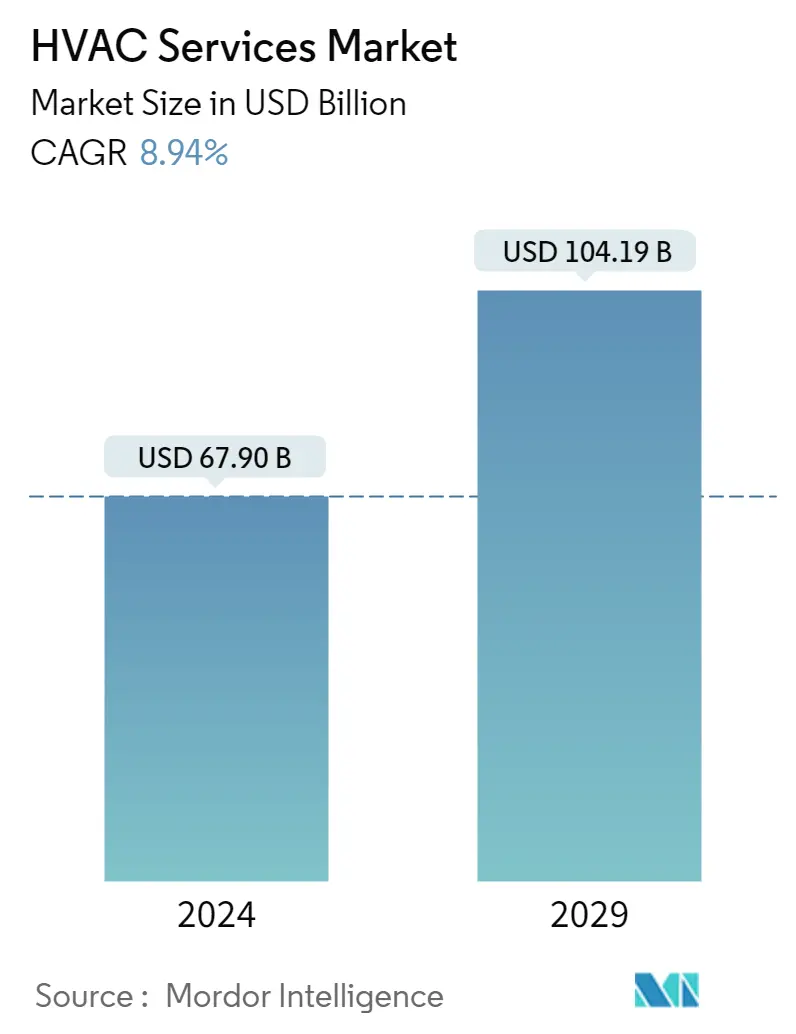

HVAC Market Size

| Study Period | 2017-2027 |

| Market Size (2023) | USD 62.33 Billion |

| Market Size (2028) | USD 95.64 Billion |

| CAGR (2023 - 2028) | 8.94 % |

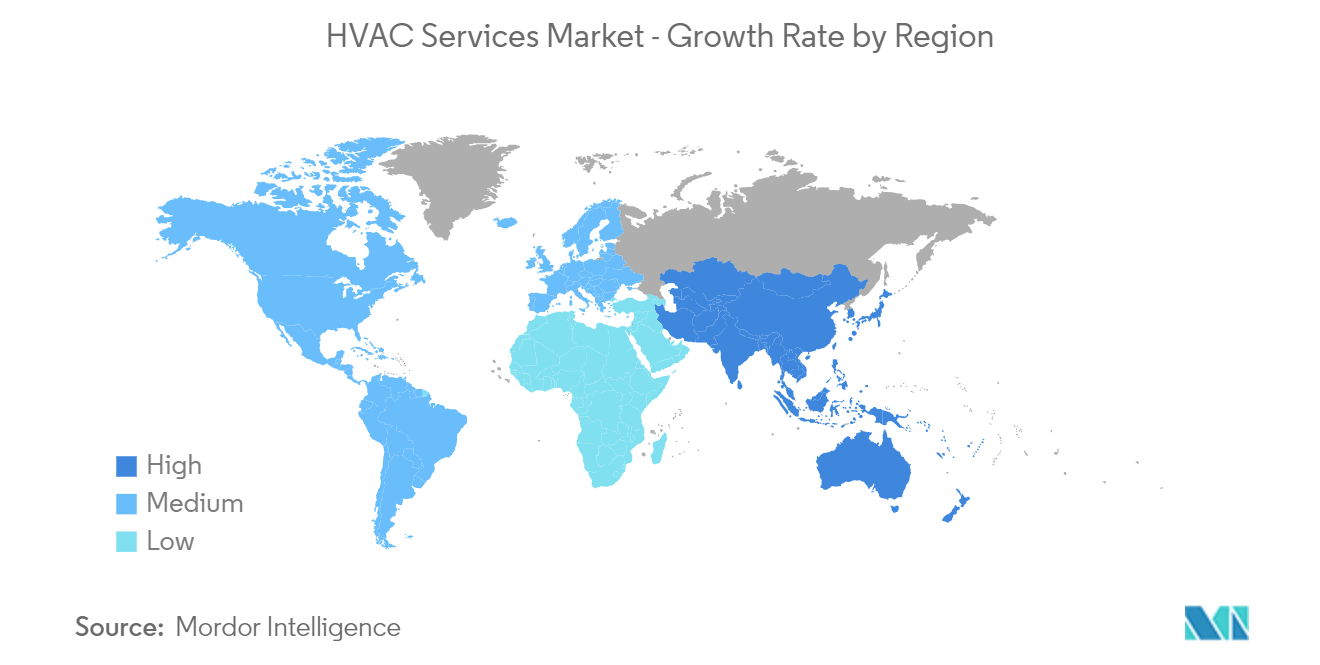

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

HVAC Market Analysis

The HVAC Services Market size is expected to grow from USD 62.33 billion in 2023 to USD 95.64 billion by 2028, at a CAGR of 8.94% during the forecast period (2023-2028).

The growing use of air conditioners in homes and offices is one of the significant drivers stressing the need for HVAC services.

- Technological innovations and climate changes have increased the adoption of HVAC equipment. For instance, in October 2022, 75F Smart Innovations India and Tata Power Trading Company (TPTCL) inked a contract to jointly promote automation and energy-efficient building solutions. Through this partnership, TPTCL and 75F will collaborate to provide solutions for smart building automation and HVAC (heating, ventilation, and air conditioning) optimization powered by advanced technologies like IoT, cloud, and AI/ML.

- Furthermore, the growth in the construction industry and the rising disposable income in developing countries have increased the availability of HVAC equipment for a broader consumer base. For instance, According to the Bureau of Labor Statistics, the construction sector's output in the United States is expected to amount to approximately USD 1.58 trillion by 2028. HVAC services are expected to witness significant market growth, majorly due to the increased need to install and maintain the energy efficiency of the existing systems.

- The growing construction industry in major emerging economies and the expansion of end-user markets, such as the information center market, are influential factors driving the evolution of the HVAC services market over the forecast period. The advantages of using HVAC systems are energy efficiency, improved results, and a longer lifespan. According to British Petroleum (BP) PLC, primary energy consumption in India increased by 10% in 2022, from 32 to 35 exajoule.

- Further, the mixed global climatic circumstances and the vital need to maintain an ambient environment in a building are the key reasons that will positively impact the market over the forecast period. In recent times, intelligent features and higher energy efficiency have been the critical purchase criteria for most customers. The trend is expected to gain traction over the next few years. According to Stratego, co-founded by the Intelligent Energy Europe Programme of the EU, an investment of EUR 50 billion ( ~USD 52.43 billion) from 2010 to 2050 will save enough fuel to reduce the costs of the energy system. As part of this investment, district heating's share stood at EUR 5 billion (~USD 5.24 billion), and individual heat pumps at EUR 15 billion (~USD 15.73 billion).

- Furthermore, any changes in demand for the equipment will further impact the service market positively, as higher demand for new equipment leads to higher installation or retrofitting services. HVAC companies offer a variety of services for both non-commercial and commercial property owners. These services not only give attention to improving the equipment's performance but can also reduce energy costs.

- Furthermore, the European Union is focused on the European green Deal, a directive that aims to reduce energy consumption by 9% by 2030. Such instances favor HVAC manufacturers as governments across Europe have been initiating Tax Credit programs for energy-efficient home improvements. For example, the Italian Revenue agency recently offered Suberbonus a 110% tax deduction for renovations in residential sectors to improve energy efficiencies. This increases the demand for replacing older HVAC equipment with new HVAC equipment in the residential sector.

- With the outbreak of COVID-19, most commercial and industrial construction projects started carried on at a slower pace while some were canceled. Production lines at some HVAC manufacturers had to be put on hold for several weeks, and installers saw their new installation projects limited by sanitary guidelines. However, in European countries such as Italy, AHU sales benefitted from the increased ventilation demand due to COVID-19.

HVAC Market Trends

This section covers the major market trends shaping the HVAC Services Market according to our research experts:

Residential Segment is Expected to Register Significant Growth

- The HVAC services need in the residential sector are mainly due to the growing population in the world, thereby leading to new installations. The market in developed regions, like Europe and North America, is primarily from the maintenance and replacement services. Further, as of October 2022, China's population stood at 1.45 billion, followed by India, with residents of 1.38 billion.

- With rising global temperatures and enhancing living standards, market penetration for A/C systems is expected to grow substantially from current levels in developing nations. Also, amidst the global financial crisis and housing market collapse, an overhang of housing in many mature economies led to a breakdown in the costs of existing homes and stifled the latest residential construction spending.

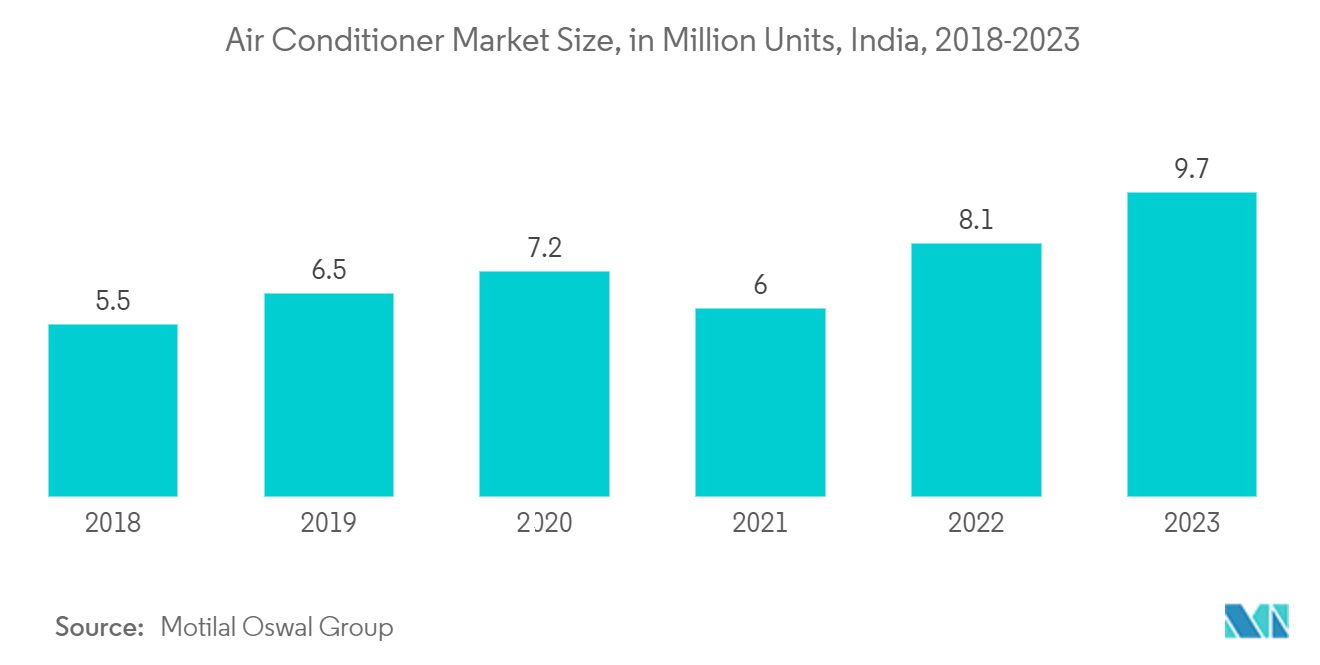

- According to JRAIA, the global demand for room air conditioners has increased to 95.16 million in recent years. Furthermore, according to Motilal Oswal Group, increasing demand for home appliances and a reasonably low penetration rate has left the Indian air conditioner market with plenty of room to grow and is estimated to reach 9.7 million units in the financial year 2023.

- Moreover, investments by the government sector in new building construction and smart infrastructure can also drive the demand for HVAC services. According to the U.S. census bureau, US new home construction in March 2022 was around 68,000 units, or 3.9% higher than in March 2021. Further, 622,000 building permits for multifamily housing units were granted in the United States in 2021, compared with 492,000 over the previous twelve months.

- For instance, in April 2022, Daikin announced its support for the REPowerEU, which has set a goal to boost the rollout of heat pumps from 10 million units in 2027 to 30 million units in 2030. This is further associated with residential decarbonization as the movement can help the European Union achieve the residential sector's decarbonization goals by 2050. Various HVAC services vendors are further supporting such initiatives.

- According to an Aeroseal report, irregular speed heat pumps can reduce monthly homeowner costs by up to 40%. On its own, proper building or home insulation can improve HVAC efficiencies by up to 30%.

United States to Experience Significant Market Growth

- Growing government support, in the form of higher budget allocations, designed to increase homeownership and sustainable community development, and the increasing housing affordability in the country, may contribute to the ever-growing residential construction sector. In addition, increased construction activities, rapid urbanization, infrastructural reforms, and HVAC unit replacements are some of the major factors supporting the growth of the HVAC services market in the country.

- According to IEA, more than 90% of households in the United States have air conditioning equipment, compared to just 8% of the 2.8 billion people living in the hottest parts of the world. The growing use of air conditioners in homes and offices around the U.S. will be one of the top drivers stressing the need for HVAC services in the region.

- Furthermore, brownfield and greenfield opportunities for the new and existing building stock are also anticipated to significantly aid the market growth during the forecast period. Further, the Biden plan to build modern, sustainable infrastructure and an equitable clean energy future to put the United States on an irreversible path to achieve net-zero emissions, economy-wide, by no later than 2050. A large part of the overall Biden plan is to make commercial buildings (especially aging buildings) more energy efficient. The plan calls for an upgrade of 4 million commercial facilities in the United States. Energy efficiency measures touted by the Biden administration as part of their plan include installing LED lighting, electrical appliances, and advanced heating and cooling systems. The plan also comprises investment in “energy upgrades” for homes, offices, warehouses, and public buildings.

- The HVAC Industry is moving towards smart technologies in the United States, as the region is witnessing a high level of IoT integrations. State policies and regulations also govern the demand for HVAC services in the country. For instance, according to Aeroseal, LLC, in the northern U.S., furnaces must have a 90% efficiency rating, but in southern states, only an 80% efficiency rating is required. This indicates that the HVAC services industry tends to be fueled by local and regional regulations.

- According to the US EIA Residential Energy Consumption Survey (RECS), 76 million primarily occupied US homes (64% of the total) use central air-conditioning equipment. Heat pumps are used for heating or cooling in approximately 13 million homes (11%). By 2023, all new residential central air-conditioning and air-source heat pump systems sold in the United States will be demanded to meet new energy efficiency standards, fueling the growth of HVAC services.

HVAC Industry Overview

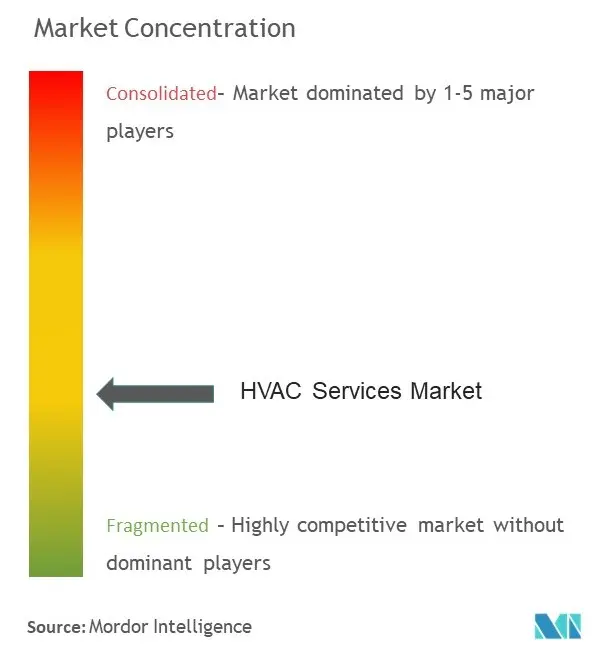

The HVAC services market is favorably competitive and consists of several prominent players. The market performers are focusing on expanding their consumer base across foreign countries. These enterprises leverage strategic collaborative initiatives to boost their market share and profitability. The companies performing in the market are also acquiring start-ups working on HVAC services technologies to strengthen their production capacities.

- January 2022: Daikin Applied introduced SiteLineBuilding Controls, a scalable, cloud-based technology that connects, manages, and monitors individual HVAC equipment and integrated building systems. With the SiteLineBuilding Controls, commercial building owners and operators have the tools and insights to optimize performance, improve indoor air quality, and trim energy use and carbon emissions.

- January 2022: Emerson announced the launch of the next generation of Copeland ZPK7 single (fixed) speed scroll compressors for residential and light commercial HVAC applications, including heat pumps, split air conditioning, packaged systems, rooftops, and geothermal systems.

HVAC Market Leaders

Siemens AG

Honeywell International Inc.

LG Electronics, Inc.

Electrolux AB

Johnson Controls International PLC

*Disclaimer: Major Players sorted in no particular order

HVAC Market News

- October 2022: Ingersoll Rand Inc has agreed to acquire SPX Flow’s Air Treatment business for a purchase price of USD 525 million. The SPX Flow Air Treatment business will join Ingersoll Rand’s Industrial Technologies and Services (IT&S) segment.

- January 2022: Comfort Systems USA Inc. announced the acquisition of MEP Holding Co. and its related subsidiaries, including Indianapolis-based Edwards Electrical & Mechanical, Inc. With this acquisition, the company may establish a robust full-service presence in Indianapolis and provide Comfort Systems USA with exceptional specialized capabilities in clean room solutions to complement its off-site construction and pre-fabrication solutions.

- January 2022: Comfort Systems USA, a leading building and service provider for mechanical, electrical, and plumbing building systems, and XOi Technologies, a method for field service data collection and indexing, announced a partnership to deploy an advanced end-to-end engagement solution better to equip commercial and industrial technicians on the job. Comfort Systems’ FIX solution powered by XOi delivers creative tools and insights, facilitating curb-to-curb technician enablement and engagement from dispatch to job fulfillment.

HVAC Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions & Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Threat of New Entrants

4.2.2 Bargaining Power of Buyers

4.2.3 Bargaining Power of Suppliers

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Construction Business in Major Emerging Economies

5.1.2 Growing Data Center Market

5.2 Market Restraints

5.2.1 Labor Shortage/High Costs of Skilled Labor

6. MARKET SEGMENTATION

6.1 By Implementation Type

6.1.1 New Construction

6.1.2 Retrofit Buildings

6.2 By End User

6.2.1 Residential

6.2.2 Commercial

6.2.3 Industrial

6.3 By Geography

6.3.1 North America

6.3.1.1 United States

6.3.1.2 Canada

6.3.2 Europe

6.3.2.1 United Kingdom

6.3.2.2 Germany

6.3.2.3 France

6.3.2.4 Benelux

6.3.2.5 Rest of Europe

6.3.3 Asia-Pacific

6.3.3.1 China

6.3.3.2 India

6.3.3.3 Japan

6.3.3.4 Rest of Asia-Pacific

6.3.4 Latin America

6.3.4.1 Brazil

6.3.4.2 Argentina

6.3.4.3 Mexico

6.3.4.4 Rest of Latin America

6.3.5 Middle East and Africa

6.3.5.1 United Arab Emirates

6.3.5.2 Saudi Arabia

6.3.5.3 South Africa

6.3.5.4 Rest of Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Siemens AG

7.1.2 Honeywell International Inc.

7.1.3 LG Electronics Inc.

7.1.4 Electrolux AB

7.1.5 Johnson Controls International PLC

7.1.6 Lennox International Inc.

7.1.7 Fujitsu General Ltd

7.1.8 Robert Bosch GmbH

7.1.9 Ingersoll-Rand PLC

7.1.10 Carrier Corporation

7.1.11 Daikin Industries Ltd.

7.1.12 Nortek Global HVAC

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

HVAC Industry Segmentation

HVAC services include the construction, installing, and servicing of heating, cooling, and ventilation systems and equipment. HVAC services regulate the temperature inside a building using heating or cooling systems, wall and ceiling ducting, or other HVAC technologies.

The market is segmented by implementation type, such as new construction and retrofit building, end users industries, such as residential, commercial, and industrial, and geography. The impact of COVID-19 on the market and impacted segments are also covered under the scope of the study. Further, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Implementation Type | |

| New Construction | |

| Retrofit Buildings |

| By End User | |

| Residential | |

| Commercial | |

| Industrial |

| By Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

HVAC Market Research FAQs

How big is the HVAC Services Market?

The HVAC Services Market size is expected to reach USD 62.33 billion in 2023 and grow at a CAGR of 8.94% to reach USD 95.64 billion by 2028.

What is the current HVAC Services Market size?

In 2023, the HVAC Services Market size is expected to reach USD 62.33 billion.

Who are the key players in HVAC Services Market?

Siemens AG, Honeywell International Inc., LG Electronics, Inc., Electrolux AB and Johnson Controls International PLC are the major companies operating in the HVAC Services Market.

Which is the fastest growing region in HVAC Services Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2027).

Which region has the biggest share in HVAC Services Market?

In 2023, the North America accounts for the largest market share in the HVAC Services Market.

HVAC Industry Report

Statistics for the 2023 HVAC market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. HVAC analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.