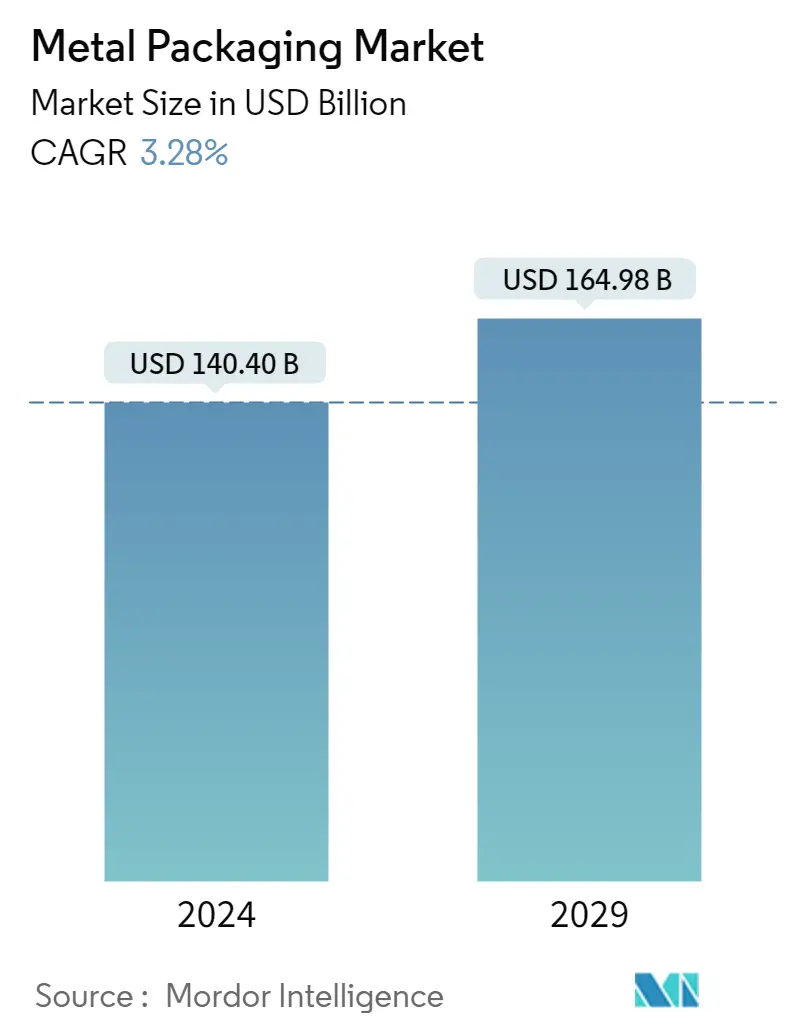

Metal Packaging Market Size

| Study Period | 2018 - 2028 |

| Market Size (2023) | USD 135.94 Billion |

| Market Size (2028) | USD 159.74 Billion |

| CAGR (2023 - 2028) | 3.28 % |

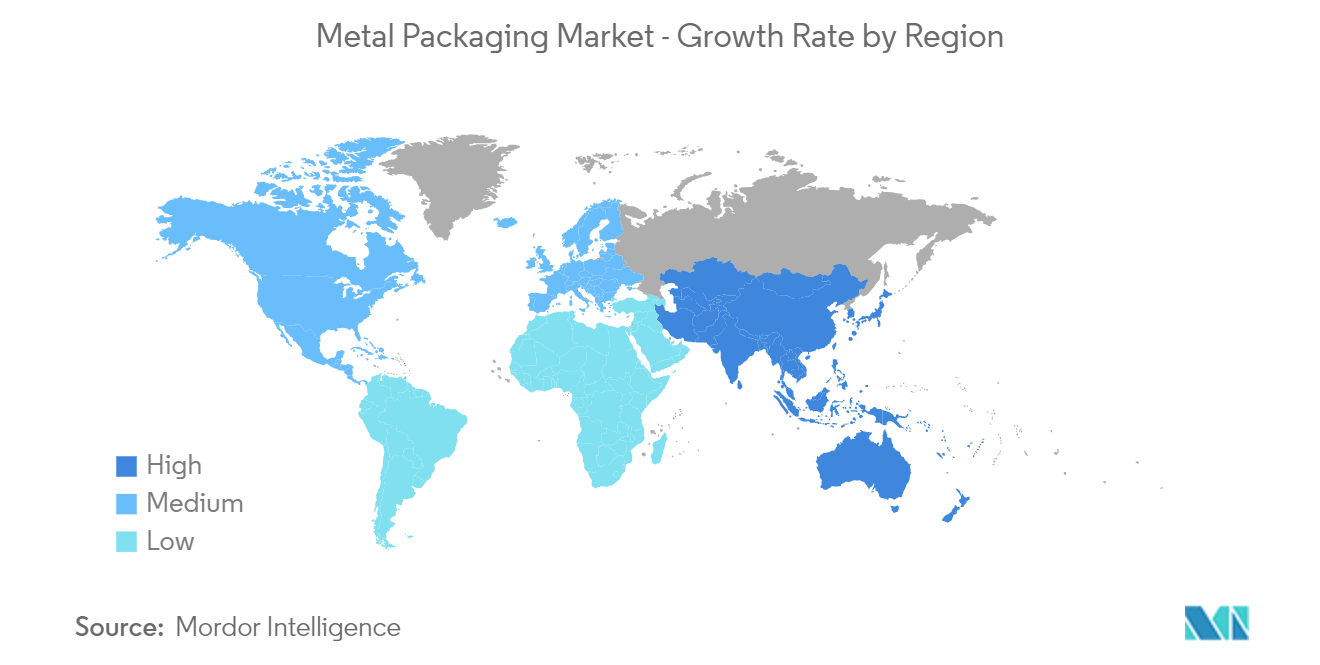

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Metal Packaging Market Analysis

The Metal Packaging Market size is expected to grow from USD 135.94 billion in 2023 to USD 159.74 billion by 2028, at a CAGR of 3.28% during the forecast period (2023-2028).

- Metal packaging is made mainly of steel, aluminum, and metal. Key benefits of metal packaging include impact resistance, the capacity to withstand severe temperatures, convenience for long-distance shipping, and others. There is a high demand for canned food, particularly in busy urban areas; therefore, the product's rising appeal for this usage encourages consumption. The product's durability and ability to withstand high pressure make it a popular choice in the fragrance industry. Metal-based packaging is also growing as luxury goods like cookies, coffee, tea, and other commodities become increasingly popular in metal packaging.

- Consumer products, cosmetics, healthcare, food & beverage, and other end-use industries rely on metal packaging. Over the anticipated period, the market is expected to increase significantly due to these end-use industries' phenomenal growth. The demand for metal packaging is also influenced by a wide range of other factors, including rising consumer demand for convenience packaging, rising health consciousness, rising "on-the-go" lifestyle trend, rising need for brand enhancement and differentiation in an environment of greater competition, and increasing environmental awareness. Due to this, businesses have adopted new package recycling regulations. The demand for metal packaging is primarily driven by customers' increasing health consciousness.

- Metal packaging is also finding extensive application in the food and beverage industry, as it is suitable for protecting food content, ensuring a longer shelf life than most other packaging solutions. In contrast, heavy-duty metal containers transport oil, chemicals, and liquids, such as drums and IBCs (Intermediate bulk containers). According to the United Nations, the world is urbanizing rapidly; the proportion of people living in urban areas is expected to increase to 66% by 2050. As urbanization is picking up and rising affluence, diet is changing, characterized by a high demand for packaged food. Additionally, excellent preservative properties and structural integrity of the various metal product types, offering higher shelf life, have increased the usage of metal packaging in the food packaging industry.

- In addition, the recyclability of metal packaging is one of the critical elements expected to drive the worldwide metal packaging market over the figure period. Because of the prevalent reusing foundation, aluminum and steel packaging materials are the two most active unrefined components for packaging. Most businesses in Europe and North America prefer to advertise that their products are packed with environmentally friendly materials.

- Moreover, ready or on-the-go meals have also witnessed a steady demand for convenience, especially among consumers with busy lifestyles. Therefore, large organized retailers have started to stack vast canned food and beverages. Nowadays, offline and online retailers stock a wide range of brands of packaged food items in their stores. Metal packaging is suited as containers for beverages as they are easy to cool, great for keeping the contents fresh, and prevent breakages when on the go due to the material's strength.

- Metal packaging faces high competition from alternative packaging solutions. Plastic and glass packaging solutions are the alternative packaging options available in the industry. Also, the increasing importance of e-commerce in Europe is expected to influence the overall packaging industry.

- Consumers have high bargaining leverage in the cosmetics and personal care industry. This is owing to increased competition and the availability of cosmetics from different manufacturers. Because these products are highly substitutable, consumers buying competitors' products can force manufacturers to lower their product prices which is a significant limitation for the aerosol cans market. With increased energy prices, supply chain disruptions during COVID-19 affected the growth of the aluminum industry.

- The war between Russia and Ukraine has resulted in economic sanctions against several countries, high commodity prices, supply chain disruptions, and impacts on many markets worldwide, and caused trade disruptions in the industry. War pushed European aluminum companies to cut production, leading to metal shortages. Commodity traders are competing for scarce profits from shipping aluminum from China as the war in Ukraine has created severe shortages for European manufacturers who rely on Russian supplies. Europe has experienced a surge in energy costs.

Metal Packaging Market Trends

Cans are Expected to Hold a Significant Share

- Metal cans provide many benefits, such as rigidity, stability, and high barrier properties, due to which they are used to store goods that have a longer shelf life and can be transported for longer distances. In Europe, metal cans of tin, steel, and aluminum are preferred. These materials have significant properties, such as being softer and lightweight, so manufacturers can save logistics costs.

- Food packaging in the country has witnessed many innovations since the rise of metal packages. Industrialization has proved to be one of the driving forces behind metal being the first choice of material for the mass commercialization of food products. The food packaging industry has used various materials over the past century, but metals like aluminum have gained the most widespread favor owing to reliable strength and sustainability. Metal cans make the most sense for long-term food storage.

- Young customers are particularly drawn to the bold, vibrant 360-degree designs that have become synonymous with craft beer. The change in consumer perception around the alcoholic can as a premium product for great tasting drinks has impacted growth; also, its overall experience fits in with today’s lifestyle. Metal Can alcoholic beverages expanded in popularity among customers since cans are more convenient, portable, and travel-friendly. Furthermore, as compared to glass bottles, metal cans are less expensive and have a much greater recycling rate.

- Consumption of personal care and manufacturing items has increased in recent years, and it is now more widely available due to its practical packaging solution. Aerosol cans are one of the most effective packaging alternatives, offering excellent performance during storage, transportation, and consumer convenience. With the expansion of the personal care & cosmetics industry globally, the demand for eco-friendly packaging cans has surged. As personal care and cosmetic products have sensitive chemical ingredients that are reactive to sun exposure and air, they are packed in aerosol cans specifically.

- Aluminum cans have a higher recycling rate and more recycled content than competing package types. According to the Aluminum Association, it’s one of the most recycled materials on the market. In April 2022, Ball Corporation partnered with Recycle Aerosol LLC to boost the recycling rates of aluminum aerosol cans in the United States; the collaboration not only increases aerosol can recycling but also establishes a closed-loop system in which used cans are recycled into new aerosol cans. The production of aluminum goods from recycled aluminum is energy- and carbon-efficient. Because the alloys used to make aluminum aerosols are of such high purity, there are efficiency improvements that also lessen the demand for virgin aluminum when they are mainly derived from recycled aluminum aerosol bottles and cans.

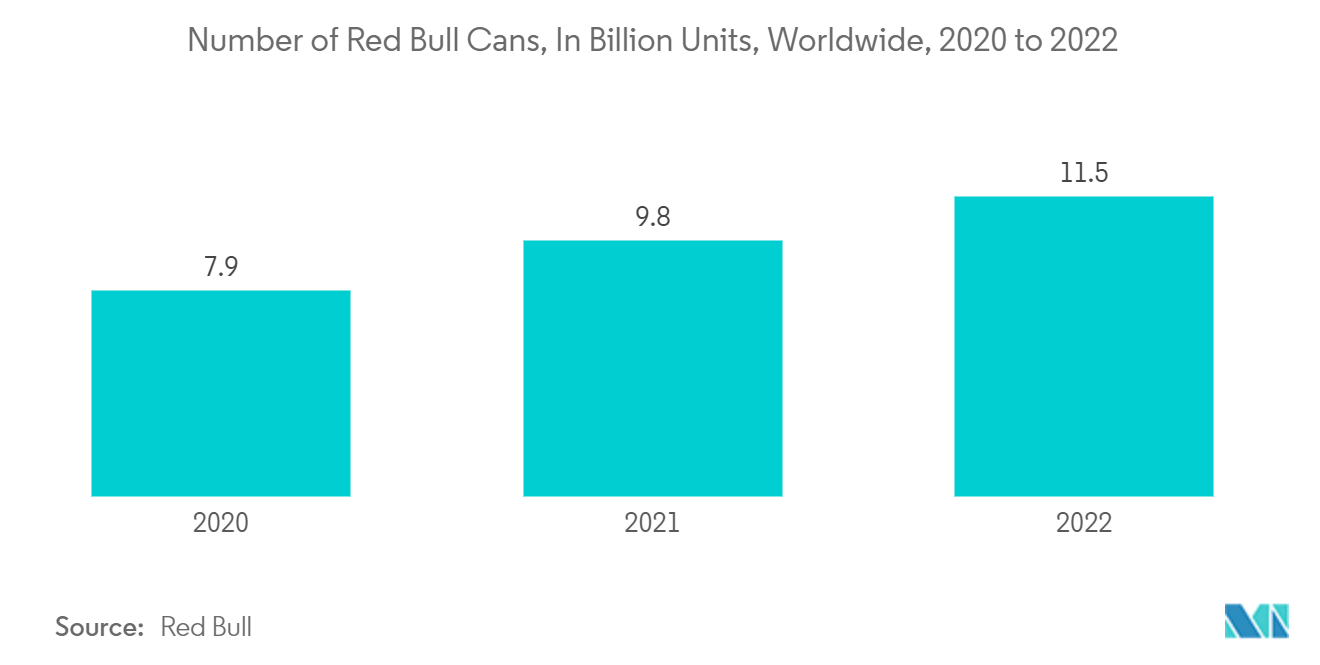

- With a huge printing surface area and various sizes, styles, and decoration choices, cylindrical aluminum beverage cans are the ideal package solution for creating a strong brand presence where it matters - on the shelf and in the hands of consumers. According to Red Bull, an energy drink brand based out of Australia, it sold more than 11.58 billion cans globally in 2022, 18.1% up from the previous year.

Asia-Pacific is Expected to Hold Major Share

- China, the largest aluminum producer in the world, reduced its output to reach net-zero carbon emissions by 2060. Therefore, the country’s aluminum imports sharply increased to compensate for the decline in domestic production. The equation has changed due to the Ukraine-Russia war. European aluminum producers cut back on production as natural gas and other energy costs increased, leading to a shortage of metal and a pricing difference of almost between China and Europe.

- Additionally, China has had access to cheaper energy and reduced production costs compared to Europe because it has not imposed sanctions on Russia. Hence, for the forecast period, the country could have the cost advantage for producing aerosol cans, which use aluminum as the primary raw material. Notable, because there is less rivalry in China than in other parts of the world, there is a huge growth opportunity for the manufacturers in the market.

- The personal care and cosmetics industries' growing demand has compelled producers to provide eco-friendly packaging options. Therefore, rising research and development (R&D) efforts and investments in green technologies propel the aerosol cans market. One of the economic sectors in China that are expected to grow the fastest and most soon is the beauty and cosmetics sector. According to the National Bureau of Statistics of China, there is a growing trend of retail sales of cosmetics by wholesale and retail businesses in the country. This growth would consequently bolster the demand for cans for packaging shampoo bottles, creams, deodorants, hair sprays, hydrating creams, and many others.

- The Indian government, as reported by the Ministry of Environment, Forest, and Climate Change, implemented a ban on single-use plastic items in response to concerns about pollution caused by such products in July 2022. With the decrease in the utilization of single-utilized plastic, the interest in aluminum or steel-based, completely recyclable metal packaging use would increment in the impending time frame across different ventures, including personal care, healthcare, pharmaceutical, and automotive.

- Although Ukraine- Russia war has bolstered India’s metal industry, and the country has strengthened its export opportunity of steel and Iron to major North American, Europe, and MEA countries, the prices of base metals are gravitating on the higher side, thereby affecting the price of products.

- The food sector is one of India's major sectors using metal cans and containers. Steel is primarily used to make rigid cans, whereas aluminum makes thin, lightweight cans. Nearly all steel used for cans is coated with a thin layer of tin to inhibit corrosion from the food and is called tin cans. The Indian market is witnessing significant emerging trends catering to the food industry. For instance, India is a major agricultural and processed food product exporter. According to the Ministry of Commerce & Industry, despite COVID-19 restrictions, particularly owing to the second wave of the pandemic, agricultural and processed food product exports achieved a robust increase of 44.3% in 2021-22 (April-June) compared to the corresponding period in 2020-21.

- Japan’s economy has entered a new phase since the beginning of the Ukraine-Russia war. Not only did the war heighten concerns about the future of the global economy, but also a series of economic sanctions declared by Japan and others have widened the gap between the Russian economy and (nearly) the rest of the globe. According to the Japan Center for Economic Research, the country’s import price index recorded a year-over-year increase of 34% in February 2022. Japan, a major importer of aluminum, faced a sudden price rise. Thereby the companies manufacturing aluminum-based aerosol cans face disruption related to the shortage of raw materials and escalated prices impacting the cost of the product.

Metal Packaging Industry Overview

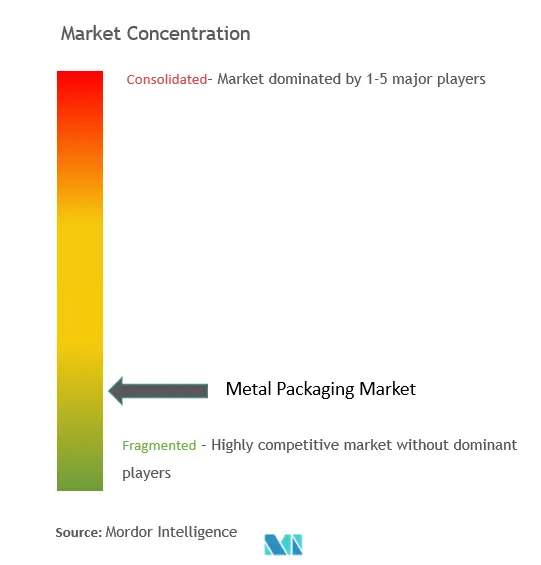

The metal packaging market is fragmented, consisting of significant individual players such as Ball Corporation, Crown Holdings, Inc., Silgan Holdings, Inc., etc. Many companies are increasing their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions.

In January 2023, CANPACK, a manufacturer of sustainable packaging solutions, joined the Aluminium Recycling Coalition, which was established in Dubai by Emirates Global Aluminium (EGA). CAN PACK has a significant aluminum can manufacturing facility in the United Arab Emirates (UAE). This Alliance, which brought together key players in the UAE's beverage, waste, and aluminum sectors, teaches people how to reuse used beverage jars most effectively to increase aluminum recycling rates.

In December 2022, Crown Holdings, Inc. announced a collaboration with Aquarius, a refreshing beverage brand produced by Coca-Cola and its dedicated print and reprographics studio, on an intelligent and engaging promotional campaign in Spain. In contrast, Aquarius was available in standard 330ml aluminum cans. This sustainable packaging format advanced a Circular Economy and helps minimize the raw materials required to be sourced from the Earth via its infinite recyclability.

Metal Packaging Market Leaders

Ball Corporation

Crown Holdings Incorporated

Silgan Holdings Incorporated

Can-Pack SA

CCL Container Inc

*Disclaimer: Major Players sorted in no particular order

Metal Packaging Market News

- February 2023: Lindal Group GmbH, a global expert in aerosol cans, has acquired shares in the biotechnology company B4PLASTICS. B4PLASTICS is a Belgian start-up developing new biopolymer materials. B4Plastics is a polymer architecture company that accelerates the adoption of new biomaterials and expands them from niche to high-volume applications. The company has a strong vision of designing and scaling materials to achieve the best balance of functionality, ecology, and cost, bridging the gap between laboratory-based research and commercial implementation.

- July 2022: Jamestrong Packaging, a food and aerosol cans manufacturer, made a USD 6 million investment in an aerosol can factory. Jamestrong Packaging intended to expand its business in Taree, New South Wales, to produce the slugs used in aerosol cans. The business would increase local production to meet the escalating product demand and generate local jobs through the new casting plant.

Metal Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute products

4.3.5 Intensity of Competitive Rivalry

4.4 Assessment of the Impact of COVID-19 on the industry

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 High Recyclability Rates of Metal Packaging

5.1.2 Convenience and Lower Price Offered by Canned Food

5.2 Market Challenges

5.2.1 Presence of Alternate Packaging Solutions

6. MARKET SEGMENTATION

6.1 By Material Type

6.1.1 Aluminum

6.1.2 Steel

6.2 By Product Type

6.2.1 Cans

6.2.1.1 Food Cans

6.2.1.2 Beverage Can

6.2.1.3 Aerosols

6.2.2 Bulk Containers

6.2.3 Shipping Barrels and Drums

6.2.4 Caps and Closures

6.2.5 Other Product Types

6.3 By End-user Vertical

6.3.1 Beverage

6.3.2 Food

6.3.3 Industrial

6.3.4 Cosmetic and Personal Care

6.3.5 Paints and Varnishes

6.3.6 Automotive

6.3.7 Household

6.3.8 Other End-user Verticals

6.4 By Geography

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 United Kingdom

6.4.2.2 Germany

6.4.2.3 France

6.4.2.4 Spain

6.4.2.5 Rest of Europe

6.4.3 Asia-Pacific

6.4.3.1 China

6.4.3.2 India

6.4.3.3 Japan

6.4.3.4 South Korea

6.4.3.5 Thailand

6.4.3.6 Rest of Asia-Pacific

6.4.4 Latin America

6.4.4.1 Brazil

6.4.4.2 Mexico

6.4.4.3 Rest of Latin America

6.4.5 Middle East and Africa

6.4.5.1 United Arab Emirates

6.4.5.2 Saudi Arabia

6.4.5.3 South Africa

6.4.5.4 Rest of Middle East & Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Ball Corporation

7.1.2 Crown Holdings Inc.

7.1.3 Can-Pack SA

7.1.4 Silgan Holdings Incorporated

7.1.5 Tubex GmbH

7.1.6 Greif Incorporated

7.1.7 Mauser Packaging Solutions

7.1.8 Ardagh Group

7.1.9 DS Containers Inc.

7.1.10 CCL Container Inc.

7.1.11 Toyo Seikan Group Holdings Ltd.

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Metal Packaging Industry Segmentation

Metal packaging is long-lasting industrial packaging comprised mostly of two key materials: steel and aluminum. The package type has outstanding qualities like durability, flexibility, and cost-effectiveness, providing various advantages over other packaging solutions for specific industrial applications. For use in packaging, aluminum is a metal that is fairly simple to sterilize. Due to its superior barrier protection and strength, it is an excellent choice for packing materials.

The Metal Packaging Market is segmented by Material Type (Aluminum, Steel), Product Type (Cans, Bulk Containers, Shipping Barrels, Drums, Caps, and Closures), End-user Vertical (Beverage, Food, Industrial, Cosmetic and Personal Care, Paints and Varnishes, Automotive, Household), and by Geography (North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material Type | |

| Aluminum | |

| Steel |

| By Product Type | |||||

| |||||

| Bulk Containers | |||||

| Shipping Barrels and Drums | |||||

| Caps and Closures | |||||

| Other Product Types |

| By End-user Vertical | |

| Beverage | |

| Food | |

| Industrial | |

| Cosmetic and Personal Care | |

| Paints and Varnishes | |

| Automotive | |

| Household | |

| Other End-user Verticals |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Metal Packaging Market Research FAQs

How big is the Metal Packaging Market?

The Metal Packaging Market size is expected to reach USD 135.94 billion in 2023 and grow at a CAGR of 3.28% to reach USD 159.74 billion by 2028.

What is the current Metal Packaging Market size?

In 2023, the Metal Packaging Market size is expected to reach USD 135.94 billion.

Who are the key players in Metal Packaging Market?

Ball Corporation, Crown Holdings Incorporated, Silgan Holdings Incorporated, Can-Pack SA and CCL Container Inc are the major companies operating in the Metal Packaging Market.

Which is the fastest growing region in Metal Packaging Market?

North America is estimated to grow at the highest CAGR over the forecast period (20221-2028).

Which region has the biggest share in Metal Packaging Market?

In 20221, the Asia Pacific accounts for the largest market share in Metal Packaging Market.

Metal Packaging Industry Report

Statistics for the 2023 Metal Packaging market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Metal Packaging analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.