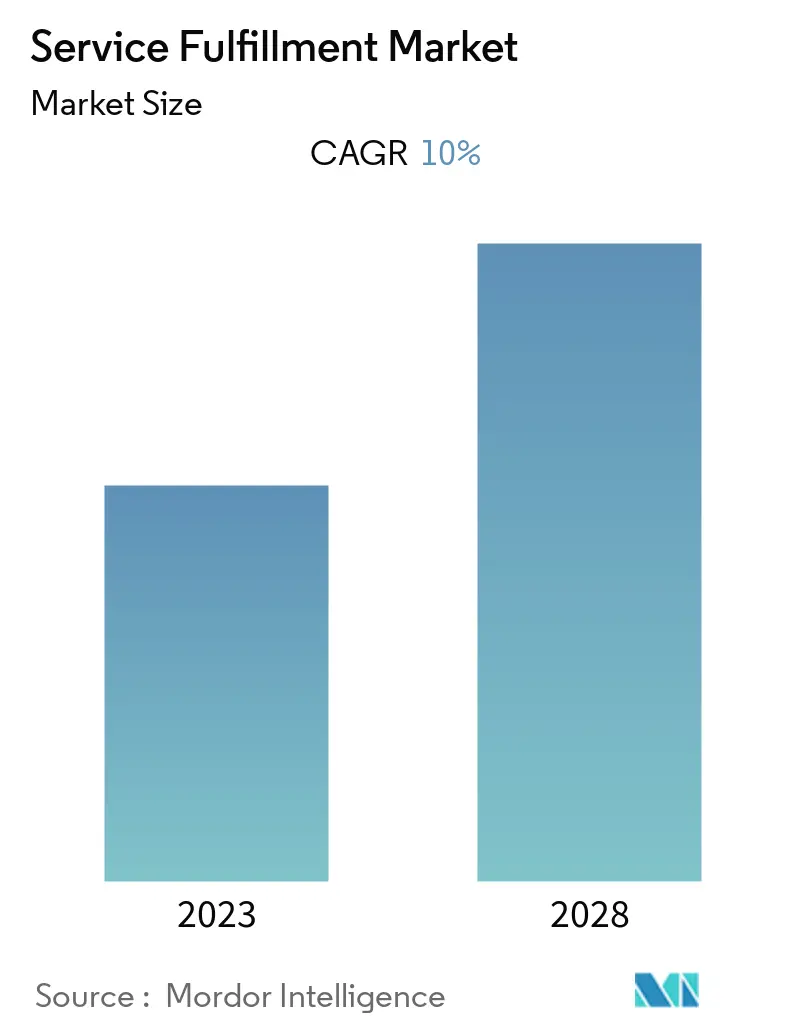

Service Fulfillment Market Size

| Study Period | 2018 - 2028 |

| Base Year For Estimation | 2022 |

| CAGR | 10.00 % |

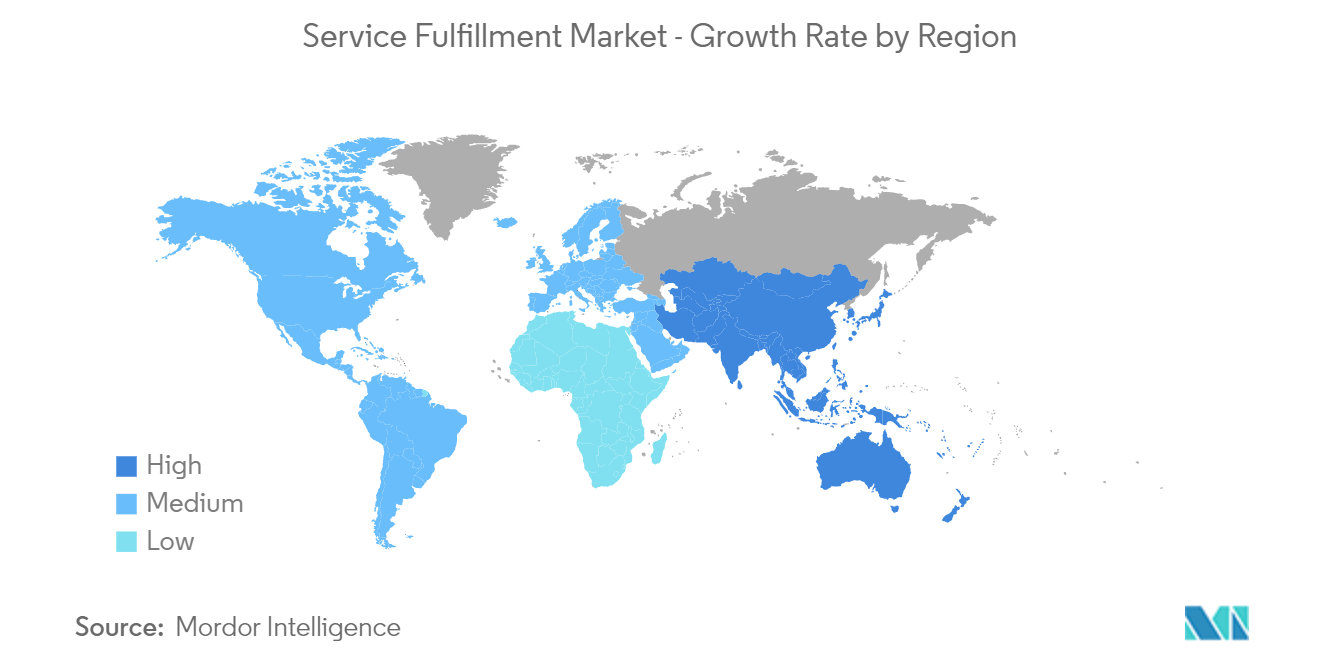

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Service Fulfillment Market Analysis

The Service Fulfillment Market is expected to register a CAGR of 10% during the forecast period. Service providers are building capabilities to provide services while reducing time-to-market for next-generation products and services, owing to the introduction of several technologies across industries. Technologies such as IoT, connected devices, 5G technology, digitization, and increase the demand for enhanced connectivity solutions.

Service fulfillment is a combined comprehensive set of tools that assist in streamlining various tasks of CSPs and organizations to reduce time to market, optimize cost, and boost automation. Network optimization becomes essential to meet new and growing service fulfillment needs.

A dynamic service fulfillment process or software enables the creation of component-based services and simplifies the launch of new products. It automates the order-to-cash process to optimize supply chain activities, capital expenditures, and operating expenses. The supply chain management solutions streamline network equipment procurement while rationalizing the supplier ecosystem.

Rapid connectivity devices and user expansion drive the global service fulfillment market. Moreover, large-scale expenditures in telecom operating technologies are increasing in demand in this industry. Moreover, simple access to crucial management solutions is propelling this industry forward. Rising income from data services drives demand in the global service fulfillment market.

Further, automation drives business productivity, which is always desirable. The challenge is achieving it cost-effectively. The cloud has efficiently streamlined the automation and use of IT infrastructures, such as server virtualization and configuration. Still, network automation has been slower to evolve due to higher complexity levels, especially among communication service provider (CSP) networks, which often cross an increased number of domains (cloud, mobile, WAN, and IT) and require higher levels of investment.

The COVID-19 pandemic impacted service fulfillment throughout the globe. The major challenge during the pandemic was workforce-related issues. Post-pandemic, the market was growing rapidly with the rapid adoption of virtualized network functions into usable components for customer service creation.

Service Fulfillment Market Trends

Increasing Network Automation and Increasing Demand for Automated, Real-time Services Drives the Market Growth

The rollout of several technological advancements, such as 5G technology, IoT, AI, Digitization, and many more, Communication Service Providers (CSPs) face constant pressure to enhance and exceed rising customer expectations while minimizing operational costs, with little visibility across platforms, systems, tools, and fragmented data.

With the increasing number of users, connected devices, mobile devices, applications, and the deployment of advanced technologies and capabilities, they are increasing their dependence on enhanced network infrastructure and enhanced connectivity solutions for essential connectivity to a wide range of endpoints.

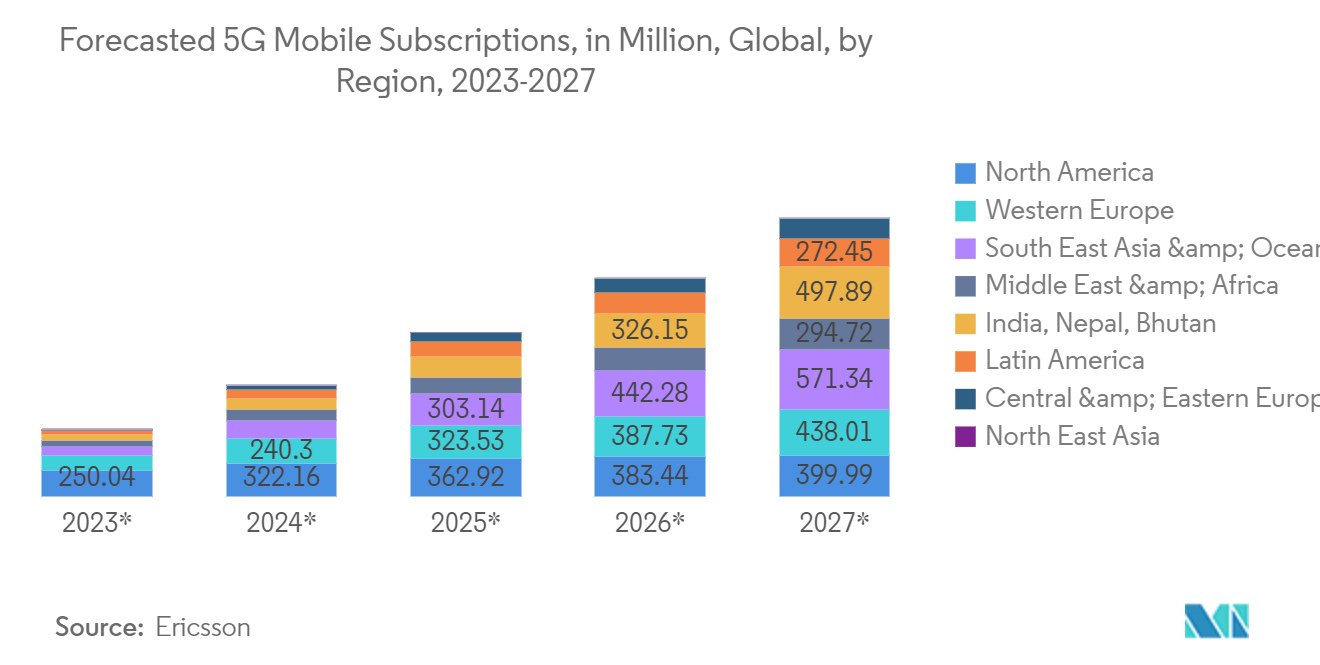

According to Ericsson, 5G subscriptions are forecast to increase globally from the current year to the following four, from over 1.6 billion to over 4 billion, respectively. North East Asia, South East Asia, India, Nepal, and Bhutan are expected to have the maximum regional subscriptions.

Subsequently, organizations and CSPs are increasingly investing in new network architectures that incorporate advanced management tools to drive the adoption of autonomous networks, leveraging technologies like AI and ML. Hence, the CSPs are contacting Service Fulfillment solution providers to enhance their supply chain activities.

Another trend in the market is the demand for continuous evaluation and performance of networks due to increased network traffic and network processing, particularly from the local area networks, which require real-time streaming network analytics and allows customers to keep track of the health of their network and continuously monitor traffic flows.

This also provides multi-dimensional visualization of application performance, network security, and utilization, thus, allowing companies to analyze and mitigate issues at the site level, application dimension, or individual IP address faster than ever before, thereby significantly improving the end-user experience.

North America is Expected to Register the Largest Market

The North American region is witnessing an increase in the demand for service fulfillment solutions due to an increase in the demand for enhanced connectivity solutions across various platforms, such as video streaming, video calling platforms, and teleconferencing, among various others.

This, coupled with a rapid increase in subscribers on various networks such as 2G, 3G, 4G, 5G, etc., propel the players to adopt service fulfillment. For instance, According to Ericcson, the region is expected to hold close to 250.04 million 5G subscriptions accounting for more than 60 percent of mobile subscriptions in the current year.

Also, the region has become a major hub for the 5G rollout, with Canadian service providers increasingly investing in procuring 5G licenses.

Furthermore, in December 2022, JLL and Quiet Platforms, an American Eagle Outfitters Inc. completely owned subsidiary, announced a collaboration to speed the building of additional advanced fulfillment facilities across the United States in 2023 to service retailers and brands in the Quiet Platforms supply chain network. The two businesses would pioneer a flexible rent-as-a-percentage-of-revenue model for logistics real estate under the terms of the agreement.

Moreover, in April 2022, FlavorCloud, one of the premier headless international logistics software providers, announced a new relationship with ShipBob, the global omnifulfillment platform with over 30 fulfillment facilities in the United States, United Kingdom, Europe, and Australia. ShipBob is completely integrated with the FlavorCloud platform and cross-border services, providing consumers with a smooth and loyalty-building international shipping and returns experience regardless of product kind, shipment origin/destination, or preferred service level.

Service Fulfillment Industry Overview

The Service Fulfillment Market is moderately highly fragmented with the presence of major players like Comarch SA, Accenture PLC, Cisco Systems, Inc., Infosys Limited, and TATA Communications Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In November 2022, Comarch and ITOCHU Techno-Solutions, one of the leading Japanese integrators, signed a framework agreement to streamline and broaden cooperation in operations support readiness, fulfillment, assurance, and service monitoring, in preparation for changes in the Japanese telecom market's digital transformation.

In September 2022, MacGregor Partners, one of the major supply chain consulting and technology suppliers specializing in intelligent logistics and warehouse management, has been acquired by Accenture. Accenture's supply chain network and fulfillment transformation capabilities, backed by Blue Yonder technology, would be expanded due to the acquisition.

Service Fulfillment Market Leaders

Comarch SA

Accenture PLC

Cisco Systems, Inc.

Infosys Limited

TATA Communications Ltd.

*Disclaimer: Major Players sorted in no particular order

Service Fulfillment Market News

- February 2023: AutoStore has announced the availability of a pay-per-pick service for its industry-leading fulfillment automation technology, which has more than 1,150 units in operation globally. The new solution would enable retailers to fulfill the rising need for more efficient warehouse operations and faster customer delivery at a lower entry price point.

- November 2022: Microsoft Corp. announced the Microsoft Supply Chain Platform, which assists to help enterprises in optimizing their supply chain data estate investment through an open approach by integrating the Microsoft AI, collaboration, low-code, security, and SaaS apps in a scalable platform. Customers that use Dynamics 365 Supply Chain Management get automatic access to Supply Chain Center. The Supply Chain Center order management module enables enterprises to effectively organize and automate fulfillment using a rules-based system that leverages real-time omnichannel inventory data, AI, and machine learning.

Service Fulfillment Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers/Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Network Automation and Increasing Demand for Automated, Real-time Services

5.1.2 Rapid Adoption of Virtualized Network Functions into Usable Components for Customer Service Creation

5.2 Market Restraints

5.2.1 Lack in Awareness

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 Software

6.1.1.1 Network Management

6.1.1.2 Inventory Management

6.1.1.3 Service Order Management

6.1.2 Services

6.2 By Deployment Mode

6.2.1 On-Premise

6.2.2 Hosted

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia-Pacific

6.3.4 Rest of the World

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Comarch SA

7.1.2 Accenture PLC

7.1.3 Cisco Systems, Inc.

7.1.4 Infosys Limited

7.1.5 TATA Communications Ltd.

7.1.6 Amdocs Group

7.1.7 Suntech S.A.

7.1.8 Telefonaktiebolaget LM Ericsson

7.1.9 NEC Technologies India Private Limited

7.1.10 Hewlett Packard Enterprise Development LP

7.1.11 TIBCO Software Inc.

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

Service Fulfillment Industry Segmentation

Service fulfillment solutions streamline, simplify, and automate the fulfillment process, which helps operators and vendors, such as telecommunication providers, Communication Service Providers (CSPs), ISPs (Internet Service Providers), and similar vendor companies, better manage the entire product and order lifecycle. It provides the operators and service providers the service agility they need across all the process areas involved, from planning to provisioning to activation.

The Service Fulfillment Market is segmented by type (Software (Network Management, Inventory Management, Service Order Management), Services), by deployment mode (On-Premise, Hosted), by geography (North America, Europe, Asia Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

| By Type | |||||

| |||||

| Services |

| By Deployment Mode | |

| On-Premise | |

| Hosted |

| By Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Service Fulfillment Market Research FAQs

What is the current Service Fulfillment Market size?

The Service Fulfillment Market is projected to register a CAGR of 10% during the forecast period (2023-2028).

Who are the key players in Service Fulfillment Market?

Comarch SA, Accenture PLC, Cisco Systems, Inc., Infosys Limited and TATA Communications Ltd. are the major companies operating in the Service Fulfillment Market.

Which is the fastest growing region in Service Fulfillment Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2023-2028).

Which region has the biggest share in Service Fulfillment Market?

In 2023, the North America accounts for the largest market share in the Service Fulfillment Market.

Service Fulfillment Industry Report

Statistics for the 2023 Service Fulfillment market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Service Fulfillment analysis includes a market forecast outlook to 2028 and historical overview. Get a sample of this industry analysis as a free report PDF download.