Market Size of Egypt Residential Real Estate Industry

| Study Period | 2019-2028 |

| Base Year For Estimation | 2022 |

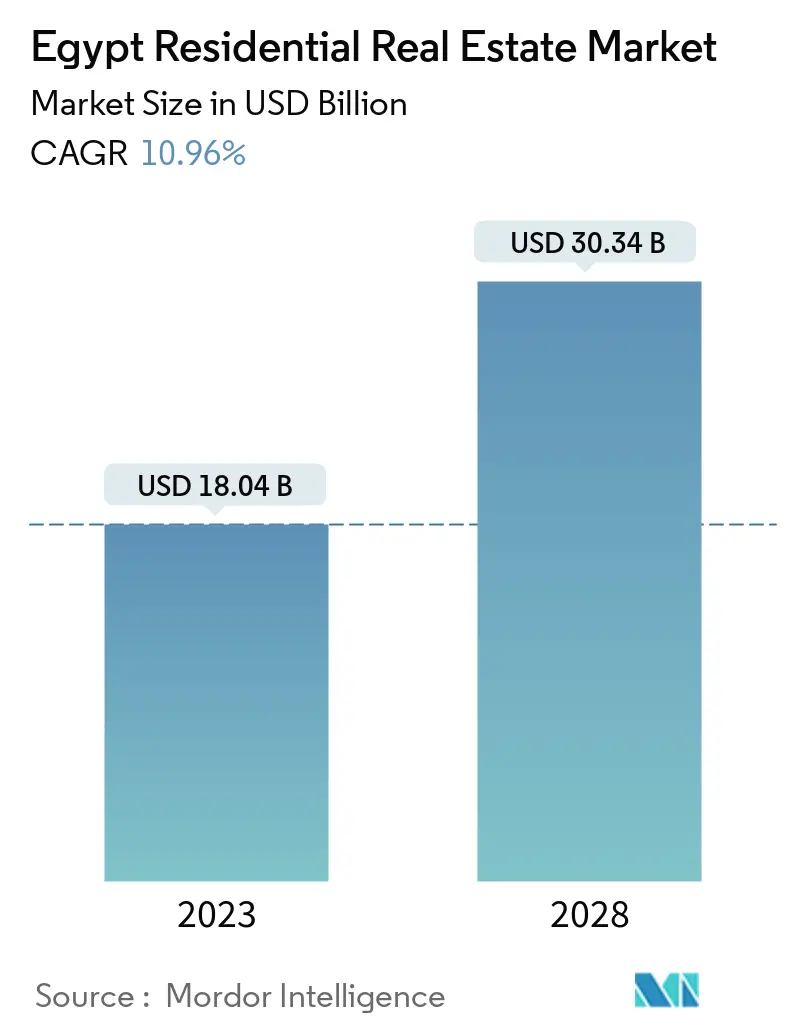

| Market Size (2023) | USD 18.04 Billion |

| Market Size (2028) | USD 30.34 Billion |

| CAGR (2023 - 2028) | 10.96 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Egypt Residential Real Estate Market Analysis

The Egypt Residential Real Estate Market size is expected to grow from USD 18.04 billion in 2023 to USD 30.34 billion by 2028, at a CAGR of 10.96% during the forecast period (2023-2028).

There is an increasing demand for residential units in key cities of Egypt, especially Cairo. Government initiatives and upcoming projects are also key drivers of the market.

- Despite the difficult economic backdrop brought on by the global pandemic, all major Egyptian real estate sectors could grow or remain stable in 2021. Cairo's residential real estate market has seen the most growth in the last year, with rents in some areas increasing by up to 8% Y-o-Y.

- In 2021, approximately 19,000 residential units were completed in Cairo, bringing the governorate's total residential stock to approximately 227,000. This is a 40% increase over the previous year, when only 2,500 residential units were delivered. Most of the residential supply completed in 2021 will be large mixed-use developments, with some developers opting for smaller-scale projects to manage cash flows. A government directive was issued in 2021 prohibiting developers from offering any units for sale until at least 30% of the project was completed.

- The Administrative Capital for Urban Development's action is also likely to have increased the project completion rate by encouraging developers to shorten the time to delivery. Looking ahead, an estimated 29,000 units were estimated to be completed in 2022, with a large proportion of them located east of Cairo. With the Greater Cairo population expected to double over the next two decades, developers will be in high demand for residential properties. The New Administrative Capital (NAC) is one area that has significantly increased its residential property offering in the last year.

- Several landmark developments, including New Garden City and Capital Residence, have been completed or are nearing completion, expanding the options for residents looking to relocate to the new city. The New Administrative Capital, which houses Egypt's key ministries, government buildings, and foreign embassies, is set to become the country's main administrative and financial center in the coming years. With over 50,000 workers expected to relocate to the NAC soon, the city will see an influx of new residents, and developers should benefit from a concentrated demand for housing.

Egypt Residential Real Estate Industry Segmentation

Residential real estate is an area developed for people to live in. As defined by local zoning ordinances, residential real estate cannot be used for commercial or industrial purposes.

The market is segmented by type (apartments and condominiums and villas and landed houses). The report offers the market sizes and forecasts in value (USD billion) for all the above segments and the COVID-19 impact is included in the report.

| By Type | |

| Apartments and Condominiums | |

| Villas and Landed Houses |

Egypt Residential Real Estate Market Size Summary

The Egyptian residential real estate market is experiencing significant growth, with an increasing demand for residential units in key cities, particularly Cairo. This growth is driven by government initiatives, upcoming projects, and a rising population. Despite economic challenges brought on by the global pandemic, the real estate market has remained stable, with some areas, such as Cairo, seeing substantial growth in residential real estate. The government has implemented measures to boost project completion rates, which will likely increase the supply of residential units. The market trends indicate a surge in private investment in the real estate sector, making it one of the most attractive investment areas in the country. The sector has managed to thrive amidst regional and global economic instability. However, the rising unit prices are exacerbating the issue of affordability. Despite this, the demand for housing remains high due to the growing population and the development of several mega projects aimed at stimulating economic growth. The luxury housing market is also seeing growth, attracting both local and foreign buyers. The industry is highly competitive with the presence of local, regional, and international players.

Explore MoreEgypt Residential Real Estate Market Size - Table of Contents

-

1. MARKET INSIGHTS AND DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Insights into Supply Chain/Value Chain Analysis

-

1.5 Industry Attractiveness - Porter's Five Force Analysis

-

1.5.1 Threat of New Entrants

-

1.5.2 Bargaining Power of Buyers/Consumers

-

1.5.3 Bargaining Power of Suppliers

-

1.5.4 Threat of Substitute Products

-

1.5.5 Intensity of Competitive Rivalry

-

-

1.6 Residential Real Estate Buying Trends - Socioeconomic and Demographic Insights

-

1.7 Government Initiatives and Regulatory Aspects Pertaining to the Residential Real Estate Sector

-

1.8 Insights into Size of Real Estate Lending and Loan to Value Trends

-

1.9 Insights into Interest Rate Regime for General Economy and Real Estate Lending

-

1.10 Insights into Rental Yields in the Residential Real Estate Segment

-

1.11 Insights into Capital Market Penetration and REIT Presence in Residential Real Estate

-

1.12 Insights into Affordable Housing Support Provided by the Government and Public-Private Partnerships

-

1.13 Insights into Real Estate Tech and Startups Active in the Real Estate Segment (Broking, Social Media, Facility Management, and Property Management)

-

1.14 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Apartments and Condominiums

-

2.1.2 Villas and Landed Houses

-

-

Egypt Residential Real Estate Market Size FAQs

How big is the Egypt Residential Real Estate Market?

The Egypt Residential Real Estate Market size is expected to reach USD 18.04 billion in 2023 and grow at a CAGR of 10.96% to reach USD 30.34 billion by 2028.

What is the current Egypt Residential Real Estate Market size?

In 2023, the Egypt Residential Real Estate Market size is expected to reach USD 18.04 billion.