-carbon heat sources. For example, the UK Department of Business, Energy, and Industrial Strategy awarded a EUR 54 million contract for heat network funding in July 2022, which will support the development of the scheme in London and working that use low-carbon heat sources like heat pumps and energy from waste to warm properties.

- The impact of IoT and smart HVAC systems is another critical technology expected to drive the market in the future. HVAC systems can exchange data with other connected devices thanks to the Internet of Things (IoT) in HVAC technologies. Integrating smart HVAC systems into homes and commercial buildings detects when maintenance is required automatically, preventing customer annoyances that could cause problems.

- Vendors are also focusing on several strategic investments, such as acquisitions, product launches, and expansions, that will drive the market in the future. Carrier, for example, introduced the AquaForce Vision 30KAV with PUREtec refrigerant in March 2022, an R1234ze chiller designed for industrial processes such as pharmaceuticals, food manufacturing, chemicals, plastics, metal industries, and other applications that require ultra-reliable cooling up to -12 degrees Celsius. This demonstrates the demand for chillers in Europe's industrial sectors.

- New EC recommendations to strengthen the F-gas regulation may result in strict reductions in HFC refrigerants and bans on common AC refrigerants in April 2022, negatively impacting the European air conditioning and refrigeration industry. Starting on January 1, 2027, the European Commission wants to ban the use of HFCs with GWPs of 150 or higher in new split system air conditioners and heat pumps with rated capacities up to and including 12kW. Furthermore, beginning January 1, 2027, the recommendations intend to prohibit the use of HFCs in new split systems with power greater than 12kW.

- Because of the high initial cost of HVAC equipment, some customers may be discouraged from purchasing or upgrading their systems. This is especially true for homeowners and small business owners who may have limited budgets and need help to afford the initial costs of a new system.

- The COVID-19 pandemic significantly impacted the HVAC industry, as demand for systems dropped significantly during the first few months due to lockdown restrictions and businesses refraining from investing in new equipment. Many construction projects were halted around the world as a result of the pandemic. Construction activity declines in the commercial, residential, and industrial sectors temporarily dampened demand for HVAC systems.

Europe HVAC Industry Segmentation

HVAC equipment is an indoor and vehicular environment comfort technology that engages in providing thermal comfort and appropriate indoor air quality. It is a critical part present in various residential structures, which include single-family homes, apartment buildings, hotels, and senior living facilities; medium to large industrial and office buildings, such as skyscrapers and hospitals; vehicles, such as cars, trains, airplanes, ships, and submarines, and in marine environments, where safe and healthy building conditions are regulated, concerning temperature and humidity, using fresh air from outdoors.

The Europe HVAC Equipment Market is Segmented By Equipment (Air Conditioning/Ventilation Equipment (Single Splits/Multi-Splits (Ducted and Ductless), VRF, Air Handling Units, Chillers, Fans Coils, Indoor Packaged, and Roof Tops), Heating Equipment (Boilers/Radiators/Furnaces, and Heat Pumps)), End User (Residential, Commercial, and Industrial), and Country. The report offers the market size in value terms in USD million for all the above segments.

| Equipment | |||||||||||

| |||||||||||

|

| End User | |

| Residential | |

| Commercial | |

| Industrial |

| Country | |

| United Kingdom | |

| Italy | |

| Germany | |

| France | |

| Spain | |

| Eastern Europe | |

| Benelux | |

| Nordics | |

| Russia | |

| Turkey | |

| Rest of Europe |

Europe HVAC Market Size Summary

The Europe HVAC market is experiencing substantial growth, with a rising demand for heating, ventilation, and air conditioning systems. This growth is driven by factors such as the increasing popularity of smart systems, the integration of the Internet of Things (IoT), industrial automation systems, smart manufacturing, and Industry 4.0. Further, the continued urbanization and population growth in Europe are also contributing to the surge in demand for indoor and outdoor temperature control systems. Government regulations and initiatives promoting energy-saving and low-carbon heat sources are also propelling the market forward. However, the high initial cost of HVAC equipment and the impact of the COVID-19 pandemic on the construction industry have posed some challenges to the market. Air conditioning equipment is expected to hold a significant market share in the HVAC equipment market due to rising residential and commercial user numbers and government regulations requiring energy-efficient and environmentally friendly equipment. The adoption of heat pumps is also anticipated to drive the heating equipment segment of the market. The market is further stimulated by several strategic investments by vendors, including acquisitions, product launches, and expansions. Despite the challenges posed by new EC recommendations to strengthen the F-gas regulation and the high initial cost of HVAC equipment, the Europe HVAC market continues to thrive and expand.

Explore MoreEurope HVAC Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness: Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Buyers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Assessment of the Impact of COVID-19 on the Industry

-

-

2. MARKET SEGMENTATION

-

2.1 Equipment

-

2.1.1 Air Conditioning/Ventilation Equipment

-

2.1.1.1 Type

-

2.1.1.1.1 Single Splits/Multi-Splits

-

2.1.1.1.2 VRF

-

2.1.1.1.3 Air Handling Units

-

2.1.1.1.4 Chillers

-

2.1.1.1.5 Fans Coils

-

2.1.1.1.6 Indoor Packaged And Roof Tops

-

2.1.1.1.7 Other Types

-

-

-

2.1.2 Heating Equipment

-

2.1.2.1 Type

-

2.1.2.1.1 Boilers/Radiators/Furnace and Other Heaters

-

2.1.2.1.2 Heat Pumps

-

-

-

-

2.2 End User

-

2.2.1 Residential

-

2.2.2 Commercial

-

2.2.3 Industrial

-

-

2.3 Country

-

2.3.1 United Kingdom

-

2.3.2 Italy

-

2.3.3 Germany

-

2.3.4 France

-

2.3.5 Spain

-

2.3.6 Eastern Europe

-

2.3.7 Benelux

-

2.3.8 Nordics

-

2.3.9 Russia

-

2.3.10 Turkey

-

2.3.11 Rest of Europe

-

-

Europe HVAC Market Size FAQs

How big is the Europe HVAC Equipment Market?

The Europe HVAC Equipment Market size is expected to reach USD 27.28 billion in 2023 and grow at a CAGR of 6.09% to reach USD 36.66 billion by 2028.

What is the current Europe HVAC Equipment Market size?

In 2023, the Europe HVAC Equipment Market size is expected to reach USD 27.28 billion.