Market Size of HVAC Services Industry

| Study Period | 2017-2027 |

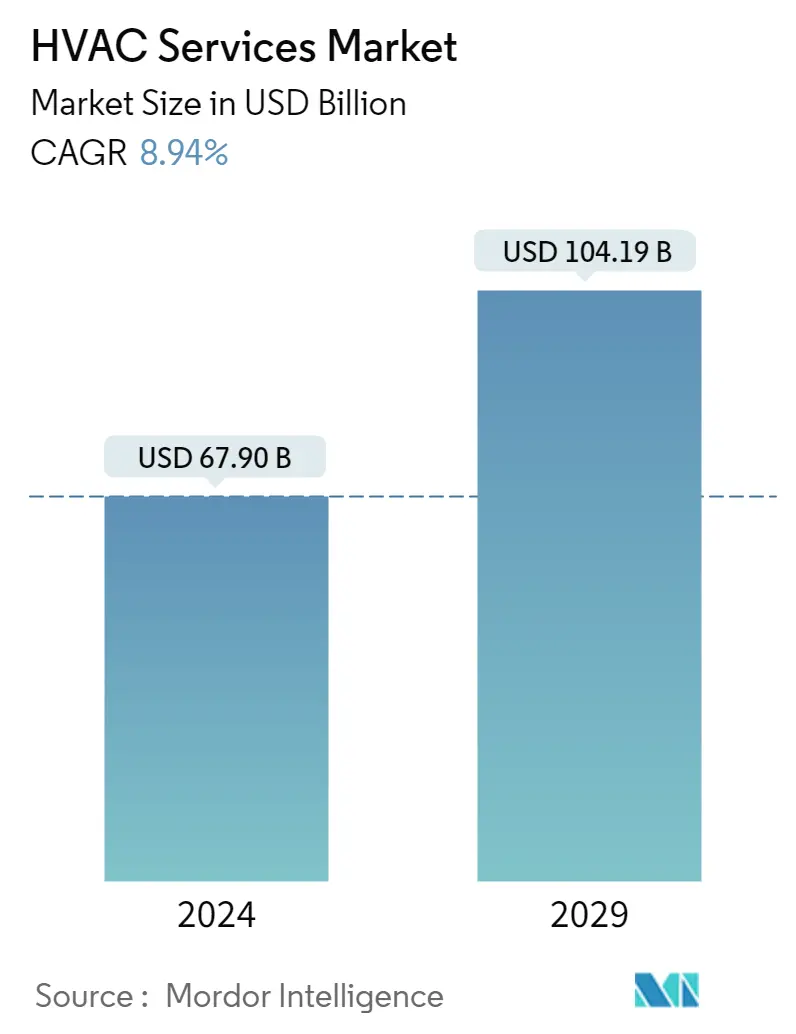

| Market Size (2023) | USD 62.33 Billion |

| Market Size (2028) | USD 95.64 Billion |

| CAGR (2023 - 2028) | 8.94 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

HVAC Market Analysis

The HVAC Services Market size is expected to grow from USD 62.33 billion in 2023 to USD 95.64 billion by 2028, at a CAGR of 8.94% during the forecast period (2023-2028).

The growing use of air conditioners in homes and offices is one of the significant drivers stressing the need for HVAC services.

- Technological innovations and climate changes have increased the adoption of HVAC equipment. For instance, in October 2022, 75F Smart Innovations India and Tata Power Trading Company (TPTCL) inked a contract to jointly promote automation and energy-efficient building solutions. Through this partnership, TPTCL and 75F will collaborate to provide solutions for smart building automation and HVAC (heating, ventilation, and air conditioning) optimization powered by advanced technologies like IoT, cloud, and AI/ML.

- Furthermore, the growth in the construction industry and the rising disposable income in developing countries have increased the availability of HVAC equipment for a broader consumer base. For instance, According to the Bureau of Labor Statistics, the construction sector's output in the United States is expected to amount to approximately USD 1.58 trillion by 2028. HVAC services are expected to witness significant market growth, majorly due to the increased need to install and maintain the energy efficiency of the existing systems.

- The growing construction industry in major emerging economies and the expansion of end-user markets, such as the information center market, are influential factors driving the evolution of the HVAC services market over the forecast period. The advantages of using HVAC systems are energy efficiency, improved results, and a longer lifespan. According to British Petroleum (BP) PLC, primary energy consumption in India increased by 10% in 2022, from 32 to 35 exajoule.

- Further, the mixed global climatic circumstances and the vital need to maintain an ambient environment in a building are the key reasons that will positively impact the market over the forecast period. In recent times, intelligent features and higher energy efficiency have been the critical purchase criteria for most customers. The trend is expected to gain traction over the next few years. According to Stratego, co-founded by the Intelligent Energy Europe Programme of the EU, an investment of EUR 50 billion ( ~USD 52.43 billion) from 2010 to 2050 will save enough fuel to reduce the costs of the energy system. As part of this investment, district heating's share stood at EUR 5 billion (~USD 5.24 billion), and individual heat pumps at EUR 15 billion (~USD 15.73 billion).

- Furthermore, any changes in demand for the equipment will further impact the service market positively, as higher demand for new equipment leads to higher installation or retrofitting services. HVAC companies offer a variety of services for both non-commercial and commercial property owners. These services not only give attention to improving the equipment's performance but can also reduce energy costs.

- Furthermore, the European Union is focused on the European green Deal, a directive that aims to reduce energy consumption by 9% by 2030. Such instances favor HVAC manufacturers as governments across Europe have been initiating Tax Credit programs for energy-efficient home improvements. For example, the Italian Revenue agency recently offered Suberbonus a 110% tax deduction for renovations in residential sectors to improve energy efficiencies. This increases the demand for replacing older HVAC equipment with new HVAC equipment in the residential sector.

- With the outbreak of COVID-19, most commercial and industrial construction projects started carried on at a slower pace while some were canceled. Production lines at some HVAC manufacturers had to be put on hold for several weeks, and installers saw their new installation projects limited by sanitary guidelines. However, in European countries such as Italy, AHU sales benefitted from the increased ventilation demand due to COVID-19.